- Sponge iron prices dip INR 200/t d-o-d

- Semis, finished steel prices drop

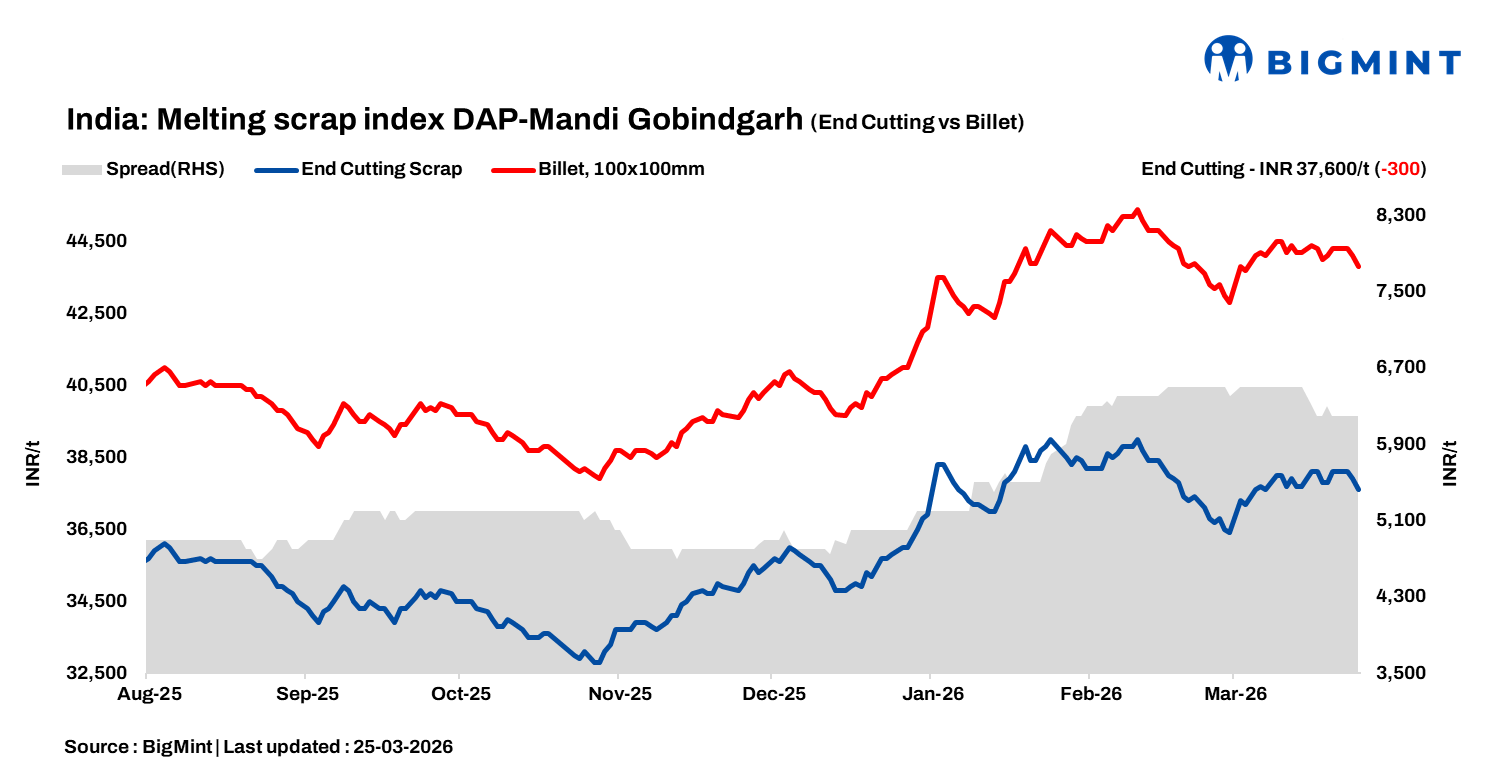

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, softened by INR 300/tonne (t) d-o-d to INR 37,600/t DAP on 25 March 2026. Scrap prices in the region declined by INR 300-400/t d-o-d. Today, scrap arrivals in Mandi Gobindgarh were slightly better compared to the last few days. However, on account of weak and soft demand in the semi-finished and finished steel segments-where prices eased by INR 200-300/t-mills refrained from paying premium rates for scrap. As a result, sellers reduced their offers today.

A mill owner informed, “Scrap prices may remain under pressure in the near term due to weak steel demand and slight improved supply.”

Alternative raw material prices

The alternative metallics segment mirrored a cautious trend. Sponge iron (CDRI) prices in Mandi Gobindgarh fell by INR 200/t to INR 32,400/t DAP, reflecting subdued demand. Meanwhile, steel-grade pig iron prices in Ludhiana remained stable at INR 39,700/t DAP, with limited buying activity

Steel market trends

Ingot prices in Mandi Gobindgarh declined by INR 200/t to INR 43,800/t DAP on reduced transaction volumes. Rebar (Fe500) prices fell by INR 200/t to INR 49,400/t ex-works, while HR strip prices softened by INR 100/t to INR 45,800/t ex-works. Market participants reported that subdued offtake restricted aggressive bookings, keeping procurement largely need-based. Weak downstream demand weighed on steel prices, further impacting scrap sentiment.

Overview of Mumbai market

Rebar (Fe 500) prices on the Mumbai IF market declined by around INR 300/t, settling near INR 50,600/t ex-works. Buying activity remained moderate, with limited transactions observed, but showed some improvement compared to the past few sessions as the recent price correction encouraged enquiries. Market sentiment continued to be cautious, keeping procurement largely need-based. Despite the relatively subdued trading activity, mills have largely held their offer levels. Supported by elevated raw material costs, any sharp downside in prices appears unlikely in the near term.

On the raw material side, HMS (80:20) scrap was assessed at INR 34,300/t DAP, with the scrap-billet conversion spread hovering around INR 9,800/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,900-6,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $365/t, approximately INR 36,612/t (inclusive of freight). HMS (80:20) prices in Mumbai decreased by INR 200/t d-o-d to INR 34,300/t DAP. Indicative prices of shredded from Europe stood at $386/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,950/t.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply