- Fluctuations in global tags lead to fewer inquiries

- Chinese spot, futures prices decline $5-7/t w-o-w

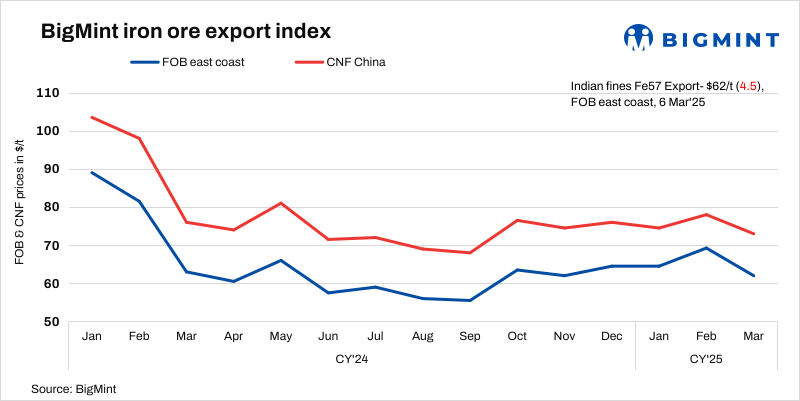

Indian iron ore fines export prices declined by $6-7/tonne (t) w-o-w due to subdued market sentiment in China and a lack of buyers in the market. Sharp fluctuations in global prices led to fewer inquiries, with exporters awaiting price clarity before making further deals.

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index declined by $4.5/t w-o-w to $62/t FOB east coast, India, on 6 March 2025. However, prices were stable against the previous assessment on 3 March. Odisha-based traders sold around 110,000 t of iron ore fines (Fe 57%) at $73-75/t CFR China last weekend. However, trades remained muted till the middle of this week.

Commenting on recent market fluctuations, an Odisha-based seller stated, “Exporters are hesitant to offer cargoes, as current bids are too low. We are waiting for the Chinese market to provide some direction before committing to deals. The recent drop in global indices led to lower bids from buyers, with discounts on Fe 57% cargoes hovering at around 20-21%.”

On the domestic front, the market performed well, supported by active procurement from exporters. However, export market sentiment was weak, with expectations that prices could decline further. The outcome of China’s upcoming economic policy meeting is expected to provide better clarity on future trends.

A miner informed BigMint, “The export market is slow, as sellers are not willing to sell at the current prices. However, the domestic market is stable with good demand. We are only taking higher-priced orders for lower grades, following material availability concerns amid the fiscal year-end.”

Sources indicate that fines export prices declined due to poor demand and weak macroeconomic indicators from China. The poor economic outlook in China is a major factor impacting iron ore prices. Chinese steel demand remains sluggish, and mills are cautious about procuring raw materials.

As per reports, the recent announcements from the Two Sessions policy meeting did not fulfil market expectations, as the expected stimulus measures failed to materialize. This has resulted in a continued decline in prices of raw materials such as iron ore and coking coal. Additionally, news of crude steel production cuts further pressured the market, with iron ore prices expected to drop below the $100/t CFR, which is lower than market expectations.

Chinese spot prices decline w-o-w: The benchmark iron ore fines prices in China dropped sharply by $7/t w-o-w to $100/t CFR on 5 March. Tariff concerns on steel products pressured the raw material market, with limited buying seen. Secondary market transactions were also limited, as participants awaited updates from China’s Two Sessions. Deliveries scheduled for the second half of April may fetch higher prices.

DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract opened at RMB 777/t ($103/t), falling by RMB 28/t ($4/t) w-o-w on 6 March. D-o-d, prices inch up by RMB 4.5/t ($1/t) today.

Price indicators

- Two (2) deals were reported in this publishing window and one (1) was considered for price calculations. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received nineteen (17) indicative prices in the current publishing window, and sixteen (16) were considered for price calculation as T2 inputs and given a 50% weightage.

Outlook

As per BigMint’s analysis, iron ore export prices are likely to remain under pressure unless there is a positive policy shift in China.

Leave a Reply