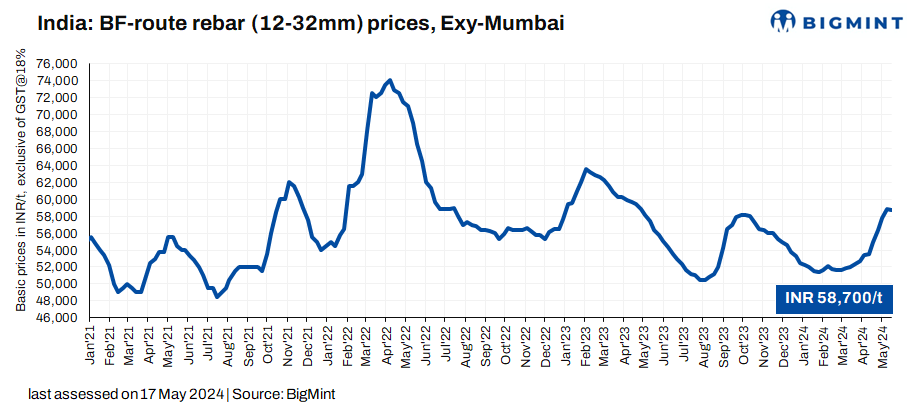

Trade-level blast furnace (BF) rebar prices are hovering at nearly 1-year high levels now as similar price levels were last seen in end-April 2023, as per BigMint data. On weekly basis, prices have showed mixed trends across markets amid slow buying activities, shortages of sizes in the trade channel. Prices have increased consistently over the last few weeks amid interim price hikes by tier-1 mills due to lesser supplies in April-May.

Current rebar prices (12-32mm, Fe500D) in the trade segment have dipped marginally w-o-w by INR 100/t ($1/t) to INR 58,700/t ($704/t) exy-Mumbai. Prices are exclusive of GST at 18%.

In the projects segment, prices are hovering around INR 57,500-58,000/t ($690-696/t) landed Mumbai basis.

Factors driving market dynamics:

1. Limited availability and shortage: Some leading tier-1 mills have undergone maintenance shutdowns during the April-May period, which led to shortage of materials in the trade channel. Additionally, a PSU steel major has been under shutdown due to non-availability of coking coal. Consequently, market participants have been quoting higher prices due to unavailability of various material sizes. Meanwhile, demand from end-users has remained weak amid price volatility and market uncertainty.

2. IF rebar prices drop w-o-w: Induction Furnace (IF) route rebar trade prices dropped w-o-w by INR 100/t ($1/t) to average of INR 53,200/t ($638/t) exw-Mumbai. Manufacturers offered internal trade discounts amid slow buying activities in the market. Buyers have booked good volumes over last few days and procured cautiously this week amid uncertainty due to volatility in prices.

Inventory days are around 8-10 days now against 6-8 days in the previous month. Prices of raw material like billets, sponge iron were volatile during the period. IF-rebar trade prices now stand at INR 53,300/t ($639/t) exw-Mumbai as per BigMint’s assessment on 17 May. It must be noted that the IF-based mills have a 65-70% share in the rebar market.

The gap between BF-IF rebars widened to around INR 5,500-6,000/t ($67-72/t) in May as compared with INR 4,000-4,500/t ($48-54/t) in last month. The gap between the two widened amid interim price hikes by primary mills during April-May period.

3.Infrastructure, construction demand: India’s national highway construction for the April 2024 was recorded at 483 kms against 523 kms in the corresponding period last year (CPLY).

Despite of the slowdown in project awards in H2CY23, the Ministry of Road Transport and Highways (MoRTH) has continued to front-load capital expenditure, spending over INR 54,500 crores on new highways in April 2024. The ministry has already met nearly 20% of its annual capex target with 11 months remaining, as per the report from the Union Cabinet.

Outlook

Supply issues are likely to ease in coming days as market participants expect that PSU mill will resume production from next week and other private steel mills will also restore normal operations next month. Consequently, prices might cool down with easing supply issues.