- LME aluminium stays resilient on supply-side concerns

- Downstream industries seek duty cut amid rising raw material costs

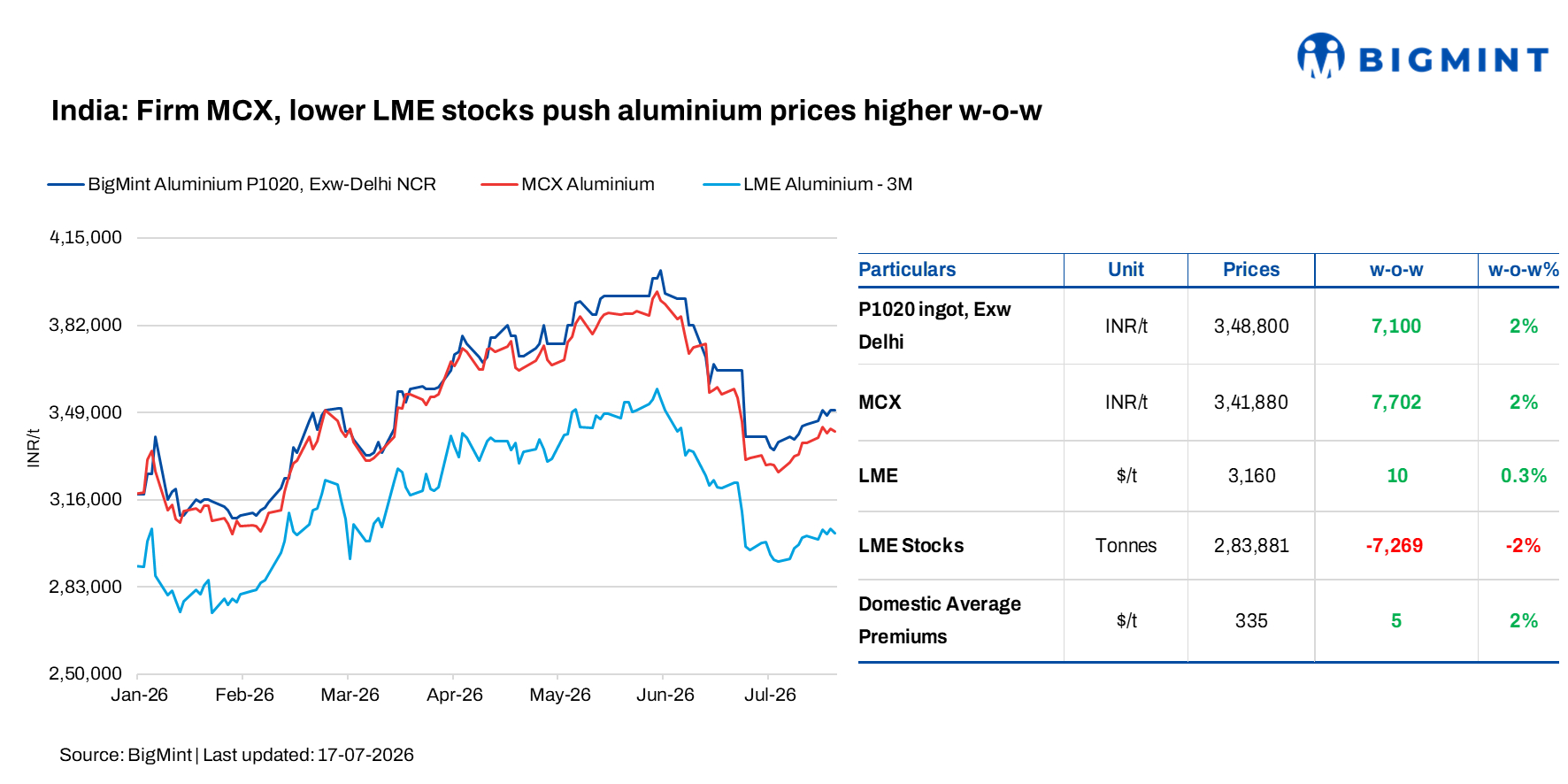

Domestic aluminium prices in India continued to strengthen w-o-w as of 17 July 2026, supported by firmer trends on the Multi Commodity Exchange (MCX) and the London Metal Exchange (LME), despite monsoon-driven subdued buying activity in the physical market.

According to BigMint’s assessments, P1020 aluminium ingot prices in Delhi NCR increased by INR 7,100/t (2%) w-o-w to INR 348,800/t on 17 July, from INR 341,700/t on 10 July.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX rose by INR 7,702/t (2%) w-o-w to INR 341,880/t from INR 334,178/t in the previous week.

Meanwhile, three-month aluminium prices on the LME edged up by $10/t (0.3%) to $3,160/t from $3,150/t. At the same time, LME aluminium inventories declined by 7,269 t (2%) to 283,881 t, indicating continued tightness in exchange stocks and providing support to global aluminium prices.

Market updates

The domestic aluminium market remained firm during the week, supported by stronger MCX trends and declining LME inventories. Although gains on the LME were modest, the continued drawdown in exchange stocks reinforced concerns over global metal availability, keeping overall market sentiment positive.

Demand, however, remained subdued as the ongoing monsoon season continued to weigh on consumption across key end-user industries. Market participants noted that most buyers are procuring material only for immediate requirements, with limited appetite for inventory build-up amid volatile global price movements.

Across Asia, aluminium premiums remained largely stable despite sluggish trading activity. Japanese buyers continued purchasing only prompt cargoes while awaiting clarity on Q4 contract premiums. The broader Asian market also witnessed limited enquiries, with sellers lowering offers amid expectations of additional supply from the Middle East and Indonesia. In India, domestic aluminium premiums remained firm at around $330-340/t, supported by tight primary metal availability despite muted demand.

Meanwhile, downstream aluminium manufacturers have urged the Ministry of Mines to reduce the effective 8.25% import duty on primary aluminium, stating that the current tariff structure has enabled import-parity pricing by domestic producers, significantly increasing raw material costs. Industry associations highlighted that margins of downstream MSMEs have compressed by up to 70%, while rising global aluminium prices have pushed input costs higher by 20-35% over the past three months. They also raised concerns over an inverted duty structure, under which several finished aluminium products continue to enter India at low or zero duty under various FTAs.

In Western markets, European aluminium premiums remained under pressure due to ample replacement supply from Canada and Indonesia and seasonally weak demand. The US premium, meanwhile, stayed broadly stable as slower summer demand offset support from declining global inventories and ongoing geopolitical uncertainties.

Outlook

Domestic aluminium prices are expected to remain firm in the near term, supported by stronger MCX trends, lower LME inventories, tight supply, and stable regional premiums. However, monsoon-related demand weakness is likely to keep physical buying largely requirement-based. Market participants will also closely monitor developments on the proposed import duty rationalisation, as any policy change could influence domestic primary aluminium pricing and improve raw material availability for downstream manufacturers in the coming months.

Leave a Reply