- PHCC index rises to $213/t amid fresh Australian cargo trades

- Met coke strength, mixed steel demand offer cautious support

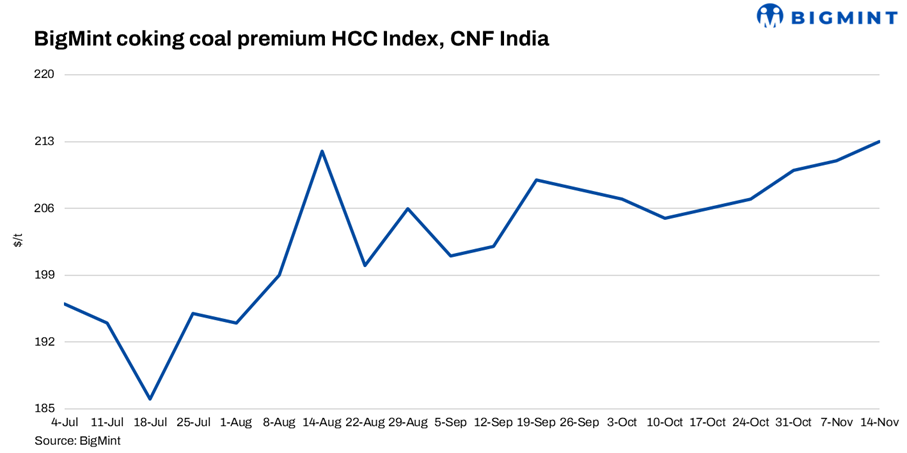

BigMint’s premium hard coking coal (PHCC) index was assessed at $213/tonne (t) CNF Paradip, India, on 14 November 2025, up by $2/t against the previous assessment on 7 November 2025.

In a recent deal, an eastern India-based steel mill booked 30,000 t of Australian PHCC cargo at 98.5% of the index.

Another western India-based mill had booked 30,000 t of Australian PHCC at 50% index and 50% fixed price basis.

Market sources cited that India’s coking coal market has remained range-bound, with price indications at around $213-215/t CFR. A participant from an Indian mill highlighted that the market seems to be witnessing a slow correction.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

Two deals were heard concluded. Hence, this category was considered for index computation and given a weightage of 50%.

Five (5) firm offers, bids, and indicative prices were heard. Out of these, three (3) were considered for price calculation and given 50% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia — normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Met coke prices rise further in eastern India, supported by robust fundamentals: The Indian metallurgical coke (met coke) market displayed mixed movements during the week ending 13 November 2025. Prices in eastern India gained marginally amid robust demand, while those in the western region held steady amid limited spot activity and balanced demand.

In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 31,500/t ex-Jajpur, marking a rise of INR 500/t w-o-w. Meanwhile, western India’s ex-works Gandhidham prices remained unchanged at INR 30,000/t. Foundry-grade met coke in Rajkot rose slightly by INR 200/t to INR 35,700/t, supported by steady consumption and firmer cost push.

2. Chinese coke prices strengthen on tight supply: China’s met coke plants completed the third round of price hikes in early November amid strong feed coal costs and tight supply. Profit margins remained thin but stable, while coke inventories at steel mills stayed low, lifting restocking activity.

3. India’s BF-rebar trade prices drop amid slow demand: India’s trade-level blast furnace (BF) rebar prices dropped w-o-w, owing to slow demand across major markets. Some primary mills either offered price support or reduced list prices amid weak market sentiments. Trade-level BF rebar prices dropped by INR 500/tonne (t) ($6/t) w-o-w to INR 47,300/t ($533/t) exy-Mumbai, as per BigMint’s benchmark assessment on 14 November 2025. Prices are exclusive of GST at 18%.

4. Indian HRC prices remain range-bound: Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends w-o-w. Some markets saw a downtrend, while in others, prices remained firm. HRC prices hovered between INR 46,500-48,300/t ($525-546/t) across regions, while cold-rolled coil (CRC) tags ranged between INR 52,000-56,500/t ($588-538/t).

Leave a Reply