- Bauxite imports from Guinea plunge 45% y-o-y, pulling down total

- Bauxite output dips 2% on lower volumes from Odisha, Jharkhand

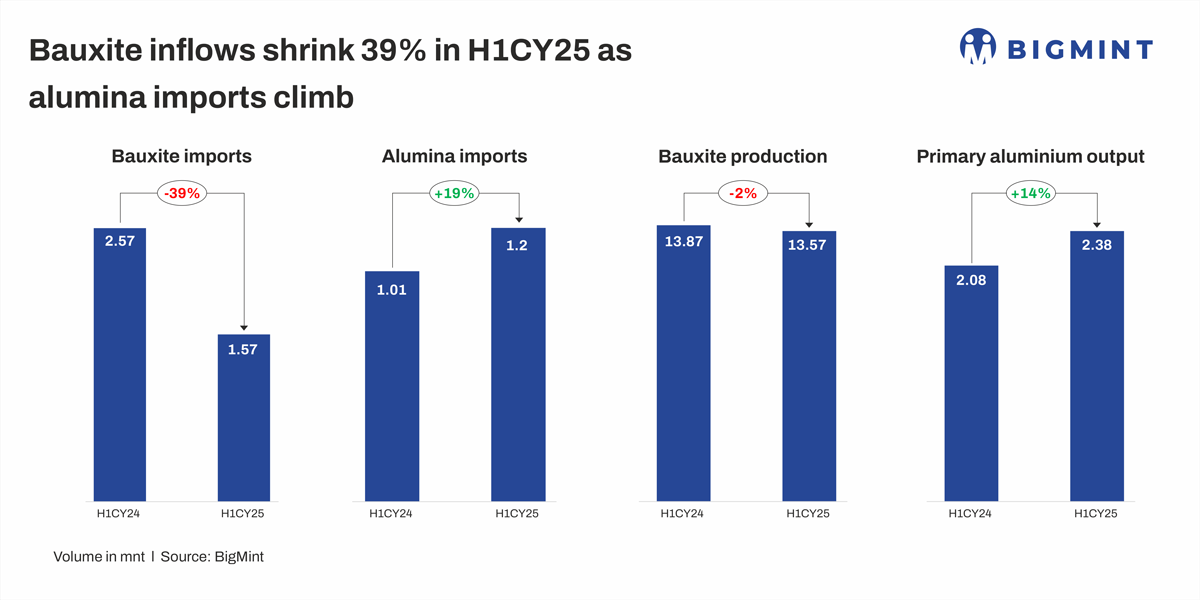

India’s bauxite imports fell sharply by 39% y-o-y in the first half of calendar year 2025 (H1CY’25) to 1.57 million tonnes (mnt) from 2.57 mnt in H1CY’24. What makes this fall even more notable is that it occurred amid a 2% dip in domestic production, which stood at 13.57 mnt versus 13.87 mnt a year earlier.

In contrast to bauxite, alumina imports rose 19% y-o-y to 1.20 mnt in H1CY’25. This uptick indicates a shift towards importing value-added material, likely to bridge quality gaps or compensate for raw bauxite shortages, particularly among producers without captive refining capabilities.

Despite India’s abundant bauxite reserves, imports of aluminium raw materials have continued to rise even as domestic production remains steady, largely due to structural and regulatory challenges. Delays in mine auctions, such as the stalled Karlapat block in 2021, and disruptions such as the abrupt halt of Vedanta’s public hearing on the Sijimali project, highlight the persistent hurdles facing mine development.

Meanwhile, the country’s rapidly growing aluminium industry requires a steady and scalable supply of raw material. Until domestic bottlenecks in mining are resolved, imports will remain an essential part of India’s bauxite supply chain.

Bauxite production weak across states, Gujarat remains stable

Regional bauxite production volumes highlight a largely negative picture. Odisha, the country’s leading bauxite-producing state, recorded a 14% drop, while Jharkhand saw the sharpest fall of 16%. Madhya Pradesh registered an 11% decline, followed by Chhattisgarh at 8% and Maharashtra at 2%. In contrast, Gujarat remained resilient, with output holding steady.

Country-wise bauxite, alumina imports

India’s bauxite and alumina imports saw a sharp 28% decline y-o-y in H1CY’25, to 2.76 mnt from 3.58 mnt in the same period last year. The significant drop was primarily driven by a 45% slump in imports from Guinea, the largest supplier of bauxite, whose volumes fell to 1.38 mnt from 2.5 mnt in H1CY’24.

Despite stricter mining regulations under Guinea’s military-led government, bauxite demand continued to rise. Companies such as SBG, GAC, and KIMBO reported zero exports, while Kambia Bauxite Mining remained inactive. Major Chinese players maintained stable shipments, but smaller operators faced challenges. Port diversification, with nine active facilities, supported export growth. The government’s push for local refining over raw exports led to disputes, with some firms losing licenses for not meeting refinery construction deadlines.

Additionally, shipments from Indonesia also saw a 17% decline, to 0.53 mnt from 0.64 mnt.

In contrast, China increased its alumina exports to India, by 44% to 0.13 mnt from 0.09 mnt in H1CY’24. This growth was supported by strong domestic alumina production in China.

The decline in India’s bauxite imports was largely attributed to reduced availability from Guinea, coupled with stronger demand from China, which led to cargo diversions. Additionally, imports from Indonesia and Vietnam also eased, reflecting softer global trade flows and ongoing logistical challenges.

Despite the fall in imports, India’s domestic production of bauxite remained relatively steady.

India defies raw material supply challenges, primary aluminium output rises

Despite raw material volatility, India’s primary aluminium production remained resilient. Output in H1CY’25 rose notably by 14% y-o-y to 2.38 mnt.

Vedanta led growth, with a 20% increase to 1.07 mnt, while Balco and Nalco both registered 13% gains, producing 0.34 mnt and 0.27 mnt, respectively. Hindalco also grew modestly by 5% to 0.69 mnt.

Outlook

Looking ahead, India’s bauxite imports in H2CY’25 are likely to remain subdued, with steady alumina imports and consistent domestic bauxite production. Despite a dip in domestic bauxite output in H1, annual production is expected to remain stable compared to the previous year. This stability is supported by a growth trend in domestic bauxite production, which has seen a CAGR of 2.58% from 2020 to 2024.

Leave a Reply