- Coal production declines by 2% y-o-y in Apr-Oct’25

- Peak power demand remains below govt projections

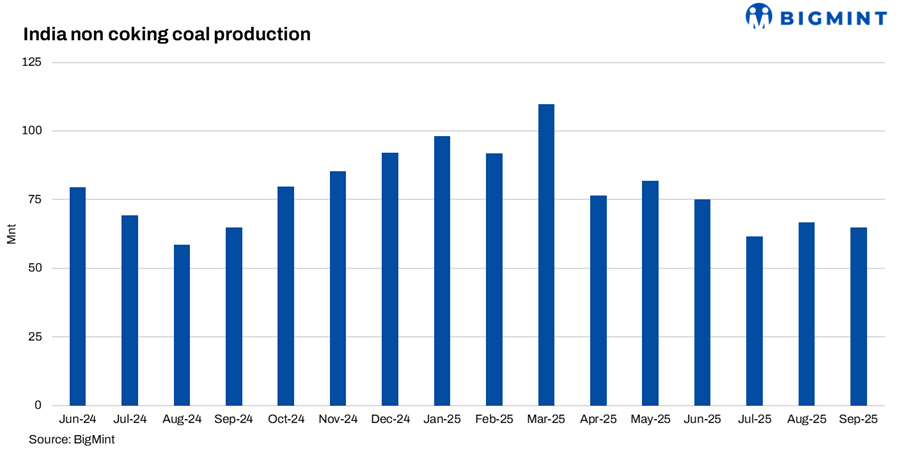

India’s non-coking coal sector continues to struggle with a supply overhang, leading to weak pricing and sluggish production momentum. While global seaborne thermal coal markets have experienced a significant bull run, domestic indicators point towards a pronounced slowdown.

Highlights

- India’s coal production in October 2025 registered 77.43 million tonnes (mnt), an 8.5% y-o-y decline, and cumulative production for the fiscal year (April-October 2025) remains 2.04% behind last year’s pace.

- This production curb appears to be a strategic response to weaker-than-expected demand rather than an operational failure. Peak power demand has plateaued in the 240-245 GW range, substantially below the government’s projection of 277 GW. Consequently, total power output fell by 11% y-o-y in October, with coal-fired generation down 14% y-o-y.

- The most telling metric is the inventory build-up. Coal stockpiles at power plants surged to 52.05 mnt as of mid-November 2025, representing approximately 17 days of cover. This is a significant 42% increase from the 36.64 mnt held at the same time last year. Simultaneously, non-coking coal stocks at major Indian ports have risen 8% y-o-y to 12.84 mnt.

Takeaway

This combination of reduced production, high inventories, and falling consumption suggests that the post-monsoon demand recovery has been tepid. The data indicates that industrial power burn remains sluggish, and the market is currently working through a substantial overhang of supply.

Leave a Reply