- India output revised lower on yield losses despite steady acreage

- Argentina’s sharp area cut reduces South American export availability

The USDA World Agricultural Production (WAP) January 2026 report points to a slightly tighter global cotton supply scenario for 2025/26, led by downward revisions in India and Argentina, two key foreign producers. Global cotton production is now estimated at 119.4 million 480-lb bales, marginally lower than last month and slightly below earlier expectations, even as some producing countries show stability.

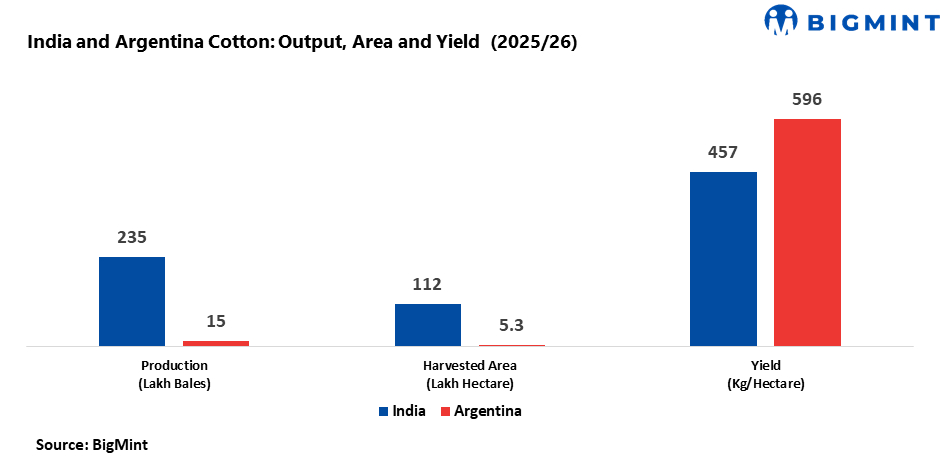

What happened is that India’s cotton production has been revised down m-o-m to 23.5 million bales, from around 24.0 million bales earlier. The revision is driven entirely by yield, which is now estimated at 457 kg per hectare, down 2% m-o-m, while harvested area remains unchanged at 11.2 million hectares.

Weather woes

Despite this cut, India’s output is still 1% higher y-o-y, but remains 7% below the five-year average, highlighting persistent structural yield challenges. According to the report, uneven monsoon distribution and excessive rainfall during August-September caused flower and boll shedding in key producing states such as Maharashtra, Gujarat, and Telangana, sharply reducing yield potential. These states together account for a large share of India’s total production, amplifying the impact of yield losses.

Acerage shift

In Argentina, the adjustment is more severe on the acreage side. Cotton harvested area for MY 2025/26 is now forecast at 530,000 hectares, down 15% from last month and last year, as farmers in northern provinces shifted land toward sunflowerseed. As a result, Argentine cotton production is estimated at 1.5 million bales, down 16% m-o-m, though still marginally higher y-o-y due to improved yields of 596 kg per hectare, up 19% y-o-y. Planting was around 80% complete by end-December, and while early crop conditions are reported as generally good, the reduced area significantly limits Argentina’s exportable surplus for the season.

At the global level, total foreign cotton production for MY 2025/26 is estimated at around 105.5 million bales, slightly lower than last month, while world output is broadly flat compared with last year. This indicates that supply growth outside the US is losing momentum. Importantly, the WAP data shows no major offsetting increases from other origins large enough to neutralise the combined decline from India and Argentina. As a result, global availability remains adequate on paper but less comfortable than earlier projections, particularly for consistent, export-grade cotton.

Why this happened is mainly due to weather disruptions in India and crop economics in Argentina. In India, excess moisture after a strong early monsoon reduced yield efficiency, despite stable acreage. In Argentina, relative profitability favoured sunflowerseed over cotton, leading to a structural acreage shift rather than a temporary adjustment. These factors together have constrained foreign supply growth at a time when global demand has not collapsed but remains cautious.

What may happen next is a more supported global cotton balance in the second half of MY 2025/26. For ginners, lower output in India could tighten quality cotton availability as arrivals progress. For spinning millers, near-term supply may remain sufficient, but origin-specific tightness could emerge later in the season. For brokers, the focus will remain on India’s arrival pace, quality spreads, and Argentina’s January-February weather during boll formation, as these will determine whether global cotton prices remain range-bound or move higher if demand shows even a modest recovery.

Leave a Reply