- Semi-finished steel prices fall to lowest level in 6 months

- Mandi market under pressure due to declining steel tags

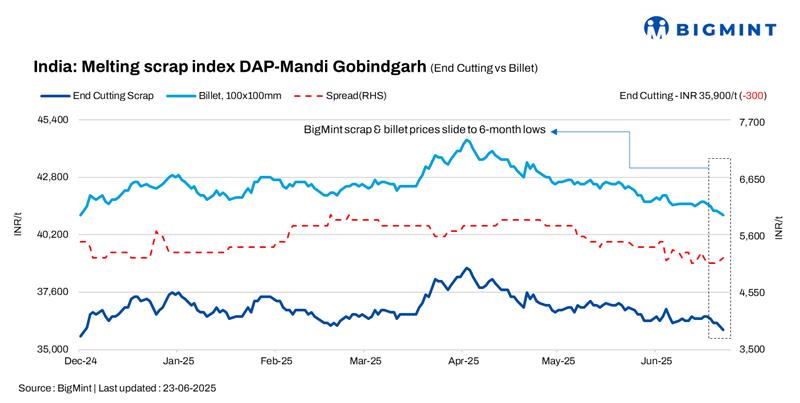

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 300/tonne (t) d-o-d to INR 35,900/t DAP on 23 June, 2025. Scrap prices have declined to a six-month low, revisiting levels last seen on 3 December 2024, amid continued market weakness.

The continued decline in both semi-finished and finished steel prices is exerting downward pressure on scrap suppliers, compelling them to consider reductions in prices to stay competitive.

A mill owner informed, “The Mandi Gobindgarh market is currently under pressure due to more competitive prices from neighbouring states for both semi-finished and finished steel. This regional competition is driving a day-on-day price decline, as mills are being forced to adjust their offers downward to remain in the market.”

Raw material prices

Sponge iron (CDRI) prices in Mandi witnessed a d-o-d correction of INR 100/t, settling at INR 28,900/t, reflecting easing demand and ongoing price pressure. Meanwhile, steel-grade pig iron prices in Ludhiana held firm at INR 35,800/t (DAP).

Steel market trends

Semi-finished steel prices slide across markets

Steel ingot prices in Mandi Gobindgarh declined by INR 300/t on a d-o-d basis, now at INR 41,000/t DAP. The downtrend aligns with a broader market movement, as semi-finished steel prices across major trading centers recorded a dip of INR 100-500/t. Notably, Ahmedabad reported the steepest correction with ingot prices slipping by around INR 500/t. Mandi ingot prices have now hit their lowest point in six months, a level last seen on 2 December 2024.

Rebar prices in Mandi drop to 9-month low

Rebar prices in Mandi Gobindgarh declined by INR 600/t day-on-day, settling at INR 45,700/t ex-works. The price correction is attributed to high inventory levels and a lack of active buying interest, prompting mills to reduce their offers. This marks the lowest price in nine months, last recorded on 19 September 2024.

Overview of Jalna market

In the Jalna market in western India, billet and rebar prices remained steady at INR 39,400/t and INR 43,500/t, respectively, while HMS 80:20 prices declined by INR 100/t to INR 30,500/t. Persistent rainfall has disrupted finished steel trade in the region, prompting mills to optimise production by maintaining a 50:50 charge mix of scrap and sponge iron. Additionally, scrap arrivals at mills have slowed, largely due to lower bid prices from buyers.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,000-5,400/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $338-342/t, which equates to approximately INR 31,858/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable at INR 30,500/t DAP. Indicative prices of shredded from Europe stood at $360-365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,800/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply