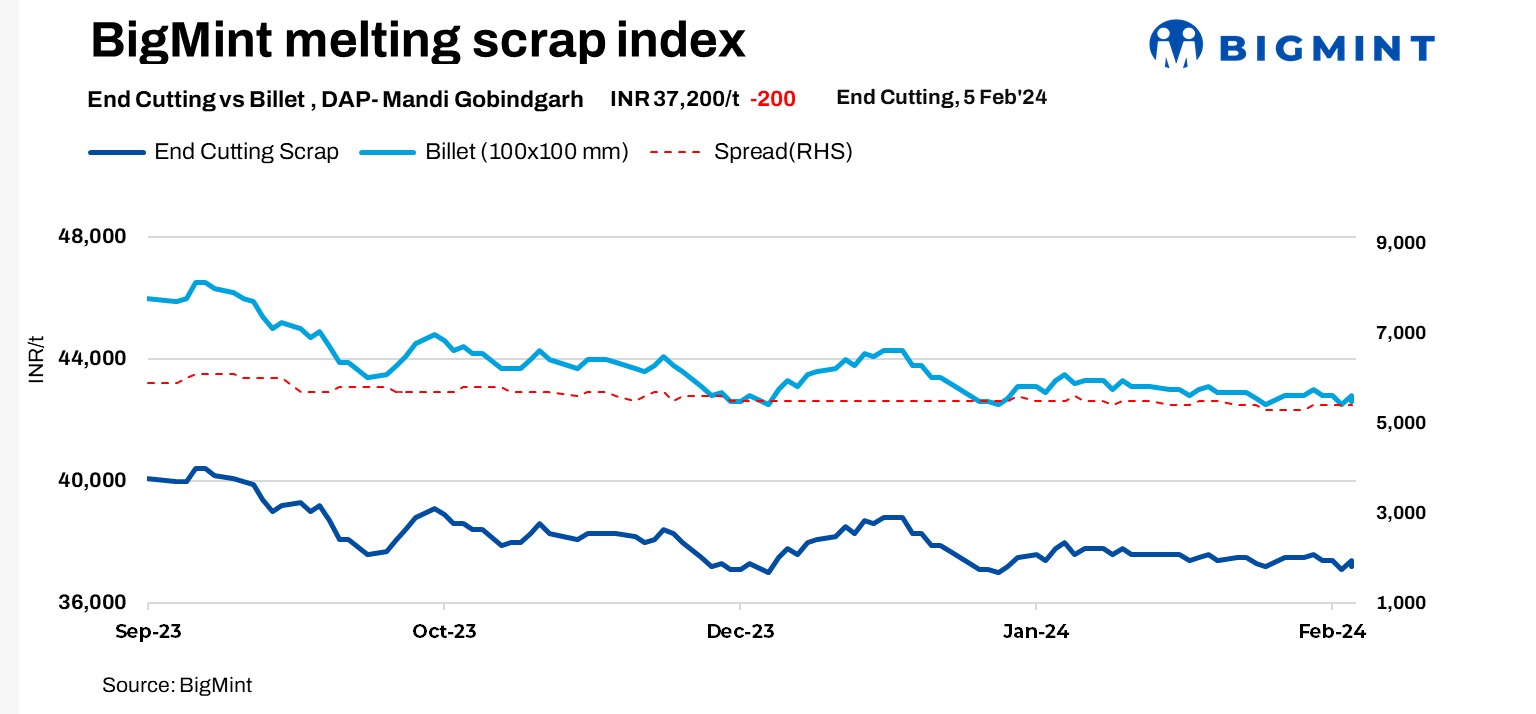

BigMint’s index for domestic steel scrap (end-cutting) in Mandi Gobindgarh recorded a drop of INR 200/t on 5 February, 2024, reaching INR 37,200/t on a delivered-at-plant (DAP) basis. The mills in Mandi are acquiring domestic scrap at a subdued level today, aligning with the sluggish activity observed in the finished steel market.

A trader said : “Scrap suppliers are encountering challenges in procuring scrap amid slow trade activity in both semi-finished and finished steel, coupled with fluctuating market conditions. Mills are demanding scrap at lower levels, while suppliers are facing higher scrap prices. Additionally, a slight shortage of scrap is observed in the market today.”

In Mandi, prices of steel ingots experienced a decline of INR 200/t, settling at INR 42,600/t at the time of reporting and price normalisation. Concurrently, prices in various significant markets saw a decrease ranging from INR 100/t to INR 200/t today.

Raw materials price update

In Mandi, the price of sponge iron (CDRI) saw a reduction of INR 100/t, settling at INR 31,100/t. At the same time, pig iron (steel grade) prices in Ludhiana remained unchanged at INR 39,500/t on a delivered-at-plant (DAP) basis.

Overview of other markets

Alang: Ship-breaking melting scrap prices in Alang, Gujarat, remained stable d-o-d on 5 February, 2024. As per BigMint’s assessment, HMS (80:20) prices stood at INR 34,000/t exy. Almost stable semi-finished steel prices in Gujarat in the last trading session and moderate buying inquiries for scrap in the region prompted scrap suppliers to keep offers firm today.

Jalna: In the Jalna market, situated in western India, semi-finished, finished steel and HMS 80:20 prices prices remained steady and were assessed at INR 42,300/t, INR 48,000/t and INR 32,500/t. Trade movements in finished steel were restricted in today’s trading session.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic Vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $385-$400/t, which equates to approximately INR 35,000/t(including freight),while local scrap-HMS(80:20) prices in Mumbai remained stable at INR 32,500/t d-o-d.

In India, demand for imported scrap continued to remain sluggish today, primarily due to a notable disparity between bids and offers. Indicative offers for shredded scrap from Europe were in the range of $415-420/t CFR Nhava Sheva.

An official from a steel mill commented on the current market conditions, stating, “The market is currently slow, with no buyers showing interest in booking shredded scrap or even inquiring about offers due to perceived unviable prices.”

A representative from a trading company further added, “It has been a considerable amount of time since we last made purchases in India. However, the challenges arise as finished steel sales are not providing sufficient support, creating an environment where it seems unlikely for inquiries to increase in India this week.”

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,000/t.

To see SteelMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.