- OEMs attempting to negotiate Feb settlements lower

- Market awaits Mar’26 automaker settlements

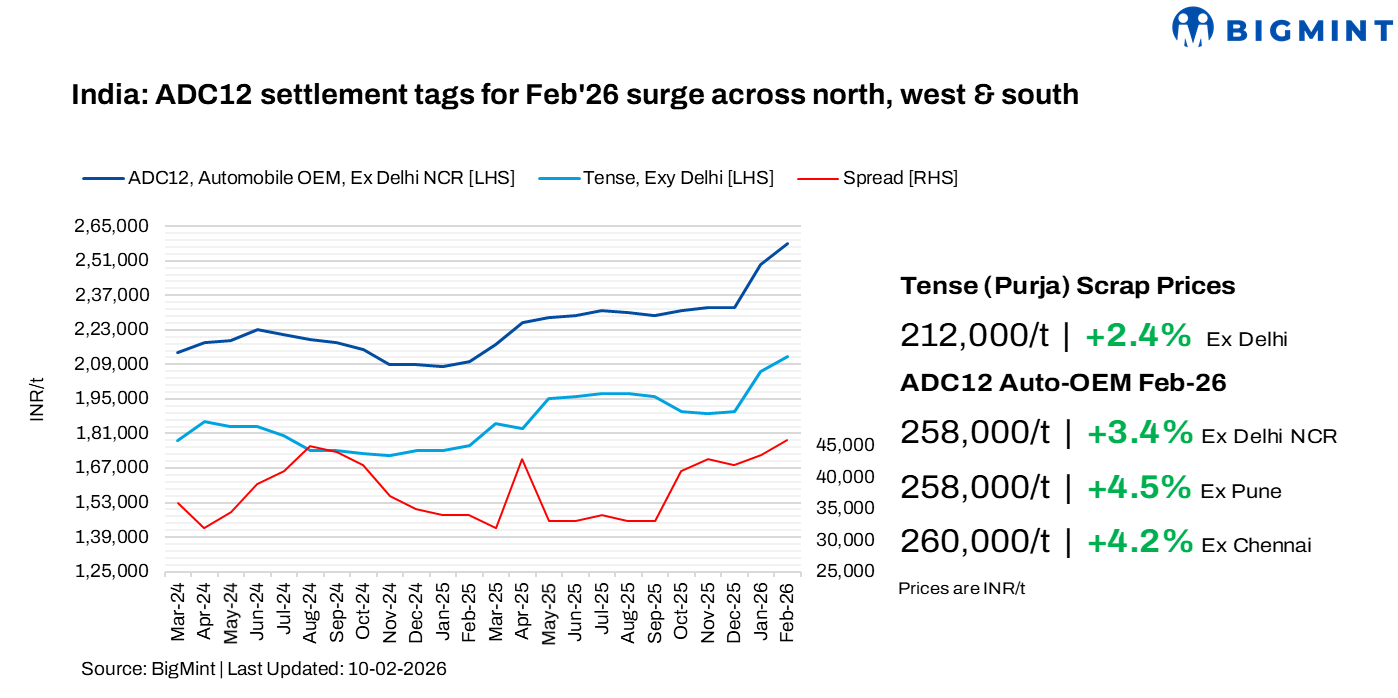

India’s aluminium ADC12 alloy ingot prices surged m-o-m in February 2026 across regions amid a rise in raw material prices and sustained firm auto demand.

BigMint’s monthly assessment for OEM-grade ADC12 showed slight price hikes across key regions:

Delhi: INR 258,000/t, up by 3.4% m-o-m

Pune: INR 258,000/t, up by 4.5% m-o-m

Chennai: INR 260,000/t, up by 4.2% m-o-m

These prices are based on 30-day payment terms.

The spread between scrap and semi-finished products stood largely steady, hovering between INR 44,000-46,000/t in both Delhi NCR and Chennai, due to similar increases in scrap and ingot prices.

