- Steel majors pay 100%+ premiums to secure iron ore supply

- High premiums provide cost stability, strategic advantage

There is an explanation for high premiums being paid in India’s mineral auctions. They are not reckless bids – they are a logical and calculated hedge. India’s steel majors are paying over 100% premiums for merchant iron-ore mines because, once security of supply, grade certainty and logistics savings are factored in, the math turns in their favour and shields them from volatile markets and costly imports.

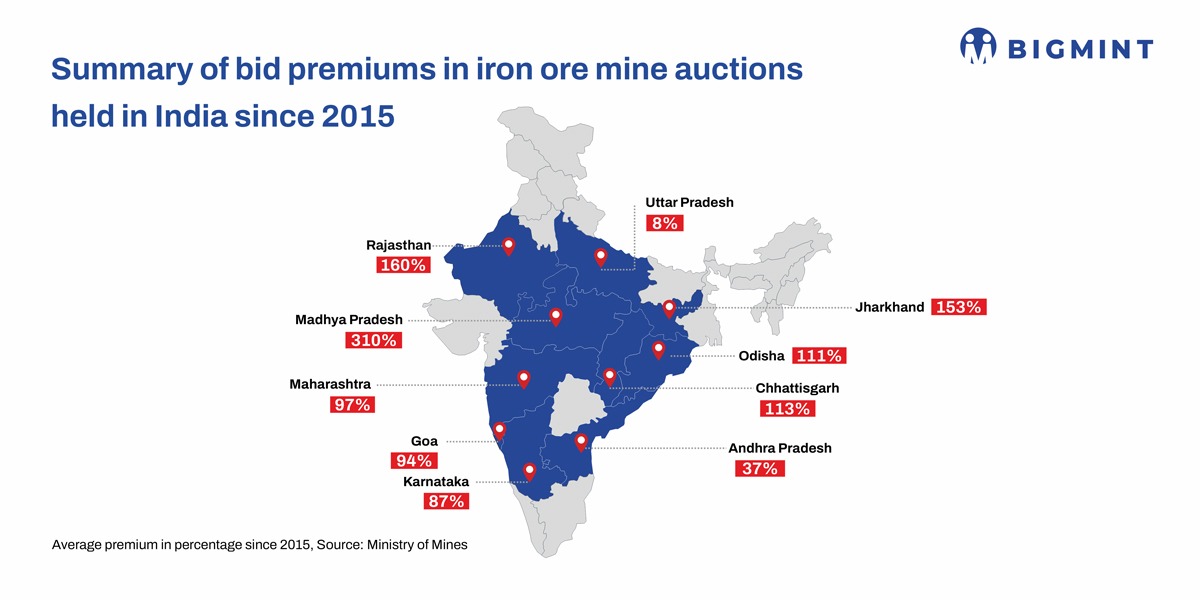

According to data published by the Ministry of Mines, ~130 iron ore (including combined iron ore, manganese and dolomite deposits) blocks have been auctioned since 2015 across different states mainly Odisha, Karnataka and Chhattisgarh (3 states producing ~87% of India’s iron ore). The weighted average premiums across states often exceed 100%, but production from these mines has remained strong and supply to the system continues to grow, especially from the Odisha blocks and expired/category C blocks in Karnataka despite of high auction premiums.

Players who drive premiums

Captive players with end-use plants have dominated the process, winning about 80 of the 130 blocks and controlling more than ~60% of Odisha, which produces 55% of India’s iron ore.

Economics behind 100 % premium

Taking a typical Odisha iron ore mine at a 100 % premium shows that the economics is still favourable for integrated steel producers. At an IBM reference price for Fe 60-62%, the premium itself works out to roughly INR 4,500/t. Adding mining costs of about INR 400/t and statutory levies such as royalty, DMF and NMET of around INR 750/t, plus logistics costs of approximately INR 500/t for a nearby captive plant, the total landed cost of iron ore comes to about INR 6,000-6,200/t if compared grade to grade on similar slab.

When compared with alternative sources, this cost remains competitive. Domestic non-captive sources deliver landed costs ranging between INR 5,200/t and INR 6,000/t but with far greater variability in price and supply and grade slippages as well. Imported ore, even at a benchmark of global Index CFR China $100/t, lands in India at roughly INR 10,000/t. This demonstrates that even at a 100% auction premium, captive mines provide cost stability and a clear advantage over imports while being broadly at par with or cheaper than domestic alternatives with owning the mine having separate advantages.

Strategic advantages beyond cost

Owning an auctioned iron ore mine at even 120-125% premiums offers benefits that go far beyond the headline cost for following reasons:

- Security of supply: A single, long-term source of ore with predictable grade and quantity gives steel plants the confidence to plan capacity and investment.

- Insulation from market volatility: Freedom from the uncertainty of spot auctions and juggling multiple short-term suppliers.

- Compliance and coordination savings: One captive source means one set of approvals and documentation instead of navigating numerous contracts.

- Logistics efficiency: Most large steelmakers are building or expanding high-capacity slurry pipelines — increasing from about 36 mnt per annum today to nearly 200 mnt over the next two to three years — which can lower transport costs by roughly INR 800-1,000/t (assuming alternate cost in same range) while avoiding road congestion, weather-related disruptions and law-and-order risks.

Taken together, these factors make even high-premium blocks economically viable and strategically sound for integrated steel producers.

The Evidence: Serious Bidders Keep Coming

Despite the perception that auction premiums of 100% are prohibitively high, India’s leading steel producers have continued to bid aggressively – even since 2015 auctions. In Odisha, blocks have been secured at premiums around 110%; in Chhattisgarh, at around 115%; and in Karnataka, at more than 90%. These are not speculative or opportunistic plays but deliberate, strategic acquisitions by integrated steelmakers seeking to lock in long-term, high-quality iron ore supply to support their existing plants and ambitious capacity expansion plans.

The sustained willingness of these companies to pay such premiums underscores their assessment that, when total landed costs and security of supply are considered, these blocks remain economically attractive and central to their competitive positioning.

Takeaway

High auction premiums are not automatically a burden. When total landed cost, security of supply, grade certainty and logistics savings are considered, 100%-plus premiums can be economically rational — and far preferable to relying on volatile spot markets or costly imports. This is why India’s major steel producers, with long-term growth plans, continue to invest heavily in auctioned iron-ore blocks. Given the sector’s expansion trajectory, high premiums are likely to remain a feature of the market – and are already being absorbed into the steel industry’s operating model.

High premiums quoted by captive players during auction rounds had an adverse impact on smaller industry participants, particularly those engaged in merchant and commercial mining, rendering their operations financially unviable. However, over the past couple of years, there has been a gradual shift in this trend, with the entry of a few new players bringing a more competitive edge to the sector.

Leave a Reply