- Two and three-wheeler sales see sharp surge

- West Asia tensions disrupt auto exports

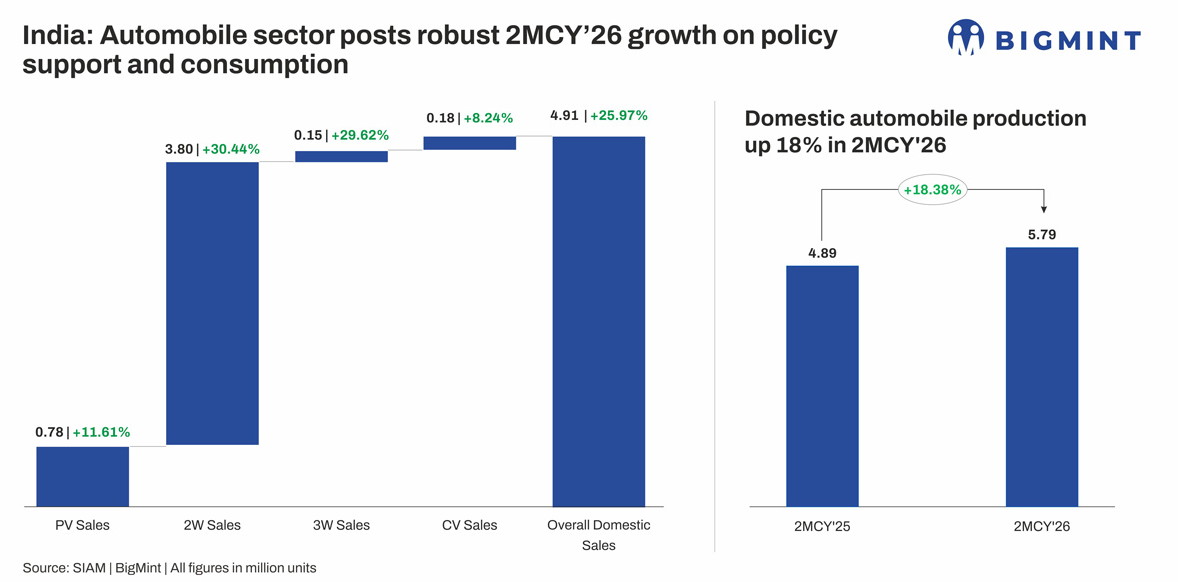

India’s automobile sector recorded robust year-on-year growth in 2MCY’26, as per SIAM OEM data, driven by strong performance across segments. Passenger vehicle sales rose 11.61% to 867,321 units from 777,075 units, while two-wheelers and three-wheelers surged 30.44% to 3,797,009 units from 2,910,823 units and 29.62% to 150,298 units from 115,955 units, respectively. Commercial vehicle sales also grew 8.24% to 184,000 units from 170,000 units.

Overall domestic sales increased 25.97% to 4,906,705 units from 3,895,200 units, while total production rose 18.38% y-o-y to 5,792,006 units from 4,892,901 units, reflecting healthy demand and sustained manufacturing momentum.

However, on a m-o-m basis, the market showed moderation. Domestic sales declined 3.49% to 2,409,738 units in February 2026 from 2,496,967 units in January, while production fell 2.14% to 2,864,612 units from 2,927,394 units, indicating a sequential slowdown after strong earlier growth.

Retail sales surge over 18% m-o-m in 2MCY’26

Meanwhile, FADA’s retail data for 2MCY’26 reflected strong year-on-year growth across all vehicle segments. Passenger vehicle sales increased 18.06% to 908,243 units from 769,318 units in 2MCY’25. Two-wheeler sales rose 23.42% to 3,553,375 units from 2,879,142 units, while three-wheeler sales grew 21.40% to 244,264 units from 201,214 units.

Commercial vehicle (CV) sales advanced 18.09% to 215,140 units from 182,188 units, and tractor sales recorded a sharp rise of 28.45% to 204,177 units from 158,955 units.

Overall retail sales increased 22.63% y-o-y to 5,056,463 units from 4,123,209 units, indicating healthy demand traction across segments. On a m-o-m basis, however, total retail sales declined by 9.46%, reflecting a sequential slowdown after strong earlier momentum.

Vehicle retail sales hit record Feb sale

India’s automobile sector is witnessing strong growth momentum, supported by robust domestic demand and improved affordability following GST changes. Retail vehicle sales surged 25.6% y-o-y in February 2026 to a record 24.09 lakh units, with growth seen across all major segments including two-wheelers, passenger vehicles, commercial vehicles and tractors.

“Feb’26 has turned out to be a landmark month for the Indian auto retail sector, further strengthening the positive momentum seen after the GST 2.0 announcement,” FADA President C S Vigneshwar said. He added that “the growth was broad-based across almost all segments,” highlighting strong underlying demand in the market.

The growth was largely driven by stronger rural demand, supported by improved agricultural incomes, along with healthy economic activity and better financing availability. Demand remained robust across both personal mobility and commercial segments, aided by festive and marriage season demand, new product launches, and continued preference for SUVs and utility vehicles.

“The sharper rural growth is particularly encouraging as it is supporting the sale of small cars, even as SUVs and utility vehicles continue to drive overall volumes,” Vigneshwar noted. At the same time, improved supply discipline and better alignment between wholesale and retail sales have helped stabilize inventory levels across dealerships.

Despite the strong demand environment, the sector continues to face some supply-side pressures, including logistics constraints and rising freight costs, which have impacted vehicle availability in certain regions. However, with healthy order books and sustained consumer interest, the market is expected to maintain steady growth momentum going forward, gradually transitioning towards a more stable phase.

Amid escalating tensions in West Asia, around 2,000 Hyundai cars exported from India to Gulf countries may be rerouted back to Chennai due to disruptions in key shipping routes such as the Strait of Hormuz and the Red Sea. Vessel movements from Tamil Nadu ports have slowed significantly, with nearly 4,000 containers already diverted. Exporters are facing delays and potential losses as cargo, including textiles and automobiles, remains stranded due to ongoing logistical uncertainties.

Impact on aluminium ADC12 alloy

Firm conditions in the automobile sector continue to lend support to India’s aluminium ADC12 alloy market, given its extensive application in automotive die-casting components. Sustained production across passenger vehicles, two-wheelers and commercial vehicles has underpinned steady demand for lightweight aluminium alloys, even as market participants navigate evolving pricing dynamics and raw material constraints.

ADC12 offer levels have increased sharply across regions, with southern markets quoting around INR 285,000-290,000/t and some suppliers offering up to INR 300,000/t, while Pune remains largely aligned with these levels. In contrast, Delhi offers for 30-day payment terms are slightly lower at INR 280,000-285,000/t. However, OEMs have shown resistance at these elevated prices, leading to significant bid-offer gaps, with buyers bidding in the range of INR 270,000-280,000/t and some targeting even lower levels of INR 265,000-270,000/t.

Outlook

India’s automobile sector is expected to maintain a steady growth trajectory, supported by resilient domestic demand, strong rural recovery, and continued preference for SUVs and personal mobility. While near-term growth may moderate due to supply-side challenges such as logistics constraints and elevated costs, healthy order books and improved affordability are likely to sustain momentum. Consequently, demand for aluminium ADC12 alloy is expected to remain firm, although price volatility and bid-offer gaps may persist in the short term.

Leave a Reply