- India’s demand weak amid price uncertainty

- Chinese coking coal, coke prices move higher

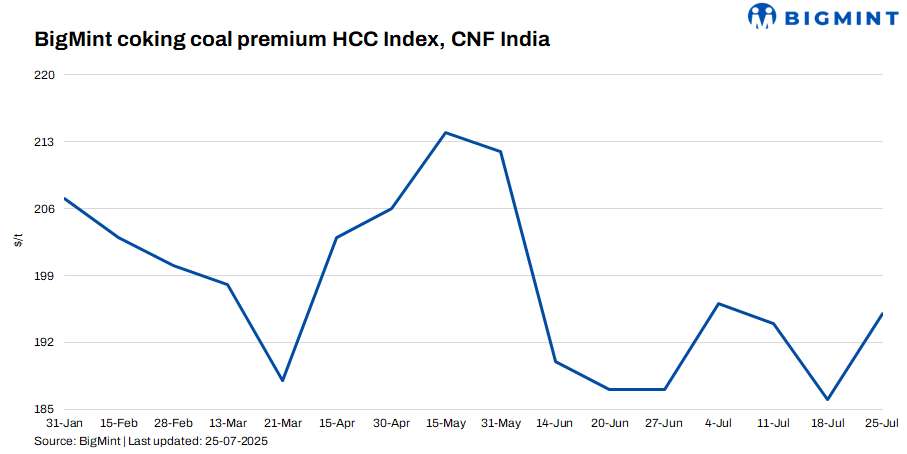

BigMint’s premium hard coking coal (PHCC) index was assessed at $195/tonne (t) CNF Paradip, India, on 25 July 2025, up by $9/t against the previous assessment on 18 July, amid positive global sentiment.

“A deal at similar levels was heard for Panamax cargo for August shipment. Market participants expect prices to further go up, as coking coal futures increased for September deliveries, but buyers are holding back. Supply is also tight, which may push buyers to lift bids,” observed a source.

Additionally, a western India-based mill booked 25,000 t of PHCC from Australia at around $195-200/t CFR India for August loading.

India’s demand for PHCC was weak due to uncertainty regarding price movements. However, Chinese buyers showed interest amid increasing domestic offers. Chinese met coke producers also initiated a third round of price hikes, though whether buyers will accept these values will become clearer from next week.

Rationale

- BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

- One deal was recorded during the publishing window. However, this category was not considered for index computation and given a weightage of 0%.

- Eight (8) firm offers, bids, and indicative prices were heard. Out of these, seven (7) were considered for price calculation and given 100% weightage.

- BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Indian met coke prices hold firm w-o-w: In eastern India, BF-grade (25-90 mm) met coke prices remained unchanged, with BigMint assessing rates at INR 29,000/tonne (t) ex-Jajpur. Similarly, the western region witnessed price stability, with Gandhidham recording ex-works prices of INR 29,100/t. The flat price trend is largely attributed to subdued trade volumes and an absence of major triggers in the domestic market.

2. Chinese coke producers implement 2nd round of price hikes: Chinese met coke producers implemented a second consecutive round of price hikes, which received acceptance from steel mills, indicating bullish sentiment. Additionally, imports from Mongolia and Russia gained momentum due to rising Chinese domestic prices and limited supply. Coke makers also proposed a third round of price hikes, though buyers’ acceptance of this revision is unclear.

3. Chinese coking coal futures surge on increased safety checks at Shanxi: China’s coking coal market displayed stronger surges on 23 July amid extended bullish sentiment. On Wednesday, the most-traded September contract for coking coal on the Dalian Commodity Exchange closed the daytime trading 11% higher at RMB 1,135.5/t, hitting the daily upper limit for a third straight session and touching the highest since late February.

Authorities in China’s coal heartland of Shanxi province in the country’s north have issued a stern warning to local officials in Changzhi, a key city for coking coal and anthracite production, amid a surge in mine accidents and growing concerns over lax enforcement of safety protocols.

Currently, sentiment in the global coking coal market is improving, as Chinese buyers have started showing interest following the hike in coal futures.

Leave a Reply