- Chinese steel production cut rumours weigh on market

- Indian iron ore fines export trade dynamics remain slow

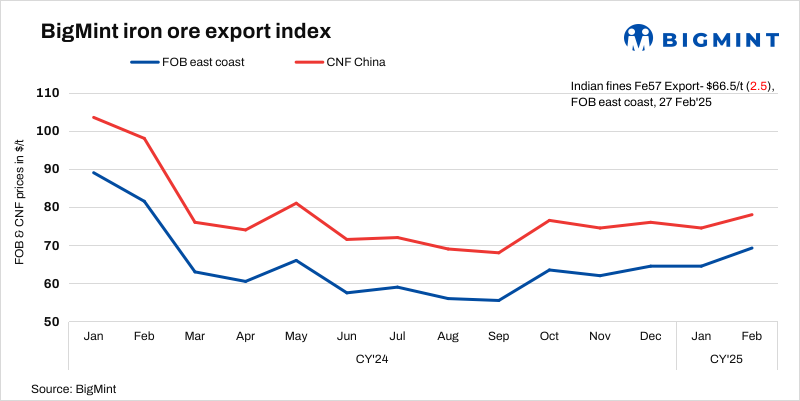

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2.5/t w-o-w at $66.5/t FOB east coast, India, on 27 February 2025. Meanwhile, prices declined by $3/t against the previous assessment on 24 February. Odisha-based traders sold around 115,000 t of iron ore fines (Fe 57%) at $78-79/t CFR China last weekend. Market participants remained cautious this week and deals were subdued.

Indian iron ore fines export prices declined this week due to weak global demand and reduced buying interest. The recent drop in global indices led to lower bids from buyers, with discounts on Fe 57% cargoes hovering around 19-20%.

Market sentiment took a hit following reports of a potential 50 million tonnes production cut in China’s steel sector. “The expected reduction in crude steel output has dampened raw material demand, leading to cautious buying activity,” a trader based in Odisha commented.

Exporters have largely adopted a wait-and-watch approach, seeking further clarity on market trends. While a few deals were concluded last weekend, trade volumes have remained muted this week.

An exporter commented: “There is uncertainty in the market, and traders are hesitant to commit to deals at current price levels.”

The disparity between bid and offer prices, coupled with strong domestic prices, is likely to further slow down exports in the coming days.

A miner informed, “The current price fluctuation has led to drop in the overseas deals inquiries and exporters have no option other than waiting for clarity about market dynamics.”

Speculation is growing that the government may implement a reduction in steel production by 50 million tons (mnt) this year. This, combined with expectations of an interest rate cut and supportive policies to be discussed during the 4-11 March meetings, has fueled a positive market outlook for steel but the raw material import market has witnessed the downtrend sentiments.

On the other hand, as the Two Sessions approach, Chinese market participants are closely watching for policy interventions, including production controls and economic stimulus measures, to effectively bolster the steel sector and drive domestic consumption.

Chinese spot prices rangebound w-o-w: The benchmark iron ore fines prices in China dropped by $1/t w-o-w to $107/t CFR on 26 February. Demand for low- to medium-grade fines persisted, with several portside deals concluded. However, low prices and abundant supply continued to pressure import margins.

DCE iron ore futures up: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract opened at RMB 805/t ($107/t), falling by RMB 32/t ($4/t) w-o-w on 27 February. D-o-d, prices dropped by RMB 7/t ($1/t) today.

Price indicators

- One (1) deal was reported in this publishing window and considered for price calculations. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received nineteen (19) indicative prices in the current publishing window, and fourteen (14) were considered for price calculation as T2 inputs and given a 50% weightage.

Few reports suggested that concerns about rising trade tensions have increased as several countries imposed anti-dumping duties on Chinese steel, which could impact export volumes. In response, the industry may contemplate reducing production to stabilise supply and avoid price declines. China might cut crude steel output by 50 mnt in CY25, followed by reductions of 20 mnt in CY26 and 10 mnt in CY27. However, the certainty of these measures remains unclear.

Leave a Reply