Market insights

Market participants across regions indicated that suppliers’ offers for ADC12 during early February were on the higher side, ranging between INR 256,000-265,000/t. However, OEMs continued to actively negotiate lower settlement levels for February 2026 deliveries, typically targeting INR 255,000-260,000/t on standard 30-day payment terms.

In Delhi, supplier offers were heard at INR 259,000-260,000/t, while bids remained lower at INR 255,000-257,000/t. In Pune, offers were quoted at INR 260,000-262,000/t, with OEMs negotiating transactions in the INR 256,000-257,000/t range.

In the south, suppliers were offering ADC12 at relatively higher levels of INR 262,000-265,000/t, while bids were largely seen around INR 256,000-258,000/t.

A secondary producer from the south noted that while most participants are broadly aligned, resistance remains among buyers unwilling to commit beyond INR 255,000/t. That said, offers have been firming above INR 262,000/t and reaching up to INR 265,000/t, particularly in the southern region, driven by notable scarcity in domestic scrap availability and higher imported scrap offer levels.

Most market participants expect prices in the southern region to remain in the INR 260,000-265,000/t range until mid-February, with expectations of a potential turnaround toward INR 267,000-270,000/t toward the latter half of the month.

Another producer reported selling ADC12 at INR 254,000/t on an immediate payment basis, ex-Chennai, adding that prices for 30-day payment terms should be closer to INR 260,000/t.

Meanwhile, feedback from OEMs and automobile manufacturers suggests that February 2026 settlements are still pending, with negotiations ongoing as current offer levels are perceived to be elevated.

Alloy imports plunge y-o-y

Imports: India’s ADC12 alloy market saw a sharp decline in imports in CY’25, with inbound volumes falling 44% y-o-y. Total ADC12 ingot imports dropped to 12,539 t in CY’25, compared with 22,431 t in CY’24. This was mainly due to the BIS certification issues in the initial months of 2025 despite India having an FTA advantage with major supplying countries like Malaysia.

Exports: India’s ADC12 exports saw limited growth in 2025, rising 4% y-o-y to 9,850 t, as strong domestic automotive demand absorbed most production. Japan remained the key destination, with exports up 4% to 8,810 t, though gains were incremental amid subdued Japanese automotive demand and limited new contract volumes.

LME price movements

LME aluminium prices averaged $3,077/t in early February, holding firm m-o-m.

Meanwhile, LME inventories declined to 492,489 t, down 1% from 498,670 t in the previous month, reflecting continued stock drawdowns.

Aluminium prices strengthened amid tightening supply conditions and improving demand signals. Chinese smelters are nearing government-imposed capacity caps, limiting further output growth, while a sharp decline in SHFE inventories further highlighted underlying supply tightness in the market.

Raw material trends

In February, imported aluminium scrap prices moved higher, supported by firm average LME aluminium prices to $3,080/t amid supply-side concerns. In line with imported scrap trends, domestic aluminium scrap prices — particularly casting-grade scrap used in ADC12 production — also strengthened as availability tightened, especially in the southern region.

Notably, tight scrap supply in the Delhi market led to a price increase of INR 5,000/t, with levels reaching INR 212,000/t, while in Chennai, prices rose by INR 12,500/t to INR 216,000/t during February.

Among key imported grades, US-origin Tense stood firm m-o-m at $2,135/t, while UK-origin Wheels increased by $30/t to $2,875/t.

Meanwhile, Chinese silicon 553 prices remained largely stable at $1,350/t CFR Mundra amid steady demand.

Outlook

ADC12 market sentiment is expected to remain positive in the near term, supported by firm automotive demand and continued tightness in domestic and imported scrap availability. While ongoing OEM negotiations may keep buying cautious, improving supply discipline among producers and sustained raw material cost pressure are likely to underpin the market. Meanwhile, market participants are awaiting major automakers’ price settlement levels for March 2026, which could further influence buying activity and sentiment.

Leave a Reply