- Prices may have reached bottom, some believe

- Project prices climb up as bookings improve

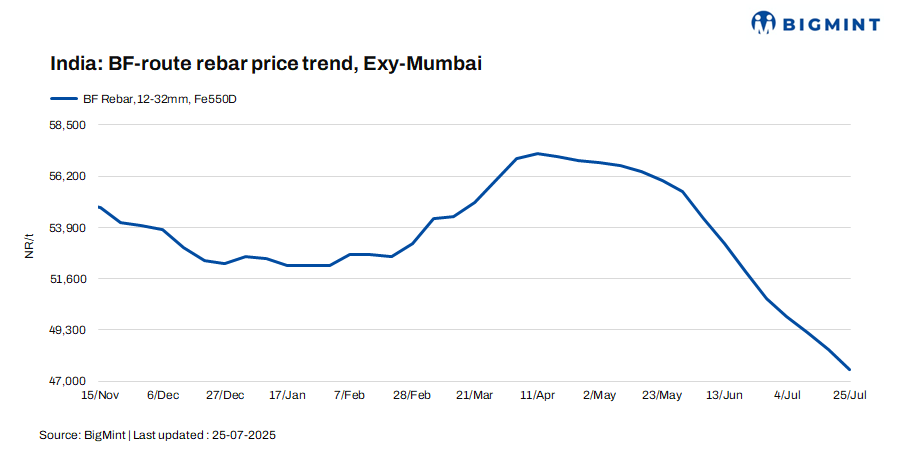

Trade-level blast furnace (BF) rebar prices declined w-o-w due to subdued demand across key Indian markets. Weak market sentiment, cautious buying, and monsoon-related disruptions kept buyers on the sidelines. While most market participants remained uncertain about a near-term price recovery, some believe prices may have reached a bottom, suggesting limited downside from current levels.

Some major private steel producers were heard to have increased list prices of rebars by up to INR 1,500/tonne (t) ($17/t) this week, with rates ranging between INR 48,000-48,500/t ($555-560/t) on landed basis. However, the impact of this hike is yet to reflect in the trade market and may become evident in the coming days.

Trade-level BF rebar prices declined by INR 900/t ($10/t) w-o-w to INR 47,500/t ($549/t) exy-Mumbai, as per BigMint’s assessment on 25 July 2025. Prices are exclusive of GST at 18%.

In the projects segment, rebar prices increased w-o-w to INR 46,500-47,500/t ($537-549/t) FOR Mumbai, supported by improved bookings. Approximately 10,000 t were booked, driven by demand from government projects.

Rebar inventories with primary mills rose to around 500,000-550,000 tonnes amid sluggish sales during the month, as per market sources.

Leading private steel mill has mainteanace shutdown plan at one of its plant starting first week of August 2025, sources informed BigMint.

Update on projects

- L&T Energy GreenTech will establish India’s largest green hydrogen plant at IOCL’s Panipat refinery, supplying 10,000 t annually using alkaline electrolysers, marking a major step in clean energy transition.

- NCC Limited has received an INR 2,269 crore order from the Mumbai Metropolitan Region Development Authority (MMRDA) for Mumbai Metro Line 6 (Swami Samarth Nagar to Vikhroli). The contract includes design, supply, installation, and commissioning of rolling stock, signalling, telecom systems, and platform screen doors.

- Rail Vikas Nigam Limited (RVNL) has received a letter of acceptance from South Central Railway for upgrading the overhead equipment (OHE) from 1x25kV to 2x25kV across 195.5 route kilometres (RKM) in Andhra Pradesh.

- GR Infraprojects’ subsidiary has received the appointed date from the National Highways Authority of India (NHAI) for a 33.5 km, INR 1,248 crore, 6-lane greenfield highway project under Bharatmala Pariyojana in Bihar, effective from 1 July 2025.

- Kalpataru Projects International Ltd. (KPIL) has bagged new orders worth INR 2,293 crore across the buildings and factories and overseas power transmission sectors, strengthening its FY’26 order book and future growth visibility.

- RITES has received a revised project order from IIM Raipur, increasing the estimated cost from INR 148.25 crore to INR 220.65 crore. The engineering, procurement, and construction (EPC) contract covers academic and hostel blocks, a dining hall, and an auditorium, to be completed in 23 months.

- L&T’s Buildings and Factories unit secured large orders in Amaravati, Mumbai, and Muscat. Projects include high-rise secretariat and residential towers, and premium office spaces, covering civil works, finishes, MEP, landscaping, and integrated amenities.

- GR Infraprojects Limited emerged as the L1 bidder for an INR 290.23 crore EPC contract to construct the 26.67 km Giridih Bypass (towards Tundi) in Jharkhand, with a 24-month completion timeline.

Factors behind market dynamics

1. IF rebar prices rise amid improved trade activities: Induction furnace (IF) rebar trade prices rose w-o-w, supported by improved trade activity across key Indian markets. The uptick in finished steel prices was supported by a rise in tags of semi-finished steel products such as billets and sponge iron, especially in central India (Raipur and Raigarh).

While buyer response to new offers remained cautious, deals were concluded at previous prices. Additionally, inventory levels remained elevated at 12-15 days.

IF rebar prices rose by INR 400/t ($5/t) w-o-w to INR 43,700/t ($505/t) exw-Mumbai as on 25 July.

The price gap between BF and IF rebars narrowed to INR 3,500-4,000/t ($40-46/t) in Mumbai, driven by a rise in IF rebar prices and a simultaneous decline in BF rebar prices. IF rebars continue to dominate the Indian market with a 65-70% share.

2. Raw material prices show mixed trend w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index rose by INR 200/t ($2/t) w-o-w to INR 5,200/t ($60/t) ex-mines on 19 July 2025. Iron ore tags in Odisha witnessed an uptrend this week, driven by a rise in base prices set by Odisha Mining Corporation (OMC) and limited availability of material in the open market amid the monsoon. Market participants said that several merchant miners were refraining from accepting bulk orders, further tightening supply.

Australian premium hard coking coal (PHCC) prices dipped by $4/t w-o-w to $190/t CNF Paradip.

Outlook

Market participants expect BF trade prices to rebound in the coming days, as an improvement was observed in the IF rebar segment this week.

Leave a Reply