- BF rebar trade prices down INR 1,300/t w-o-w, inventory rises

- HRC tags fall marginally, coated segment sees sharper correction

- Weak global sentiments, monsoon blues to affect prices in short term

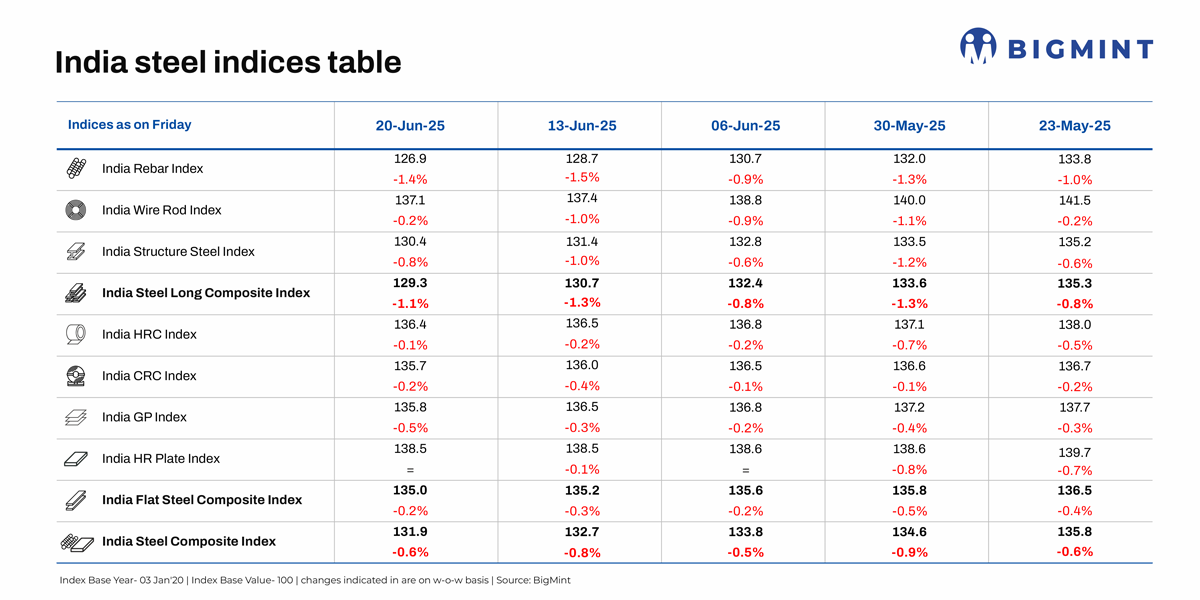

Morning Brief: The depression in the domestic steel market continued last week, with steel prices witnessing a steady downward spiral. BigMint’s India steel composite index, a fixed reference point for the domestic steel market, dropped 0.6% w-o-w on 20 June 2025, with long steel prices correcting more sharply than flats.

While the flats index decreased by 0.2% w-o-w, the longs composite index plunged 1.1%. The onset of monsoon has exacerbated the market slowdown; however, in general, deteriorating trade sentiments, weak global prices and geopolitical unrest have been exerting pressure on the global steel market for quite some time.

Steel price movements

Longs

BF rebar prices decline: Major primary steel producers reduced rebar prices amid lacklustre trade, with list prices ranging between INR 51,500-52,500/tonne (t) ($595-606/t) on landed basis. Inventories at large integrated mills rose significantly to around 400,000 t as of mid-June.

Trade-level BF rebar prices declined by INR 1,300/t ($15/t) w-o-w to INR 51,900/t ($599/t) exy-Mumbai, as per BigMint’s assessment on 20 June. Prices are exclusive of GST at 18%.

On the supply side, production ramp-ups are expected to intensify pressure on prices. A major private mill has restarted its BF and hot metal production, while another has resumed operations at its LD converter facility. Additionally, a third BF of a PSU steelmaker is set to begin operations this month, likely adding further volumes to the market.

Selling pressure drags down IF rebar prices: IF rebar prices dropped by INR 900/t ($10/t) w-o-w to INR 44,000/t ($508/t) exw-Mumbai as on 20 June. Prices remained under pressure amid monsoon disruptions and labour shortages impacting construction demand.

Mills cut list prices and offered discounts, as inventory levels rose to 12-15 days, with some regions seeing even higher stockpiles. Weak buying interest and continued drops in semi-finished and sponge iron prices further dampened sentiment.

Flats

HRC trade prices fall marginally: BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 500/t w-o-w to INR 50,900/t ($601/t) on 17 June. Additionally, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 200/t ($1/t) w-o-w to INR 58,100/t ($684t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Distributors experienced weaker demand, with a decline in inquiries and even slower conversion to actual sales. Purchases were limited and need-based, often in smaller quantities. As the quarter-end approaches, there is increased pressure to clear inventory and manage capital rotation efficiently.

“The market expects mills to offer price support soon; if not, the trade segment may incur significant losses. Meanwhile, the supply of CRCs is improving due to increased production from mills,” a market participant informed.

Coated flat steel prices edge down: India’s coated flat steel prices weakened last week amid slowing demand with intensifying monsoons. Galvanised plain (GP) coil prices dropped in the range of INR 100-500/t ($1-6/t) w-o-w across markets. Pre-painted galvanised iron (PPGI) coil prices were rangebound in the benchmark market of Mumbai.

“Demand for profiled cladding and roofing sheets is expected to be there or the next 7-10 days. However, with the monsoons intensifying, it shall wane,” said a north India-based distributor.

Prices of substrate products such as hot-rolled (HR) and cold-rolled (CR) coils have also not declined steeply amid the import restrictions by way of the safeguard duty in place. This gave prices some stability and restrained steeper declines in the recent past, sources hinted.

Subdued export trends: BigMint’s India HRC (S275) export index fell by $15/t w-o-w to $555/t FOB East India, as EU demand remained weak due to sluggish automotive and construction activity. Trade also slowed because of the Corpus Christi holidays. Meanwhile, Indian mills held back HRC offers to the Middle East amid stiff competition from other regions.

Outlook

Flat steel imports have fallen sharply since the implementation of the provisional safeguard duty and, therefore, there is no direct pressure on domestic prices due to dumping. Raising the current tariff to 24% will surely provide further protection to the domestic industry. But HRC prices are likely to remain under pressure on weakening exports and the slowdown in global demand amid high tariffs.

Market participants expect rebar prices to correct further and likely bottom out in the coming days. Procurement remains cautious amid weak demand and falling prices. Restoration of fresh supplies into the market is also likely to pressure prices.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply