- GST checks disrupt raw material procurements

- Steel inventory remains on higher side in Mandi

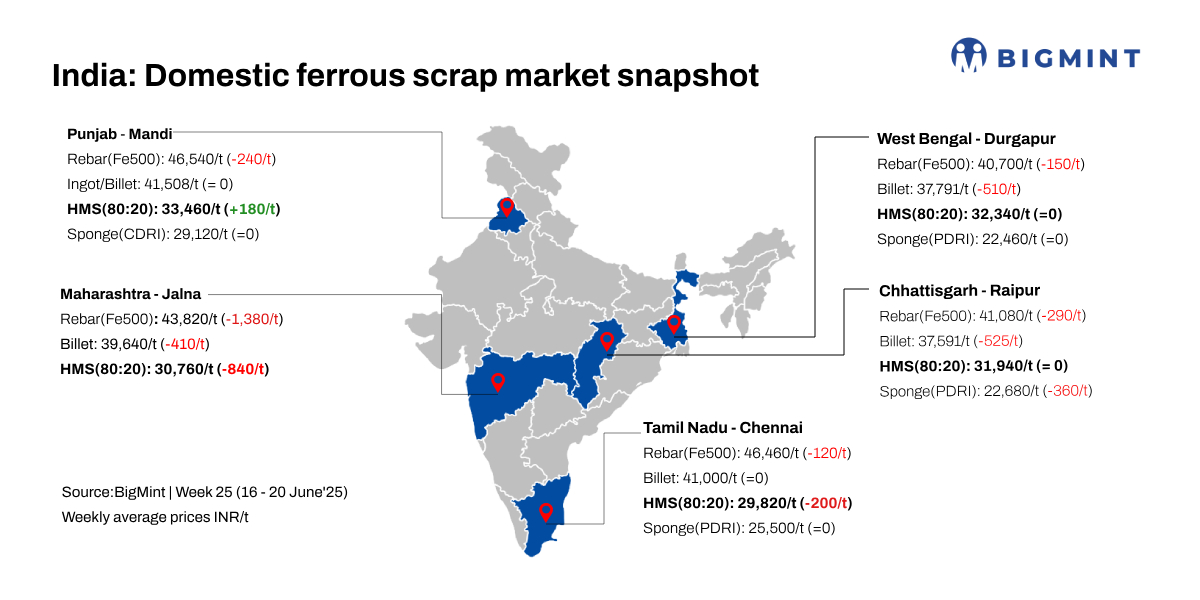

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained largely stable w-o-w, barring minor fluctuations in scrap prices, amid subdued steel demand. However, the index decreased by INR 200/tonne (t) d-o-d to INR 36,200/t DAP on 20 June 2025.

In today’s trading session, market activity remained subdued, with limited inquiries from buyers. While ongoing GST raids have resulted in a noticeable shortage of scrap, the overall demand for both semi-finished and finished steel products remained muted. This led to cautious and largely need-based buying, with transaction volumes staying at moderate levels.

A mill owner informed: “Despite the current slowdown, market sentiment among mills remains cautiously optimistic. Industry participants expect price movements to remain range-bound in the near term, with ingots likely to hover between INR 41,000-42,000/t in the coming week.”

Another mill owner informed: “The availability of competitively priced semi-finished steel from neighbouring states continues to pose a threat to local market sentiment, as buyers explore viable outsourcing options to manage cost efficiency. In the Mandi steel market, inventory levels remain on the higher side. This is contributing to sales pressure for mills, which in turn is creating liquidity challenges across segments. With demand not picking up pace, mills are finding it increasingly difficult to clear stock at expected margins.”

Additionally, a persistent gap between scrap suppliers’ price expectations and buyers’ bid levels is adding to market uncertainty. This mismatch is signalling cautious sentiment and underlining the need for realignment between input cost and finished product pricing.

Raw material prices

Sponge iron (CDRI) prices in Mandi remained stable d-o-d and w-o-w at INR 29,120/t DAP.

Steel-grade pig iron prices in Ludhiana dropped by INR 200/t d-o-d to INR 35,800/t DAP. W-o-w, prices saw a minor decline of INR 150/t.

Steel market trends

In Mandi Gobindgarh, steel ingot prices decreased by INR 100/t d-o-d to INR 41,300/t DAP. Similarly, semi-finished steel prices across major trading hubs saw a downtrend of INR 100-400/t d-o-d. Semi-finished steel prices in Mandi remained steady w-o-w amid limited trades.

Rebar prices in Mandi fell by INR 100/t d-o-d to INR 46,400/t exw. However, w-o-w, prices saw a drop of INR 240/t due to a slowdown in steel demand.

Upcoming ferrous scrap auctions

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,000-5,400/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $340-345/t, which equates to approximately INR 32,056/t (including freight). Today, local HMS (80:20) prices in Mumbai remained stable at INR 30,500/t DAP. However, on a w-o-w basis, prices declined by INR 700/t. Indicative prices of shredded from Europe stood at $360-$365/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,950/t

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply