- Aus-India vessel freight rates inch down w-o-w

- Indian steel prices drop on rising inventories

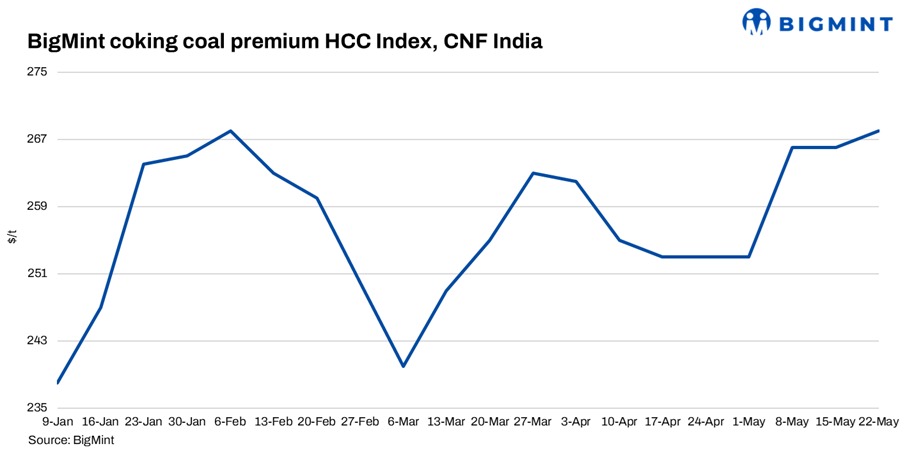

BigMint’s premium hard coking coal (PHCC) index was assessed at $268/tonne (t) CNF Paradip, India, on 22 May 2026, inching up by $2 w-o-w in recent deal.

Market chatter suggested a 30,000t trade for Australian PHCC at around $269/t CFR India by an eastern India based mill; however, the deal could not be independently confirmed at the time of reporting. Meanwhile, premium hard coking coal indices were heard around $241/t FOB for premium low-volatility (PLV) material.

BigMint has consolidated its PHCC CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia — normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors influencing prices

Australia-India vessel freights inch down: Dry bulk coal freights to India remained mixed in the week ended 22 May, with Pacific Panamax routes under pressure from weak enquiry and rising tonnage, while South Africa and Indonesia-linked routes stayed comparatively supported. In the Pacific, Panamax sentiment softened as limited Australia-India cargo enquiry and a growing list of open vessels weighed on freight ideas. Softer freight derivatives and easing bunker prices further pressured market confidence, with charterers bidding below previous fixture levels.

Indian BF rebar prices decline by INR 700/t w-o-w on weak demand and cautious market sentiment:

Trade-level BF rebar prices (distributor-to-dealer) edged down by INR 700/t ($7/t) w-o-w to INR 56,800/t ($592/t) exy-Mumbai, according to BigMints assessment on 22 May 2026. Buying activity remained moderate across key regions, while demand in south Indian markets continued to stay relatively weak, as per sources. Distributors maintained comfortable inventory levels, leading to need-based procurement amid limited construction activity. Overall market sentiment remained cautious-to-weak during the week.

Indian met coke market holds firm – In the eastern region, BF-grade coke prices increased marginally by INR 300/t to INR 36,700/t ex-Jajpur, reflecting improved buying interest and higher logistics costs. Meanwhile, prices in western India remained stable at INR 33,500/t ex-Gandhidham, indicating sufficient material availability and steady trade flow. Foundry-grade (+90 mm) coke prices also remained unchanged at INR 36,400/t ex-Rajkot, suggesting stable demand conditions from the casting and foundry segment. Additionally, India’s Ministry of Steel has urged the Ministry of Finance to reconsider and withdraw the anti-dumping duty (ADD) imposed on imported metallurgical coke (met coke), citing concerns over limited domestic availability and rising input costs for steelmakers, according to an office memorandum dated 18 May 2026.

Outlook

Coking coal prices are less likely to see an uptrend next week amid signals of steel prices weakening and not much of weather related disruptions from exporting countries.

Leave a Reply