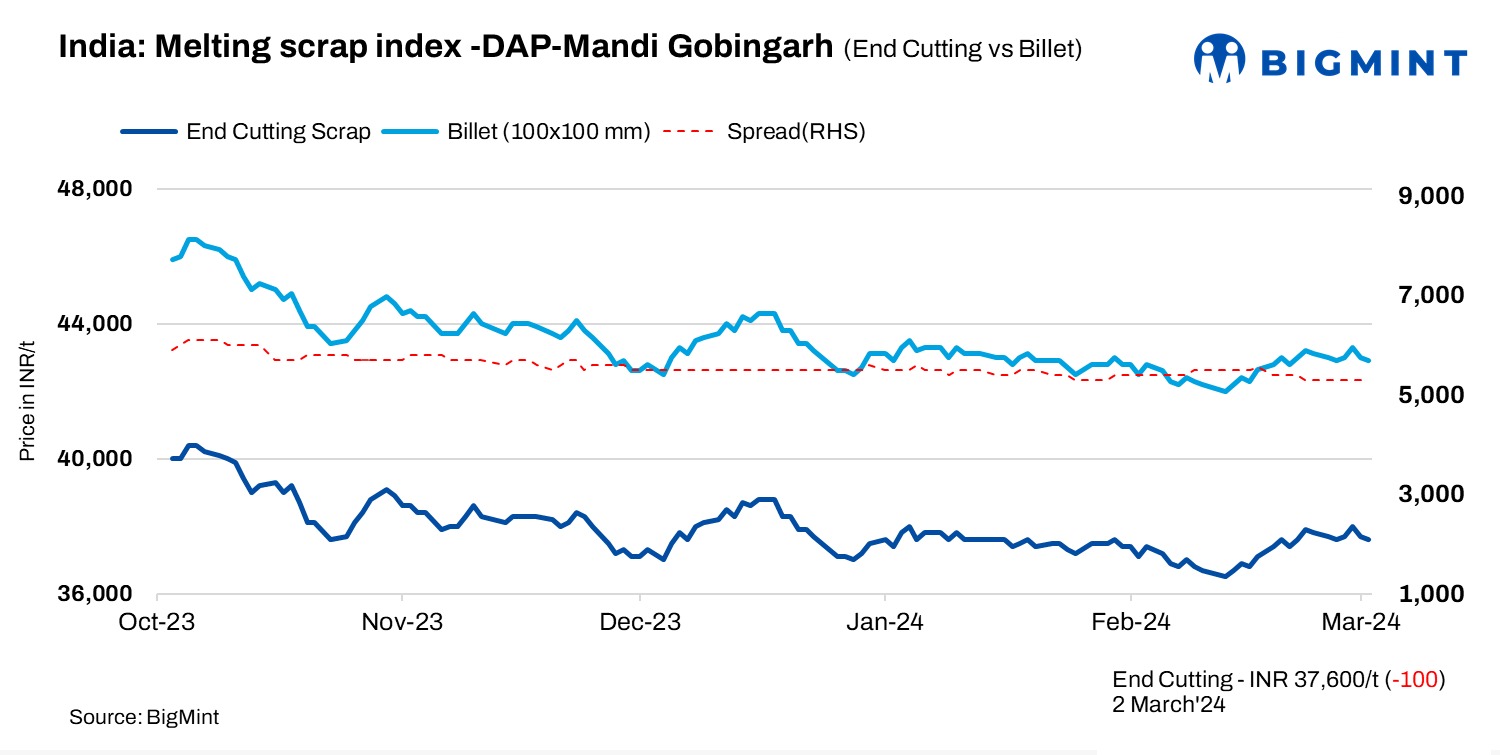

The latest update from BigMint on 2 March, 2024 revealed a price reduction in domestic end-cutting scrap at the Mandi Gobindgarh steel market. Prices saw a decrease of INR 100/t, settling at INR 37,600/t for delivery at the plant. In the region arrival of scrap was moderate, while mills procuring domestic scrap in decent levels.

Steel ingot prices in Mandi Gobindgarh saw a decrease of INR 150/t, reaching INR 42,850/t today during reporting and price normalisation. Likewise, several prominent markets also experienced a decline in prices ranging from INR 100/t to INR 200/t today. Rebar(Fe500) prices fell by INR 100/t to INR 47,600/t.

Weekly trend of Mandi

This week saw a noticeable slowdown in steel trading compared to the previous week. Prices experienced a minor decline across all steel segments, resulting in a more moderate overall activity in the mandi steel market. Steel mills are anticipating that in near future it will continue this trend, with prices remaining relatively stable and unlikely to experience significant fluctuations.

Raw material price update

In Mandi, the cost of sponge iron (CDRI) dropped by INR 300/t to INR 30,900/t today, whereas pig iron (steel grade) prices in Ludhiana rose by INR 100/t to INR 39,300/t on a delivered-at-plant (DAP) basis.

Weekly price change

There was a notable decrease in prices across various segments: semis (ingot) prices witnessed a decline of INR 250/t, end cutting scrap prices experienced a dip of INR 200/t, and sponge iron (CDRI) prices fell by INR 300/t compared to the previous week.

Overview of other markets

Gujarat’s Alang market witnessed a decline of INR 100/t in ship-breaking melting scrap prices on 2 March, 2024, as assessed by BigMint. HMS (80:20) prices are now at INR 33,600/t ex-yard. Suppliers reduced their offers due to lower semi-finished steel prices and moderate interest in scrap caused by weak sentiments prevailing in the spot market.

In the western India-based Jalna steel market, prices for semi-finished, finished steel, and scrap remained stable, assessed at INR 42,500/t, INR 49,300/t, and INR 33,100/t, respectively. According to market sources, trade activities in finished steel were limited in today’s trading session. Although the market experienced good activity in the past couple of days, it once again witnessed limited demand in finished steel.

Imported scrap market weekly scenario

At the outset of the week, the imported scrap market in India experienced a slight improvement, with buyers displaying revived interest in procuring scraps from Non-European sources. However, this trend waned as the Turkish market began to decline. Given Turkiye’s prominent position as a scrap importer, other markets closely monitor its fluctuations. Furthermore, according to insights gathered by BigMint from industry insiders, downstream demand remains subdued, prompting steel mills to reduce production by 15-20% across various regions and they also withheld inventories until March. Consequently, buying interest remained limited.

On a weekly average basis, shredded scrap offers from Europe were evaluated at $415/t CFR, a decrease of $1/t compared to the preceding week’s $416/t.

Price highlights

End-cutting and billets spread: In Mandi, the end-cutting scrap and billets spread was at INR 5,000-5,500/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $377-$388/t, which equates to approximately INR 34,356/t (including freight), while local scrap-HMS (80:20) prices in Mumbai unchanged at INR 33,500/t d-o-d.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,250/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – info@steelmint.com.