- Raw material prices improve by INR 200-300/t

- Semis, finished tags increase by INR 200-600/t

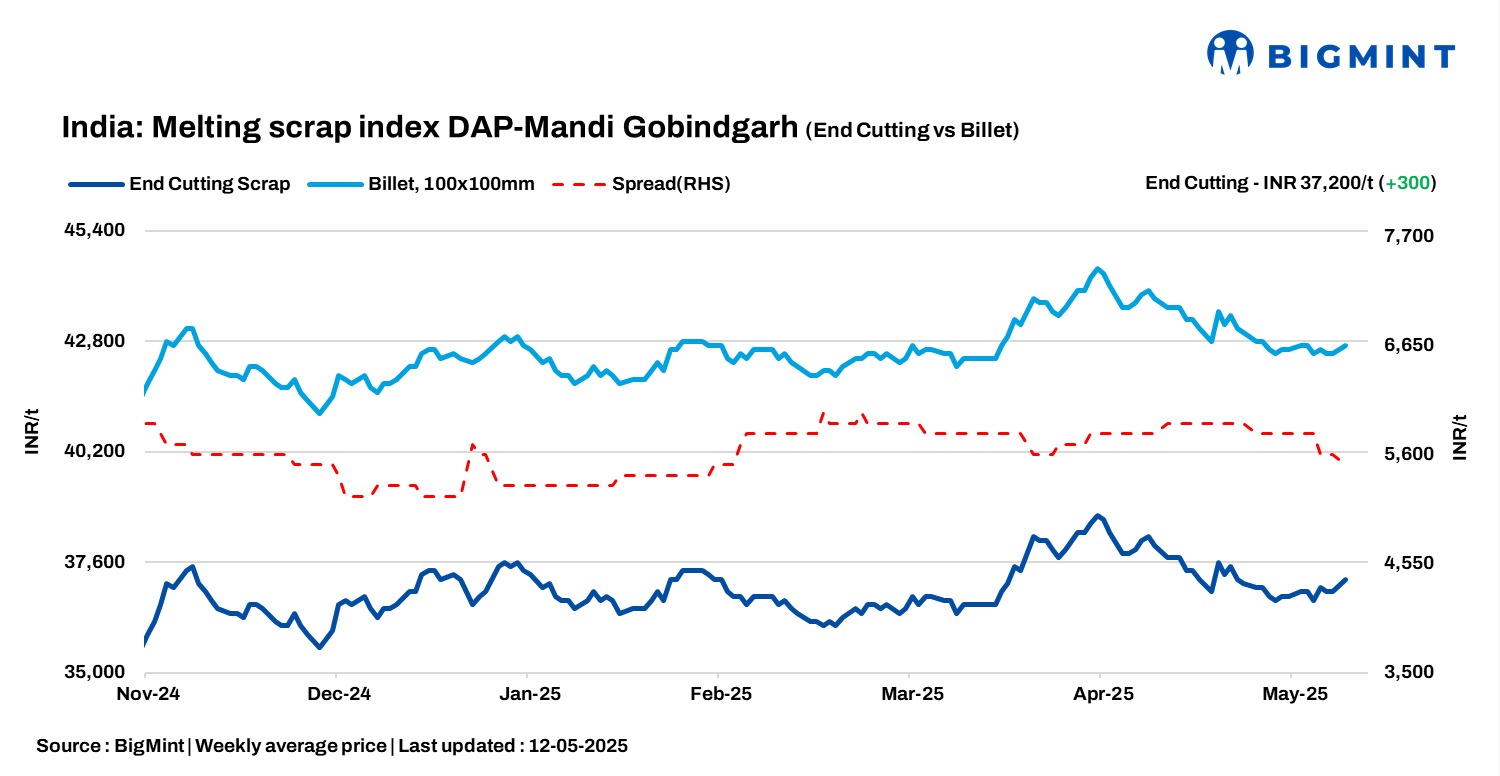

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, improved marginally by INR 300/tonne (t) d-o-d to INR 37,200/t DAP on 12 May 2025, as semi-finished steel prices inched up amid moderate market sentiments.

A Mandi-based mill owner informed BigMint, “The steel market was steady today, with no major change in trade volumes. A slight increase in buyer interest points to a stable but cautiously upbeat sentiment. With slow trading, prices are likely to stay flat unless demand or raw material prices see significant shifts.”

Another steelmaker stated, “Steel trade activity in the Mandi region resumed after a 3-4 day pause caused by geopolitical tensions along the borders, with basic buying interest showing signs of improvement and resulting in a slight uptick in prices. However, market sentiment remains cautious due to ongoing sales pressure and liquidity challenges across major regions, which are likely to keep price movements within a narrow range in the near term. A minor shortage of scrap has also been observed, potentially adding to supply-side concerns, but overall, no significant fluctuations are expected unless there are major shifts in demand or raw material availability.”

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi increased by INR 300/t d-o-d to INR 30,600/t DAP. Similarly, steel-grade pig iron prices in Ludhiana rose by INR 200/t to INR 36,600/t DAP.

Steel market trends

In Mandi Gobindgarh, steel ingot prices improved by INR 300/t d-o-d to INR 42,700/t DAP. Meanwhile, semi-finished steel prices across major trading hubs climbed higher by INR 100-600/t d-o-d, supported by steady buying interest and marginal improvement.

On the other hand, rebar (Fe 500) prices in Mandi increased by INR 200/t d-o-d to INR 47,800/t exw. Similarly, HR strip (patra) prices in the region jumped by INR 600/t d-o-d to INR 44,500/t exw. In the finished steel market, tags saw an upward movement; however, trade activity remained moderate to below moderate, reflecting cautious buyer sentiment despite the price rise.

Overview of Jalna market

In the Jalna steel market (western India), billet prices increased by INR 600/t d-o-d to INR 42,900/t. Meanwhile, rebar and HMS 80:20 prices remained unchanged d-o-d at INR 48,500/t and INR 32,700/t, respectively. Despite the billet price increase, finished steel trading slowed relative to the prior session, though scrap supply to mills remained consistent without any disruptions.

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,400-5,800/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $345-350/t, which equates to approximately INR 31,909/t (including freight). Local HMS (80:20) prices in Mumbai remained steady at INR 33,000/t DAP. Indicative prices of shredded from Europe stood at $365-370/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,750/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply