- Sponge iron prices decrease by INR 280/t w-o-w

- Finished steel prices remain steady w-o-w

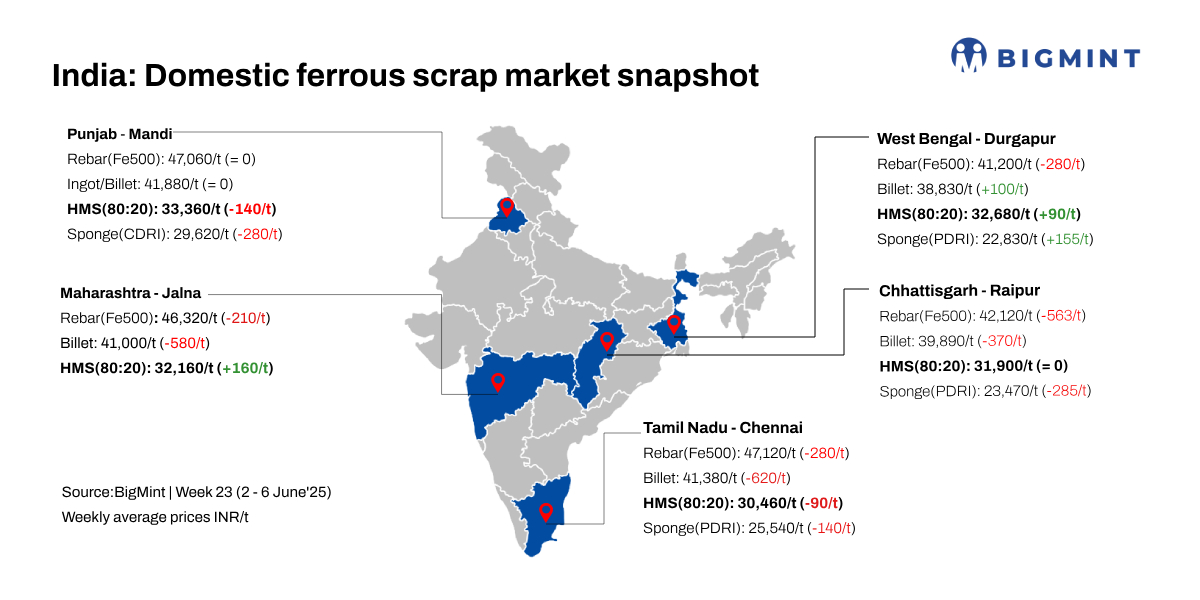

BigMint’s domestic end-cutting scrap index for the Mandi Gobindgarh market remained stable w-o-w, despite minor fluctuations driven by scrap shortages, subdued steel demand, and ongoing GST inspections. However, the index dropped by INR 350/t d-o-d to INR 36,500/t DAP on 6 June 2025.

In today’s trading session, market activity remained muted with limited inquiries from buyers. Despite a slight shortage of scrap, subdued demand for both semi-finished and finished steel kept purchase volumes restricted to moderate or strictly need-based levels. Additionally, with the ongoing scrap shortage and a noticeable gap between bids and offers, mills in the Mandi market have increased their procurement of sponge iron to support production.

A steel mill source in Mandi informed, “The beginning of the week brought significant financial pressure, as mills are burdened with essential liabilities such as electricity bills, labour wages, and other operational expenses. This strain is further compounded by the persistent challenge of low conversion margins that the secondary steel mills are facing over the past three-four years. With sluggish demand in the steel market adding to the woes, maintaining operational expenses has become increasingly difficult for mill owners.”

Bulk scrap arrivals

India witnessed two significant bulk scrap arrivals this week. A vessel carrying around 35,000 t of steel scrap docked at Kandla Port, Gujarat, comprising approximately 17,000 t of HMS and 17,000 t of shredded scrap.

Meanwhile, another bulk vessel arrived at Chennai Port in south India, delivering an estimated 27,000 t of steel scrap during the current week. (Cargo details are yet to be confirmed, but if verified, the arrival could impact short-term market sentiment and supply dynamics.)

Raw material prices

Sponge iron (CDRI) prices in Mandi remained stable d-o-d at INR 29,500/t while, w-o-w, prices decreased by INR INR 280/t. The availability of sponge iron in the Mandi market has increased steadily over the past two weeks. Mills are currently using a mix of raw materials for steel production-approximately 75% of scrap and 25% sponge iron.

Steel-grade pig iron prices in Ludhiana remained stable d-o-d and w-o-w at INR 36,000/t DAP.

Steel market trends

In Mandi Gobindgarh, steel ingot prices slipped INR 200/t d-o-d, reaching INR 41,700/t DAP. Similarly, semi-finished steel prices across major trading hubs recorded a decline of INR 100-300/t d-o-d. However, prices in the Mandi market remained largely stable on a weekly basis, supported by limited trading activity.

Rebar prices in Mandi declined by INR 100/t, settling at INR 41,700/t ex-works. However, w-o-w, prices remained largely stable as mills continued to face sales pressure.

Upcoming scrap auctions

For more details:https://www.bigmint.co/tenders/ferrous

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,100-5,400/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $344-345/t, which equates to approximately INR 31,778/t (including freight). Today, local HMS (80:20) prices in Mumbai fell by INR 200/t to INR 31,500/t DAP. Indicative prices of shredded from Europe stood at $365-$366/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,300/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply