- 30,000-t Indian deal heard closed at $570/t CFR Antwerp

- India’s HRC offers to Middle East decrease by $5/t w-o-w

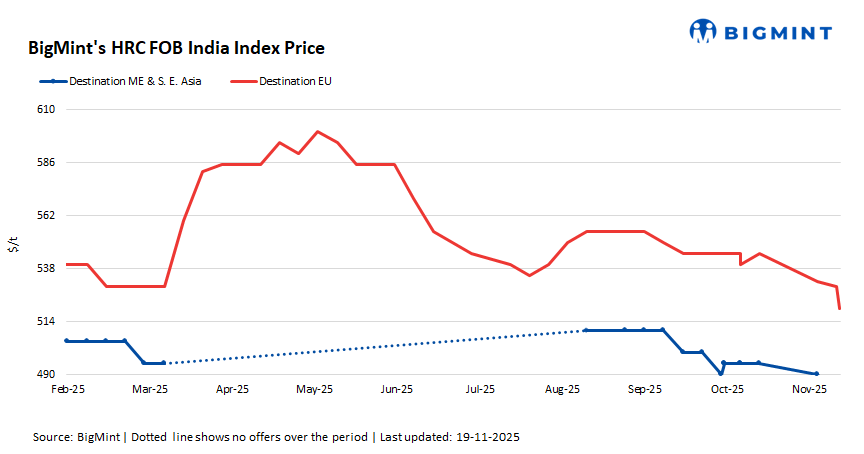

BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) region declined by $10/tonne (t) w-o-w to $520/t FOB main port on 18 November, with a deal heard concluded at around this level for December 2025 shipment. Additionally, the HRC (SAE 1006) export index for the Middle East dropped by $5/t w-o-w to $475/t FOB.

1. HRC offers to EU drop w-o-w: Indian HRC export offers to the EU dropped by $10/t w-o-w to $570/t CFR Antwerp as compared to $580/t CFR a week ago. A deal for around 30,000 tonnes (t) was heard concluded at similar price levels for December 2025 shipment.

Overall, demand in the region remained low, as buyers stayed cautious ahead of the implementation of the Carbon Border Adjustment Mechanism (CBAM).

In the domestic segment, demand remained weak, with limited, need‑based spot transactions. Buyers adopted a cautious stance due to CBAM concerns and tight margins. However, producers remained optimistic about price hikes in the near term, expecting the CBAM to discourage buyers from sourcing imports.

2. HRC offers to Middle East decline w-o-w: Indian HRC export offers to the Middle East stood at $500/t, down by $5/t w-o-w against $505/t CFR UAE a week ago. Indian steel export volumes to the UAE in October 2025 were at around 31,241 t, falling by 67% from 93,822 t a month ago. Furthermore, export volumes dropped by 43% as compared to 54,960 t in October 2024.

Meanwhile, Chinese HRC offers to the Middle East remained stable w-o-w at $480/t CFR UAE.

HRC futures on the Shanghai Futures Exchange (SHFE) January 2026 contracts edged up by RMB 35/t ($5/t) w-o-w to RMB 3,283/t ($462/t) as on 18 November 2025, compared to RMB 3,248/t ($457/t) as on 11 November 2025. Moreover, on a d-o-d basis, contracts were up marginally by RMB 4/t ($1/t) against RMB 3,279/t ($461/t).

Outlook

The short‑term outlook for Indian HRC export offers remains subdued. European demand is weak, and buyers are waiting for clarity regarding the CBAM, keeping purchases limited. In the Middle East, despite falling prices of Indian shipments, there is stiff Chinese competition. Year-end budget closures may also curb large-scale bookings for Indian material. Consequently, prices are poised to remain flat or decline slightly.

Leave a Reply