- Sponge iron prices remain steady d-o-d in Mandi

- Semis, finished prices dip by INR 100-200/t d-o-d

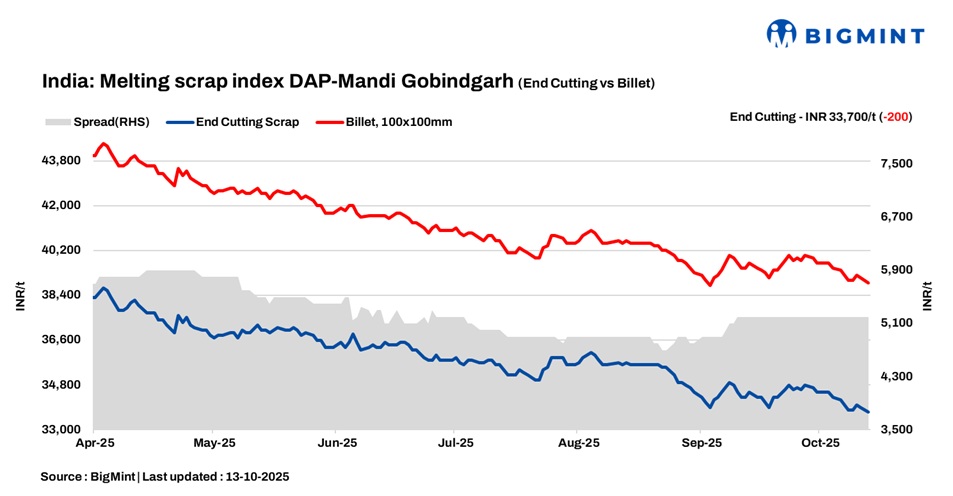

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 200/t d-o-d to INR 33,700/t DAP on 13 October 2025.

Steel prices in Mandi Gobindgarh opened the first day of Week 42 on a weak note, extending the recent downtrend, as trading activity remained subdued throughout both halves of the session. Persistent sales pressure in the finished steel segment, coupled with mounting inventories, has tightened liquidity across the market. With sentiment weighed down by prevailing uncertainties, buyers are adopting a wait-and-watch stance, anticipating further price corrections in the days ahead. The mood in Punjab’s steel hub remains cautious, with market participants watching for any triggers that could reverse the current bearish momentum.

Alternative raw materials

Sponge iron (CDRI) prices in Mandi Gobindgarh held steady d-o-d at INR 29,500/t today, showing no change from the previous session. In contrast, steel-grade pig iron values in Ludhiana softened slightly, by INR 50/t to INR 34,600 DAP. Trading activity remained minimal across alternative raw material segments, with no significant deals heard.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh declined by INR 200/t, closing at INR 38,900/t DAP. Other key production centres also witnessed price drops ranging within INR 200-600/t during today’s trading session. Notably, Muzaffarnagar and Ghaziabad experienced significant falls of INR 600/t.

Rebar (Fe500) prices in Mandi Gobindgarh declined by INR 100/t to INR 43,700/t ex-works, despite ongoing input cost pressures and inventory challenges. Similarly, HR strip (patra) prices eased by INR 300/t to INR 40,400/t ex-works in the Mandi market.

Overview of Jalna market

In the western India-based Jalna market, billet and HMS (80:20) prices declined by INR 100/t d-o-d to INR 37,200/t and INR 28,600/t, respectively, while rebar tags remained unchanged at INR 42,700/t. Market participants pointed to dull trading activity across steel products, with limited buying interest ahead of the Deepawali festival. Mills are operating with reduced production levels, which has helped balance moderate scrap inflows and limit inventory build-up, though no immediate recovery in market activity is expected.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $325-326/t, approximately INR 31,100/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 30,000/t DAP today. Indicative prices of shredded from Europe stood at $355-356/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply