- MCX gains support Indian aluminium price sentiment

- Elevated energy costs pressure European aluminium producers

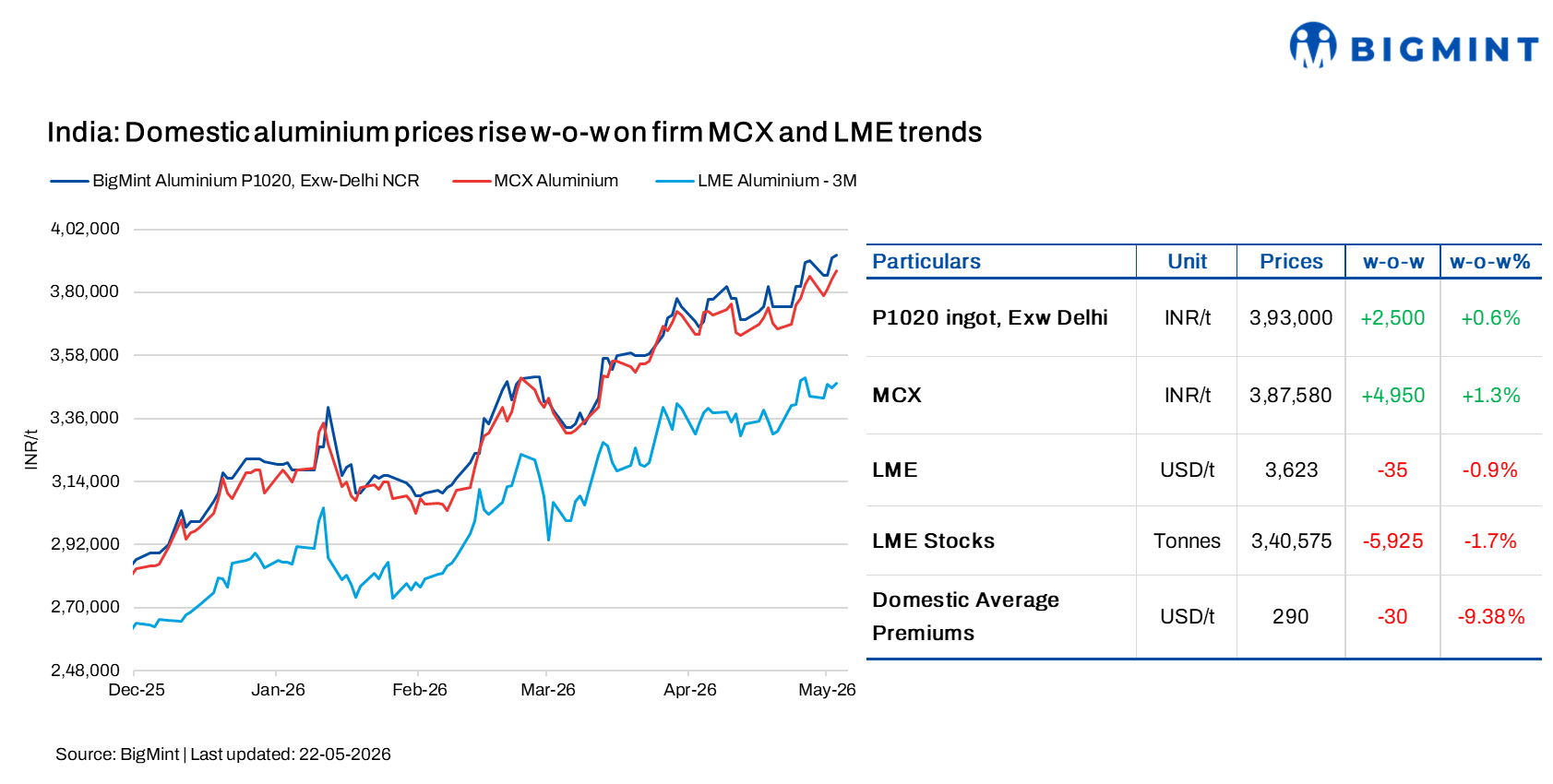

Domestic aluminium prices in India increased w-o-w as of 21 May’26, supported by firm trends on the Multi Commodity Exchange (MCX) and improved producer pricing sentiment despite mixed movements on the London Metal Exchange (LME).

As per market assessments, P1020 ingot prices in Delhi NCR increased by INR 2,500/t, or 0.6%, w-o-w to INR 393,000/t on 21 May from INR 390,500/t on 14 May. Similarly, Ex-Mumbai P1020 ingot prices rose by INR 2,000/t, or 0.5%, to INR 392,000/t from INR 390,000/t during the same period.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX increased w-o-w by INR 4,950/t, or 1.3%, to INR 387,580/t on 21 May from INR 382,630/t on 14 May, supported by improved domestic buying sentiment and recovery in global aluminium prices despite continued market volatility.

In the global market, three-month aluminium prices on the LME declined by $35/t, or 0.9%, w-o-w to $3,623/t on 21 May from $3,657/t on 14 May.

Market sentiment remained supported on continued declines in LME warehouse inventories, tightening exchange availability, and persistent supply-side concerns linked to Middle East disruptions and logistical risks around the Strait of Hormuz. However, some correction in aluminium prices during the week amid macroeconomic uncertainty and cautious buying activity limited further upside across global markets.

Market updates

A major primary producer reported that domestic P1020 aluminium premiums remained softer at $290-300/t, amid a sharp recovery in global benchmark prices and persistent tightness in near-term supply conditions. Market participants noted that buying activity has become relatively cautious at elevated price levels; however, the strong rebound in LME prices along with declining exchange inventories continued to support domestic offers. Although material availability remained stable, rising replacement costs have increasingly influenced market sentiment and pricing trends.

NALCO’s primary aluminium ingot (P1020, 99.7%) prices declined by INR 3,900/t, or around 1%, w-o-w following the company’s latest price revision, reflecting some correction in domestic producer pricing amid softer global aluminium trends.

Meanwhile, BALCO recorded a 1.7% w-o-w increase, with average prices rising to INR 421,083/t from INR 413,917/t, while Hindalco prices increased by 1.6% to INR 418,250/t from INR 411,625/t during the same period.

European primary aluminium faces energy cost pressure

European primary aluminium producers continued to face mounting pressure from elevated energy costs, as higher TTF gas prices drove electricity expenses across the region. Market participants indicated that smelters lacking long-term power agreements remained highly exposed to spot power volatility, raising concerns over lower operating rates and delayed capacity restarts. The ongoing energy uncertainty has also reinforced the importance of secondary aluminium, given its significantly lower power consumption compared to primary production.

Meanwhile, Europe P1020 premiums were heard at $600-610/t amid relatively tighter supply conditions. In Asia, import premiums were reported at $260-365/t CIF Thailand, $270-370/t CIF Vietnam, and $280-340/t CIF Japan.

Outlook

Indian aluminium prices are likely to remain supported in the near term, aided by firm MCX trends, tighter global inventories, and ongoing supply-side concerns linked to Middle East disruptions. While cautious buying and macroeconomic uncertainty may limit sharp gains, elevated energy costs in Europe and firm global P1020 premiums are expected to support overall primary aluminium market sentiment.

Leave a Reply