- Scrap arrivals from neighbouring states remain slow

- Limited imports also contribute to tight scrap supply

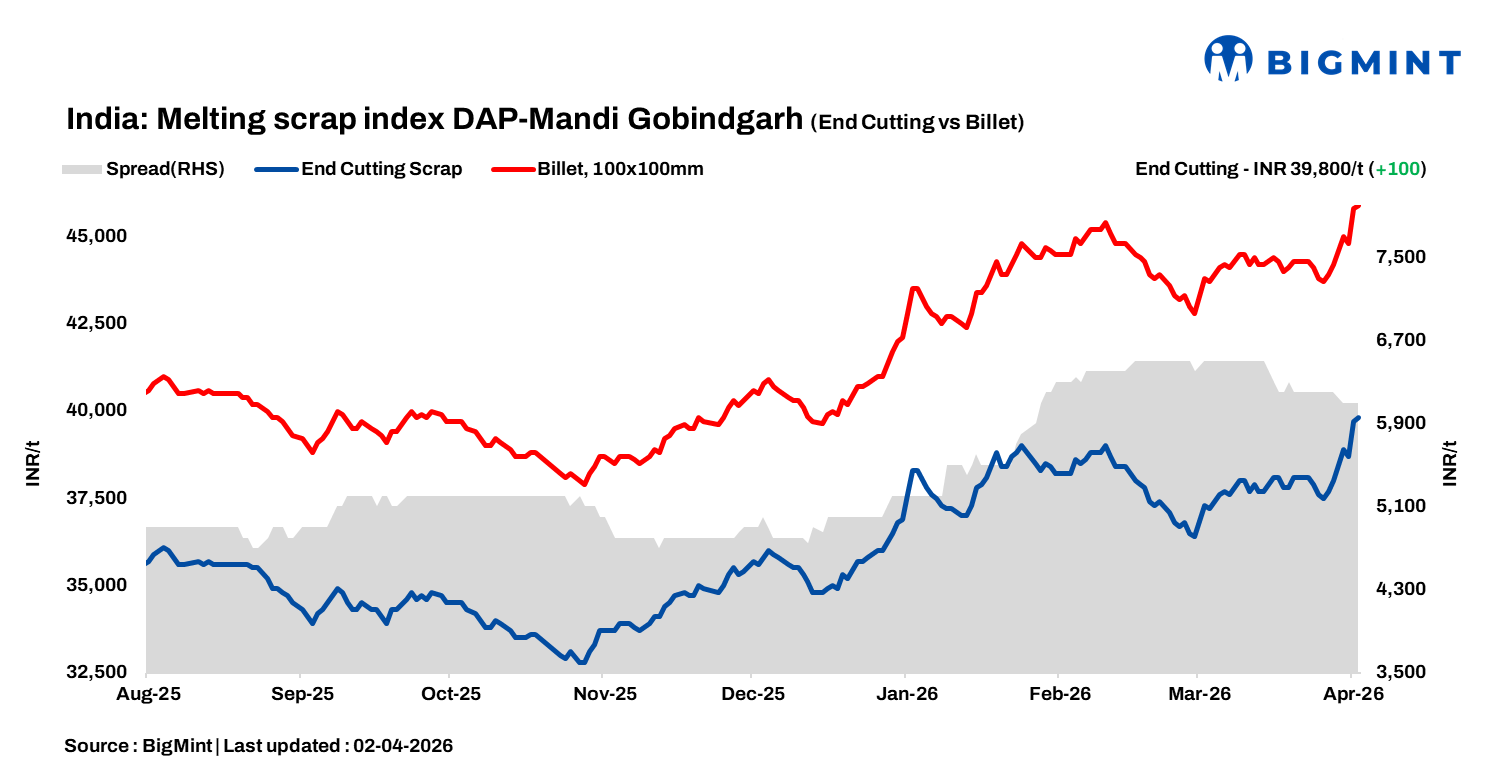

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, inched up by INR 100/tonne (t) d-o-d to INR 39,800/t DAP on 2 April 2026. The Mandi Gobindgarh steel market witnessed a moderately firm trend today, with mills continuing to procure scrap in decent volumes amid ongoing material shortages, while finished steel prices and demand also improved compared to previous sessions, lending support to prices and keeping overall market sentiment positive.

A mill owner informed BigMint, “Scrap supply into Mandi Gobindgarh from neighbouring states remains tight at present, as the recent spike in steel prices has prompted many suppliers to hold back material in anticipation of further gains in the near term. At the same time, the pause in imported scrap arrivals is tightening overall availability, enabling local scrap sellers to raise offers and maintain a stronger pricing stance in the current market.”

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh remained stable d-o-d at INR 34,600/t. Meanwhile, steel-grade pig iron prices in Ludhiana moved up by INR 500/t to INR 43,300/t DAP.

Steel market trends

In Mandi Gobindgarh, semi‑finished steel (ingot) prices increased by INR 100/t d-o-d to INR 45,900/t DAP, reflecting moderate demand, while ingot prices in other key production hubs rose by INR 100-900/t d-o-d. Rebar (Fe500) prices in Mandi Gobindgarh gained INR 300/t to INR 51,600/t exw today, whereas HR strip (patra) prices remained unchanged at INR 47,100/t exw.

Overview of Mumbai market

Rebar (Fe 500) prices on the Mumbai IF route remained stable d-o-d at around INR 53,400/t ex-works, following sharp fluctuations observed in recent sessions. Buying activity was moderate, with market participants largely adopting a wait-and-watch approach, resulting in limited but steady enquiries.

Procurement continued to be strictly need-based, reflecting cautious sentiment across the market. Meanwhile, support from elevated raw material costs and tight scrap availability is expected to keep prices firm, with limited scope for any significant downside in the near term. On the raw material side, HMS (80:20) scrap was assessed at INR 35,700/t DAP, with the scrap-billet conversion spread at around INR 1,200/t.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,900-6,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $380/t, approximately INR 37,668/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 35,700/t DAP. Indicative prices of shredded from Europe stood at $400/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,800/t.

Leave a Reply