- Sponge iron prices increase by 0.3% to INR 100/t

- Semi-finished steel prices surge by 0.7% to INR 300/t

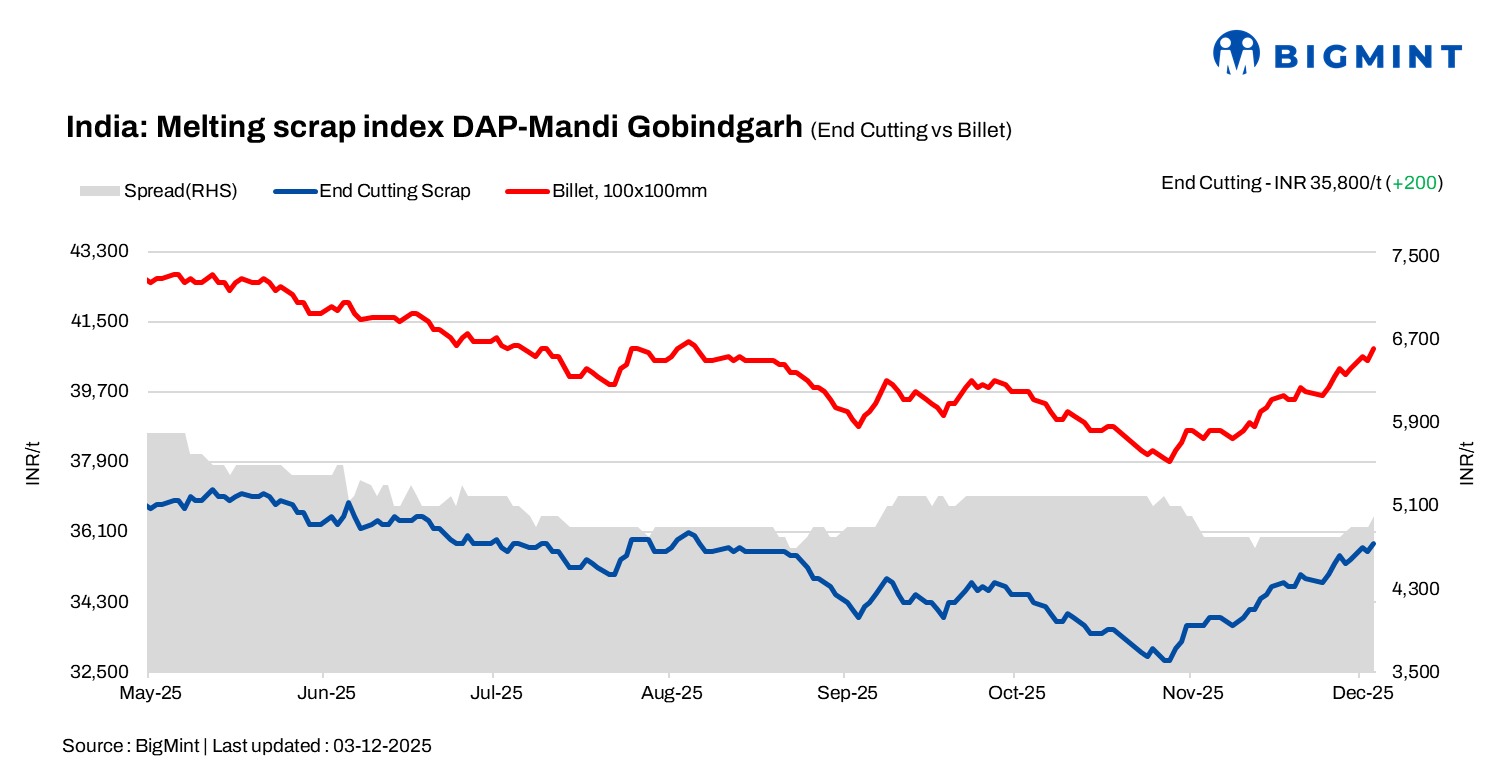

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by about 0.6% (INR 200/tonne) d-o-d to INR 35,800/t DAP on 3 December. The Mandi Gobindgarh market experienced price gains throughout both trading sessions on Wednesday in semi-finished steel, but finished steel demand was moderate because of an evident scrap scarcity in the midstream. This supply bottleneck is causing upward pressure on prices in other steel categories, reflecting a sentiment where price hikes are outpacing demand increases.

“Slightly subdued demand for patra in the Mandi market, in contrast to strengthening TMT demand fueled by infrastructure growth and construction activity. Patra mills are under significant strain from conversion losses, prompting production cuts at multiple facilities. Scrap shortages are worsening the situation, with imported scrap purchases remaining low due to unfavorable pricing from a rising dollar and falling INR, thereby tightening overall supply,” a mill owner told BigMint.

Raw material

Sponge iron(CDRI) prices in Mandi rose by INR 100/t to 29,300/t DAP. Meanwhile, steel grade pig iron prices in Ludhiana also held steady at INR 34,900/t DAP.

Steel market

In Mandi Gobindgarh, semi-finished steel (ingot) prices rose by about 0.7% (INR 300/t) day-on-day to INR 40,800/t DAP, with intraday gains of between INR 100-300/t across major hubs.

Rebar (Fe500) prices remained stable d-o-d at INR 45,200/t ex-works, while HR strip (patra) prices also remained flat INR 41,200/t ex-works. Demand remains moderate in the region, limited to routine trades, with moderate price movements expected in the near term.

Overview of Mumbai market

The price of Fe 500 Rebar on the Mumbai IF route has climbed by INR 300/t, setting the new ex-works (exw) prices at INR 43,700/t. This price appreciation is attributed to a combination of good market demand from both the retailer and large-scale project segments, coupled with healthy dispatch activity of materials booked previously. On the raw material front, HMS (80:20) scrap was assessed at INR 30,300/t DAP, while the scrap–billet conversion spread stood at around INR 9,200/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,800-5,100/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $316-$318/t, approximately INR 30,882/t (inclusive of freight). HMS (80:20) in Mumbai remained stable at INR 30,300/t DAP. Indicative prices of shredded from Europe stood at $345/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,000/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply