- Lack of GST cuts prompts suppliers to raise offers

- Finished steel prices rise by INR 400-970/t w-o-w

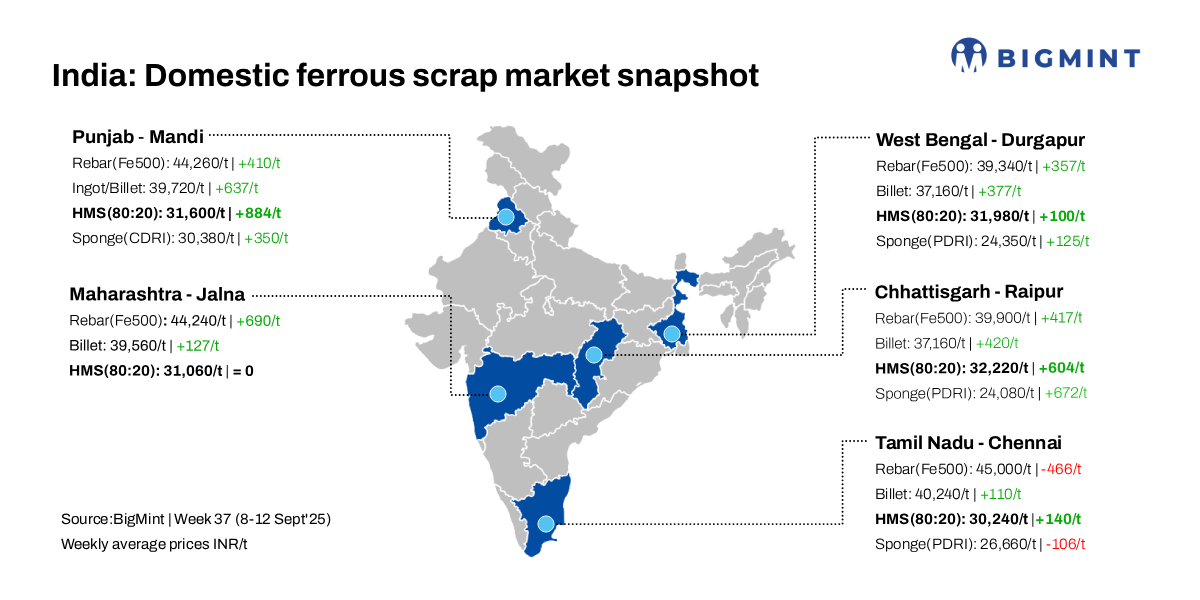

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained flat d-o-d at INR 34,300/tonne (t) DAP on 12 September 2025. However, w-o-w, scrap prices increased by INR 350-885/t, with the end-cutting scrap index gaining INR 350/t.

The Mandi Gobindgarh steel market witnessed a quiet session today, with no significant trading activity seen in the finished segment. As a result, prices declined by INR 100-200/t. Meanwhile, scrap prices remained unchanged d-o-d, indicating a stable but cautious market sentiment.

The beginning of Week 37 brought a much-needed respite to the steel trade in Mandi Gobindgarh, following the government’s clarification that there would be no reduction in GST on steel scrap, which remains steady at 18%. This announcement helped restore a degree of confidence among market participants, prompting suppliers to raise their offers and triggering a phase of active short-term buying in the region.

Imported scrap offers

Alternative raw materials

In Mandi Gobindgarh, sponge iron prices saw a d-o-d decline of INR 100/t, settling at INR 30,200/t DAP. Despite this dip, the market posted a w-o-w gain of INR 350/t, indicating underlying strength in demand or supply adjustments.

Meanwhile, the pig iron market in Ludhiana remained unchanged, at INR 35,400/t, on both d-o-d and w-o-w bases, reflecting a stable trading environment with no significant fluctuations.

Steel market trends

The semi-finished steel market in Mandi Gobindgarh remained largely stable, with prices assessed at INR 39,500/t DAP, showing no major d-o-d fluctuations. In contrast, steel ingot prices in key production centres witnessed a moderate increase of INR 100-300/t, reflecting slight upward momentum in localised demand.

In the finished steel segment, rebar (Fe500) prices in Mandi registered a d-o-d decline of INR 100/t to INR 44,100/t ex-works. Despite this dip, prices recorded a w-o-w gain of INR 410/t, indicating some underlying support earlier in the week.

Meanwhile, HR strip (patra) prices also saw a d-o-d drop of INR 200/t to INR 42,600/t ex-works, suggesting continued demand weakness. However, on a w-o-w basis, patra prices in Mandi showed a notable increase of INR 967/t, driven by earlier short-term buying interest.

Overview of Durgapur steel market

In the Durgapur market of eastern India, billet prices inched up by INR 100/t d-o-d to INR 36,900/t. HMS 80:20 and rebar prices remained stable, assessed at INR 31,900/t and INR 39,200/t, respectively. According to sources, improved billet demand from Mandi Gobindgarh and Jharkhand supported current prices. However, finished steel demand within the local market remained moderate.

Upcoming scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 4,900-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $331/t, which equates to approximately INR 31,421/t (including freight). HMS (80:20) prices in Mumbai remained stable at INR 31,300/t DAP today. Indicative prices of shredded from Europe stood at $363/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,950/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply