- Sponge iron prices dip by INR 200/t d-o-d

- Semis, finished steel prices fall by INR 100-200/t

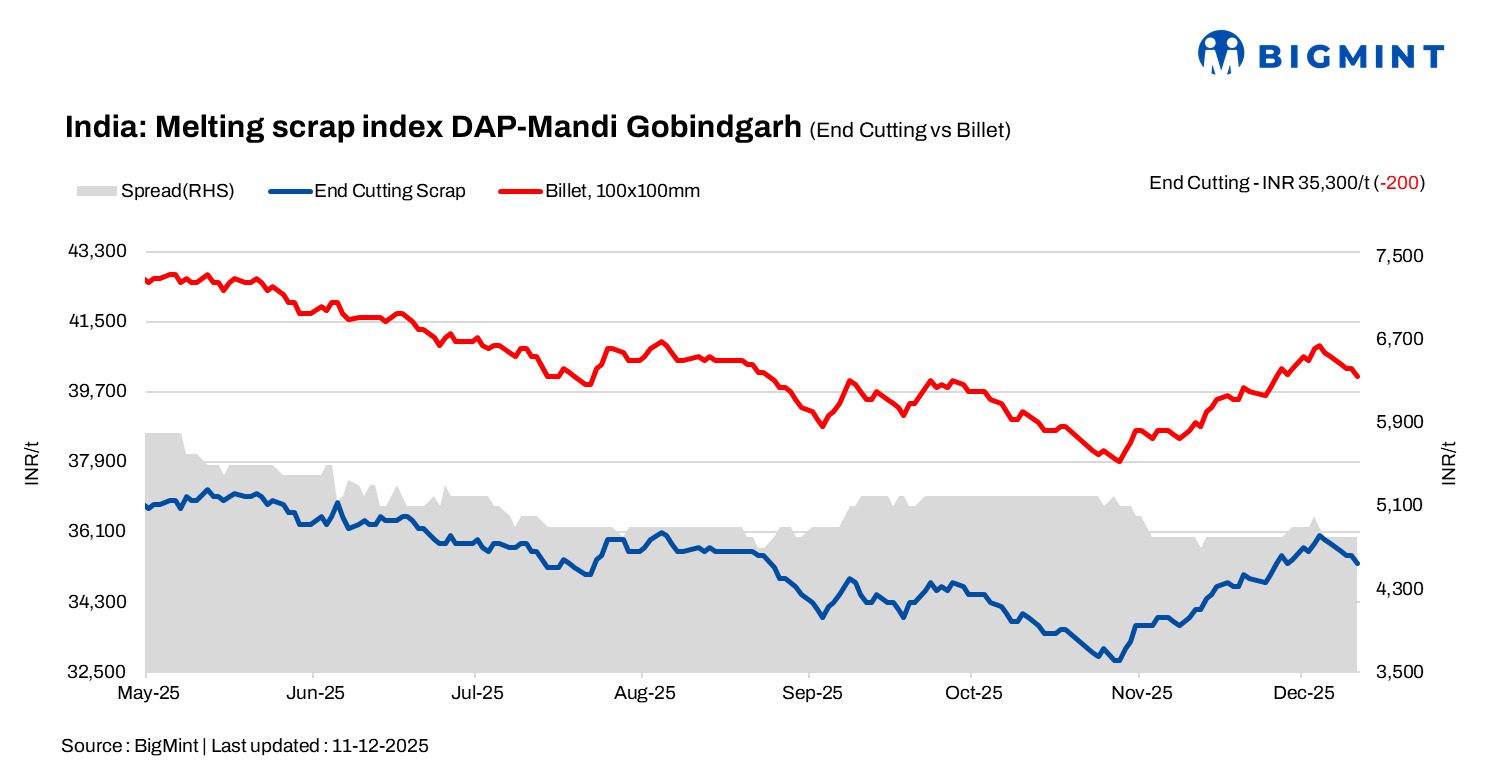

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, decreased by INR 200/tonne (t) d-o-d to INR 35,300/t DAP on 11 Dec 2025.

Scrap prices in Mandi Gobindgarh continued to decline on a sluggish and largely inactive steel market and muted buying interest. Mills are procuring scrap strictly based on immediate production needs. Although scrap supply has been slow, the overall situation remains manageable as medium-scale mills operate at 50-60% capacity utilization.

The imported scrap segment in Mandi remains subdued for a prolonged period, as buyers prefer domestic scrap due to its cost advantage. Imported scrap prices currently trade at a premium of INR 600-800/t compared to domestic offers, reinforcing the preference for local material in the steel manufacturing sector.

Raw material

Sponge iron (CDRI) prices in Mandi Gobindgarh declined by INR 200/t to INR 28,600/t DAP, while steel-grade pig iron tags in Ludhiana inched up by INR 100/t d-o-d to INR 34,800/t DAP.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh declined by INR 200/t d-o-d, settling at INR 40,000/t DAP. Other major production hubs also witnessed price drops in the range of INR 100-300/t during today’s trading session.

Rebar (Fe500) prices in Mandi Gobindgarh declined by INR 100/t to INR 44,800/t ex-works despite ongoing input cost pressures and inventory challenges. Over the past five days prices have dropped by INR 500/t in the region.

Meanwhile, HR strip (patra) prices softened by INR 100/t to INR 40,500/t ex-works. Over the last six days patra prices have fallen by INR 800 per ton, reflecting sustained weak demand.

Overview of Mumbai market

Rebar (Fe 500) prices on the Mumbai IF route slight increased by INR 100/t at INR 44,600/t exw, with limited trading activity as buyers have already procured enough material and waiting for further market direction. On the raw material front, HMS (80:20) scrap was assessed at INR 30,300/t DAP, while the scrap-billet conversion spread stood at around INR 9,100/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,700-5,000/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $318-$320/t, approximately INR 31,000/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 30,300/t DAP. Indicative prices of shredded from Europe stood at $348-350/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,450/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply