- Slow scrap arrivals allow sellers to keep offers firm

- LNG shortages may force mills to cut steel production

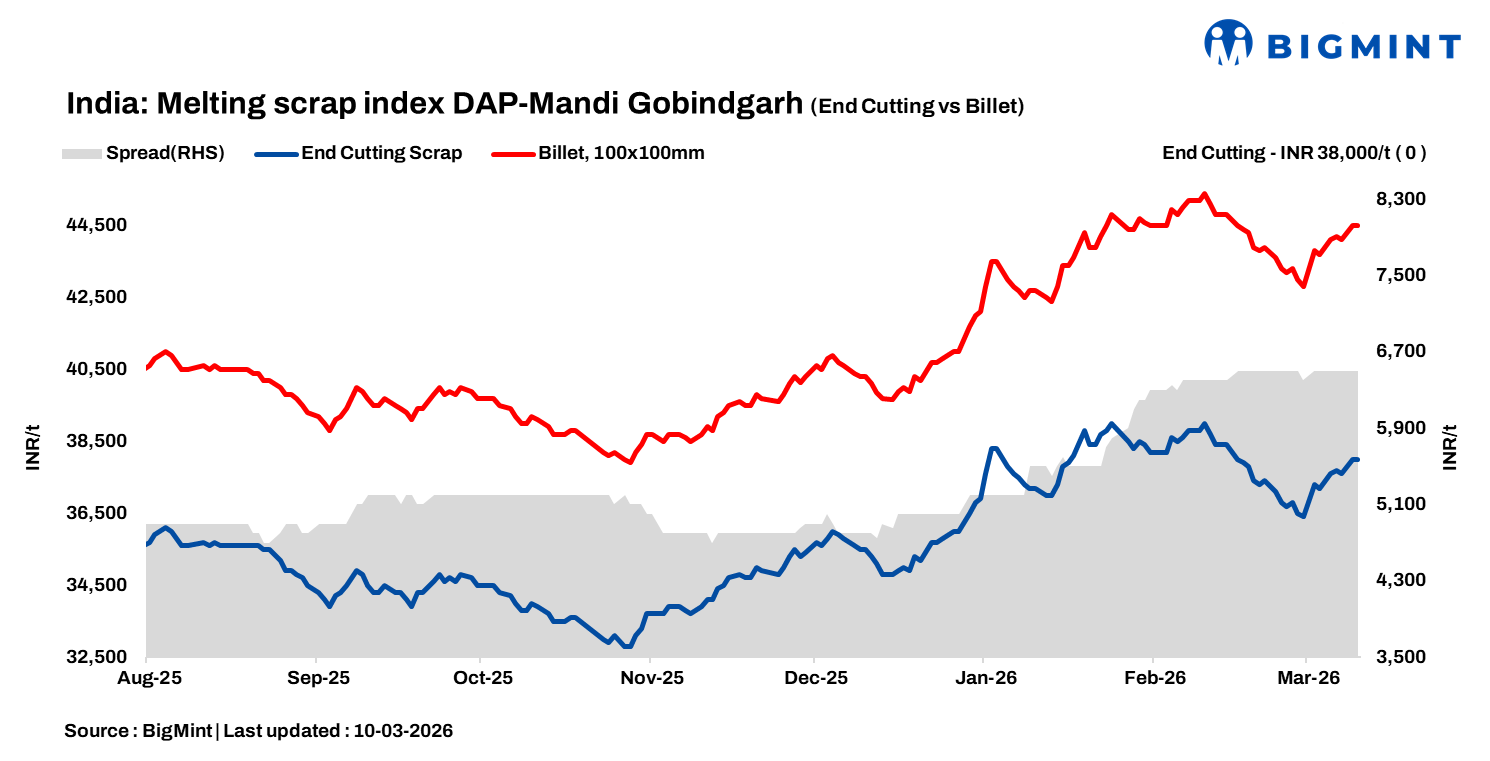

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained unchanged d-o-d at INR 38,000/tonne (t) DAP on 10 March 2026. In Mandi Gobindgarh, a key Indian secondary steel hub, the steel market showed moderate demand with mills procuring scrap in decent volumes; slow recent arrivals allowed sellers to keep offers firm today, while semi-finished and finished steel demand eased slightly from yesterday’s session.

A major mill informed BigMint, “Most rolling mills are using liquefied natural gas (LNG) for operations. However, authorities have approved only 50% of the required supply.” This limited LNG availability may force mills to cut production in the short term, potentially tightening finished steel supply and supporting upward price momentum in the coming days.

Alternative raw material prices

In Mandi Gobindgarh, sponge iron (CDRI) prices fell by INR 100/t d-o-d to INR 32,800/t DAP, while steel-grade pig iron prices in Ludhiana remained unchanged at INR 40,300/t DAP.

Steel market dynamics

Semi-finished steel prices in Mandi Gobindgarh inched up by INR 50/t d-o-d to INR 44,550/t DAP.

In the rebar (Fe500) segment, prices climbed INR 200/t d-o-d to INR 49,600/t ex-works. Buying interest stayed moderate in the region. HR strip (patra) prices also rose by INR 200/t to INR 46,700/t ex-works today.

Overview of Jalna market

The Jalna market in western India witnessed a mild d-o-d rise in steel prices, with billet and rebar edging up by INR 100/t to INR 45,100/t and INR 51,600/t, respectively. HMS (80:20) prices, however, witnessed a sharper increase of INR 600/t to INR 32,900/t. Market participants noted that finished steel trading activity has strengthened in recent days, which has supported the upward movement in steel prices. Rebar prices recorded a w-o-w increase of around INR 800/t. Amid improved demand conditions, mills raised their scrap purchase prices to ensure adequate material availability for production.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 6,300-6,600/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $360-$362/t, approximately INR 35,589/t (inclusive of freight). HMS (80:20) prices in Mumbai increased by INR 100/t d-o-d to INR 34,000/t DAP. Indicative prices of shredded from Europe stood at $382/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,400/t.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply