- Around 350,000 t of iron ore export deals heard

- Global benchmark change weighs on export market

India’s iron ore export market witnessed a notable decline this week, with only a handful of trades concluded for late-December 2025 laycan cargoes. A few lump cargoes were also finalised by exporters, but overall activity remained subdued as buyers adopted a cautious stance.

Prices, deals

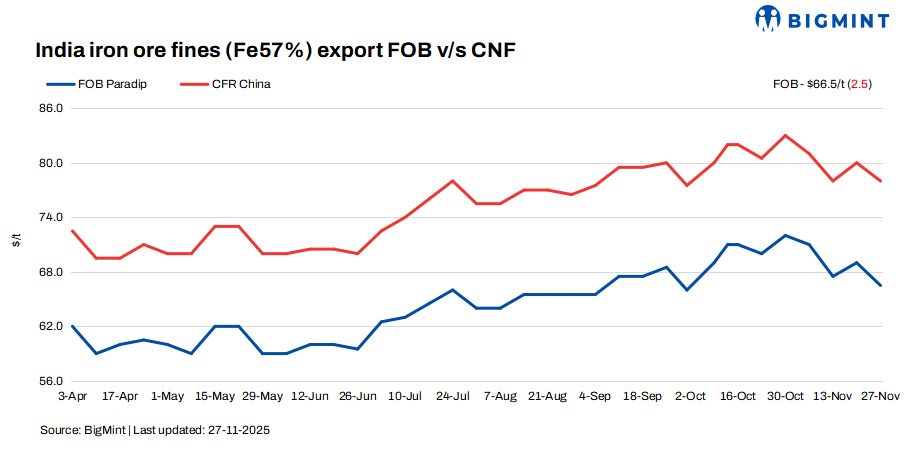

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices fell by $2.5/tonne (t) w-o-w to $66.5/t FOB east coast on 27 November. Meanwhile, the index stood at $78/t CFR China.

BigMint heard approximately 350,000 t of export deals during this publishing period, primarily for December laycan with a couple of iron ore lump cargoes recorded from the west coast.

Some suppliers put their export offers on hold due to weakening export prices and higher prices on the domestic market.

Market scenario

The price drop was largely driven by a widening discount on Indian low-grade fines, with the current discount for 57% Fe cargoes assessed at 17–18%, compared to previous weeks. According to a leading market source, “The widening discount has pressured overall offers, and buyers are not willing to engage unless they see deeper cuts.”

A key factor weighing on sentiment was the recent shift by the Australian global benchmark from using the Fe 62% index to the Fe 61% index for January laycan pricing. This index transition has further weakened confidence in the export market. An exporter noted, “Shifting to the 61% index is pulling sentiment down as it signals lower comparative valuations for Indian material.”

Meanwhile, Chinese demand remained moderate, with mills showing little urgency to secure Indian fines. An international trader stated, “Chinese mills are comfortable with current inventories and are in no hurry. Indian fines are simply not their priority right now.”

On the supply side, several exporters are holding back cargoes, closely monitoring the evolving market scenario. “Sellers are cautious. Many are analysing ongoing sentiment before committing to new deals,” an exporter said. A few miners did offer low-grade fines into the seaborne market; however, higher prices have failed to entice buyers.

Chinese spot prices firm w-o-w: The benchmark iron ore fines index inched up $2/t w-o-w to $107/t CFR China on 26 November. The prices were firm due to increased trading activity for January cargoes, which boosted market liquidity and supported mainstream grades. Buyers moved in to secure material ahead of upcoming shipments, creating short-term demand strength despite weak steel mill margins and cost pressures from higher coke prices.

DCE iron ore futures rise: Iron ore futures on the Dalian Commodity Exchange (DCE) for the Jan 2026 contract closed at RMB 799.5/t ($114/t) on 27 November, surged RMB 11/t ($2/t) w-o-w.

Rationale

- Two (2) major deals for Fe 57% were recorded during this publishing window, which were taken for price calculation. Therefore, T1 trade was given 50% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received twenty-one (21) indicative prices in the current publishing window, and fourteen (14) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports were recorded at 139.04 mnt on 27 November, falling by 0.58 mnt w-o-w, as per data published by SteelHome.

Outlook

According to BigMint, uncertainty regarding global prices is rising. The consensus among market participants suggests that Indian iron ore export prices are likely to remain rangebound in the near term. As per source, “Volatility has increased and we may not see clear pricing signals until early January.”

Leave a Reply