- Indian HRC export offers remain stable amid weak demand.

- EC’s proposal introduces TRQ system for 28 steel product categories

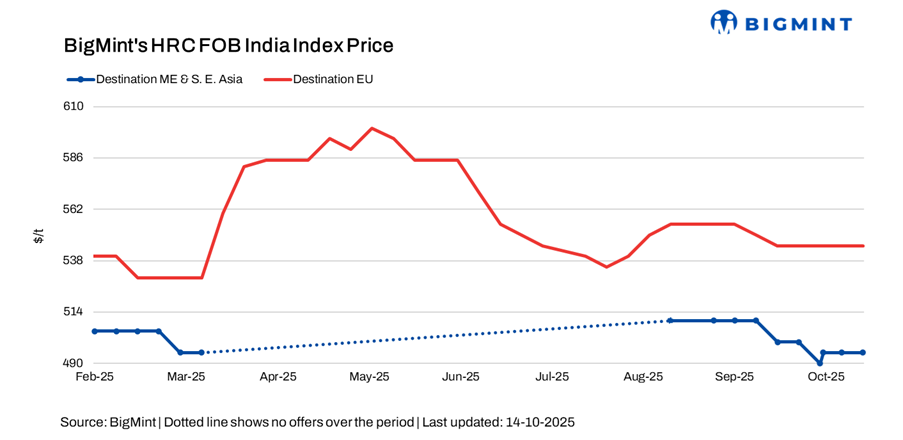

BigMint’s Indian hot-rolled coil (HRC, S275) export index for Europe held steady w-o-w at $545/tonne (t) FOB main port, due to stagnant trading activity. As per sources, “Due to the Anti-Dumping Duty (ADD) investigation, the mills are making highly selective offers, resulting in a lack of market interest”.

The Indian HRC (SAE 1006) export index for the Middle East and Vietnam remained steady w-o-w. This price stability can be attributed to weak demand in both regions, with the Middle East experiencing low demand ahead of its fiscal year-end and Vietnam’s demand dampened due to natural calamity in the region.

1. Indian HRC offers to EU remain stable w-o-w: Indian HRC export offers to the EU remains stable w-o-w with offers hovering around $595-600/t CFR Antwerp ($545-550/t FOB India), the trading activity remained muted as market players stayed cautious as European Commission has proposed a new regulation to replace the existing steel safeguard mechanism, aiming to strengthen protection for the EU steel industry amid mounting global overcapacity and trade distortions.

The European Commission’s proposal introduces a Tariff Rate Quota (TRQ) system for 28 steel product categories, with an annual quota of 18.3 million tonnes. Imports exceeding the quota will incur a 50% ad valorem duty, the quota will be administered quarterly.

Domestic demand in the EU remains uncertain due to the proposed changes to steel import safeguards and the implementation of CBAM. Market players are cautious, adopting a wait-and-see approach. While demand is expected to remain steady, local mills are likely to increase prices, potentially leading to fewer sales and less consumption.

2. Indian HRC offers to Middle East stay flat w-o-w: China maintained its HRC export offers to the Middle East at $505–510/t CFR UAE, showing w-o-w stability post National Day holidays in China. Japanese HRC offers are ranging around $475-480/t, however, no fresh offers were heard from Indian mills, the last heard offers were at $520/t CFR UAE. Market activity is notably slow, primarily because buyers are winding down purchases ahead of their December financial year-end.

HRC futures on the Shanghai Futures Exchange (SHFE) January 2026 contracts fell by RMB 33/t ($6/t) to RMB 3,240/t ($454/t) as on 14 October 2025 compared to RMB 3,273/t ($458/t) as on 9 October 2025. Moreover, on a d-o-d basis, contracts decreased by RMB 22/t ($3/t) against RMB 3,264/t ($457/t).

3. Indian HRC offers to Vietnam remain unchanged w-o-w: Indian HRC export offers to Vietnam remained stable at $505-510/t CFR Ho Chi Minh City (HCMC), but demand in Vietnam stayed weak due to the aftermath of Typhoon Matmo, which caused significant damage. The recent flooding and storms, particularly in Hanoi, are expected to further slow demand recovery. The typhoon’s impact has likely worsened the already sluggish steel market in Vietnam.

Outlook

The short-term outlook for Indian HRC exports is marked by price stability but muted trading activity. Demand remains weak across key markets. Europe is cautious due to proposed new safeguards and an Anti-Dumping Duty investigation, leading to stagnation. Meanwhile, Middle East faces a pre-fiscal year-end slowdown, and Vietnam’s recovery is hampered by recent natural calamities, keeping overall market interest low.

Leave a Reply