- Sponge iron prices increase by INR 200/t

- Semis, finished steel prices rise INR 200-300/t

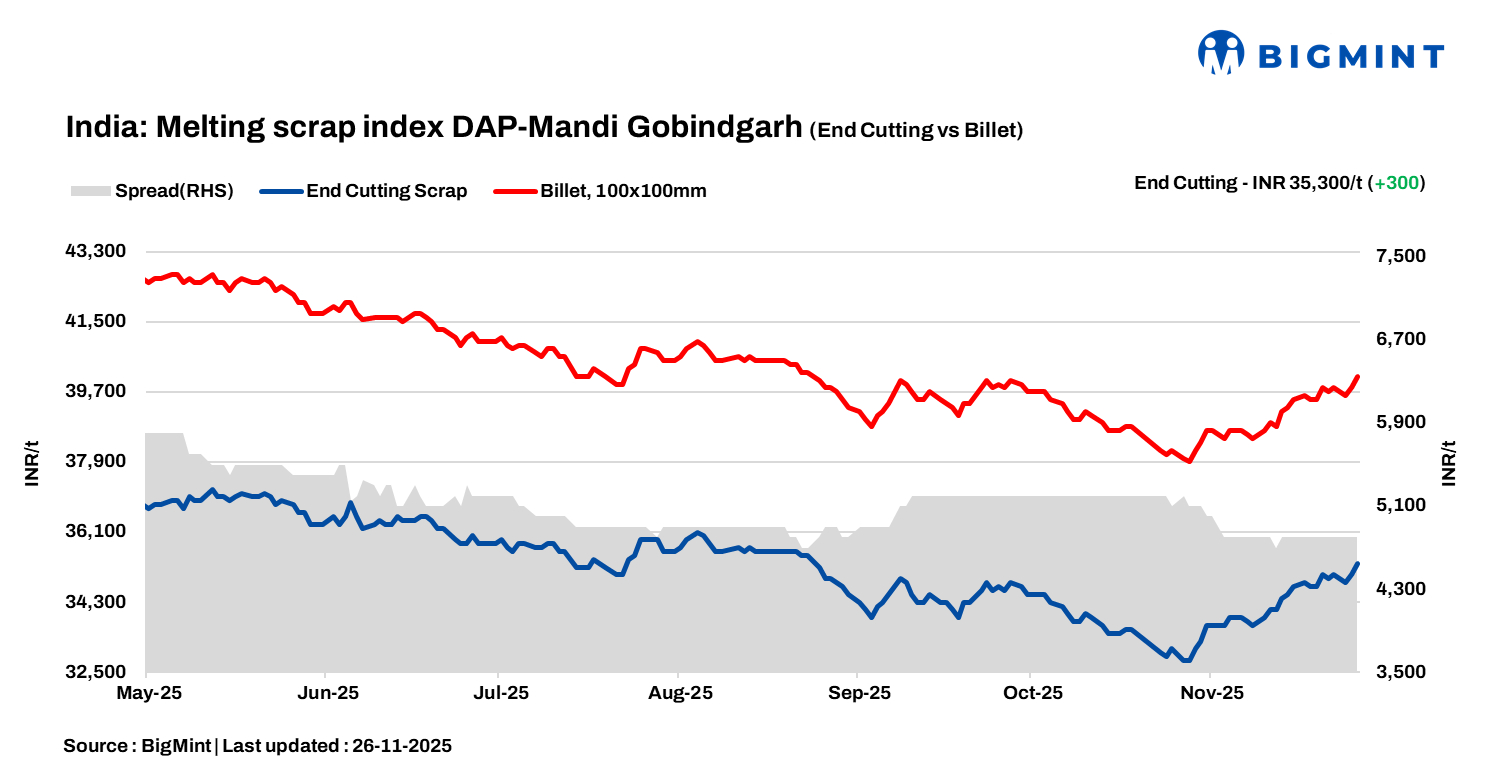

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, rose by INR 300/tonne (t) d-o-d to INR 35,300/t DAP on 26 Nov.

India’s key secondary steel hub, Mandi Gobindgarh, saw an uptick in steel demand on Wednesday, with prices rising by between INR 200-300/t across steel scrap, semi-finished and finished products. Mills reported better inquiry volumes in semi-finished steel by local re-rollers and nearby linked buyers, supporting the uptrend.

“Large units in Mandi are largely running at full capacity, while many medium-scale mills have shifted to reduced 12-hour shifts or cut production by up to 40-50% to manage weak conversion margins and higher costs. Operational sentiment remains cautious amid tight scrap availability, frequent GST checks, and continued pressure on sales realisations for small and medium units,”a mill owner told BigMint.

Raw material

Prices of sponge iron (CDRI) in Mandi Gobindgarh rose by INR 200/t d-o-d to INR 29,200/t DAP. On the other hand, steel grade pig iron prices in Ludhiana remained stable at INR 35,000/t DAP.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh surged by INR 300/t d-o-d to INR 40,100/t DAP. Ingot prices saw upticks ranging from INR 100 to INR 400/t during the day’s trading across major production hubs.

Rebar (Fe500) prices in Mandi rose by INR 200/t d-o-d to INR 44,500/t ex-works, while HR strip (patra) prices increased by INR 300/t to INR 41,100/t ex-works. Despite rising steelmaking costs and mounting credit liabilities weighing on mills, near-term sentiment remains positive, supported by steady to moderate demand from neighbouring states.

Overview of Eastern steel market

The Durgapur market in eastern India reported a notable improvement in prices, with billets gaining INR 450/t to reach INR 36,750/t and rebars moving up by INR 300/t to INR 39,100/t. HMS 80:20 scrap prices also firmed by INR 100/t to INR 30,600/t. Trading activity for finished steel has improved compared with the past few days, lending support to the ongoing price recovery. Market participants expect both prices and buying sentiment to strengthen further in December, as the market appears to have already bottomed out.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,600-4,900/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $318/t, approximately INR 30,573/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 29,800/t DAP. Indicative prices of shredded from Europe stood at $345/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,500/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply