- EU sentiment weakens amid carbon-cost uncertainty

- Middle East demand eases amid Ramadan

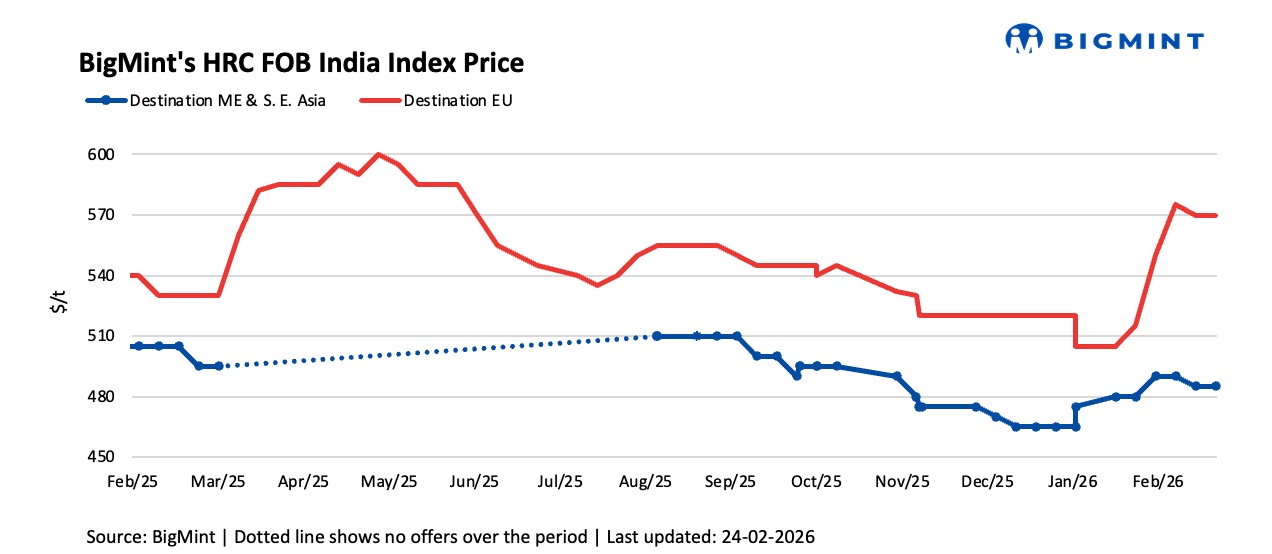

BigMint’s Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at around $570/t FOB main port as of 24 February. Similarly, the Indian HRC (SAE 1006) export index for the Middle East and South East Asia held steady w-o-w at around $485/t FOB main port amid weak demand and cautious buying sentiment across the regions.

1. HRC offers to the EU: Indian HRC export offers to the EU remained unchanged w-o-w at $620/t CFR Antwerp, amid cautious buying interest and regulatory uncertainty in Europe. Demand for imported coils continues to remain subdued following the implementation of the EU’s Carbon Border Adjustment Mechanism (CBAM) and the anticipated shift to new trade measures replacing existing safeguards. The lack of clarity has heightened uncertainty around import costs, leading to a cautious market sentiment among European buyers, with preference gradually shifting towards domestic production.

Furthermore, ArcelorMittal, a leading European steelmaker, has raised its HRC prices by around EUR 50/t ($59/t) m-o-m to EUR 750/t ($884/t) base delivered for May’26 deliveries. The price increase is primarily driven by the introduction of CBAM in 2026, along with expectations of tighter import availability and an anticipated 47% reduction in steel import quotas, despite continued weakness in overall demand.

2. HRC offers to the Middle East: Indian HRC export offers to the Middle East remained steady w-o-w at around $510/t CFR UAE, as weak demand and subdued buying activity during Ramadan continued to weigh on market sentiment.

Moreover, Chinese HRC export offers to the Middle East remained steady w-o-w at around $500/t CFR UAE, as market participants have just returned following the Lunar New Year slowdown, keeping offers largely unchanged.

Outlook

The Indian HRC export market is likely to remain cautious in the coming week amid subdued demand across key regions. In the EU, buyers remain cautious due to uncertainty surrounding the CBAM and anticipated safeguard measures, while demand in the Middle East continues to be soft amid Ramadan.

Leave a Reply