- Sponge iron prices decrease INR 200/t d-o-d

- Semis, finished steel prices decline INR 300-500/t today

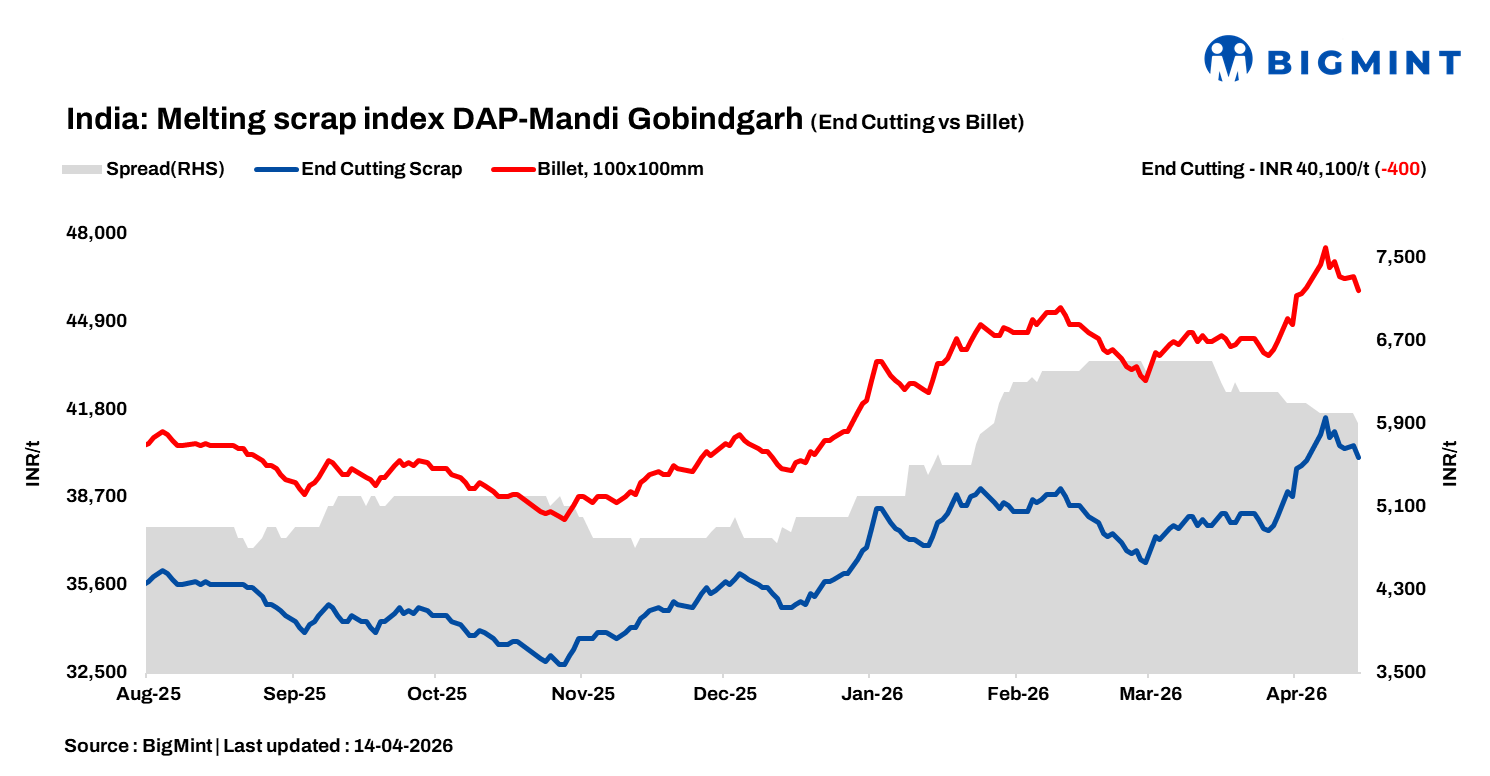

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 400/tonne (t) d-o-d to INR 40,100/t DAP on 14 April 2026. Trading activity in Mandi Gobindgarh’s secondary steel sector hit a standstill today as buyers retreated to the sidelines. This caution stems from ongoing sluggishness in the semi-finished and finished segments, where stagnant prices and weak demand have left the market without clear direction.

The Baisakhi festivities compounded this quietude, resulting in a practical market freeze. With mills throttling back production and scrap deliveries slowing to a trickle, local trade was confined to essential, “hand-to-mouth” restocking at current price levels.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh fell by INR 200/t d-o-d to INR 34,300/t amid limited demand. Meanwhile, steel-grade pig iron prices in Ludhiana remained stable d-o-d at INR 43,000/t DAP.

Steel market trends

In Mandi Gobindgarh, ingot prices declined by INR 500/t to INR 46,000/t DAP amid reduced transaction volumes, while other major production centers saw day-on-day drops of INR 150-900/t.

Rebar (Fe500) prices in Mandi eased INR 300/t to INR 52,100/t despite persistently weak trade, and HR strip (patra) prices dipped INR 500/t to INR 49,000/t ex-works. Overall, cautious buying and subdued demand kept market momentum low across key segments.

Overview of Jalna market

In the western India-based Jalna market, billet and HMS (80:20) scrap prices remained stable at INR 45,500/t and INR 34,300/t, respectively. Meanwhile, rebar prices declined slightly by INR 100/t to INR 53,100/t.

Market participants reported that trading activity in finished steel has slowed over the past couple of days, leading to softer demand sentiment. At the same time, scrap availability at mills remains adequate, with supplies aligning with current production requirements. This balanced supply situation has helped keep scrap prices stable despite weaker downstream demand.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,700-6,100/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $383-$384/t, approximately INR 37,940/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 35,700/t DAP. Indicative prices of shredded from Europe stood at $398-$399/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 16,100/t.

Leave a Reply