- Scrap supply tightens, pushing up ADC12 prices

- ADC12 alloy imports fall by 44% y-o-y in CY’25

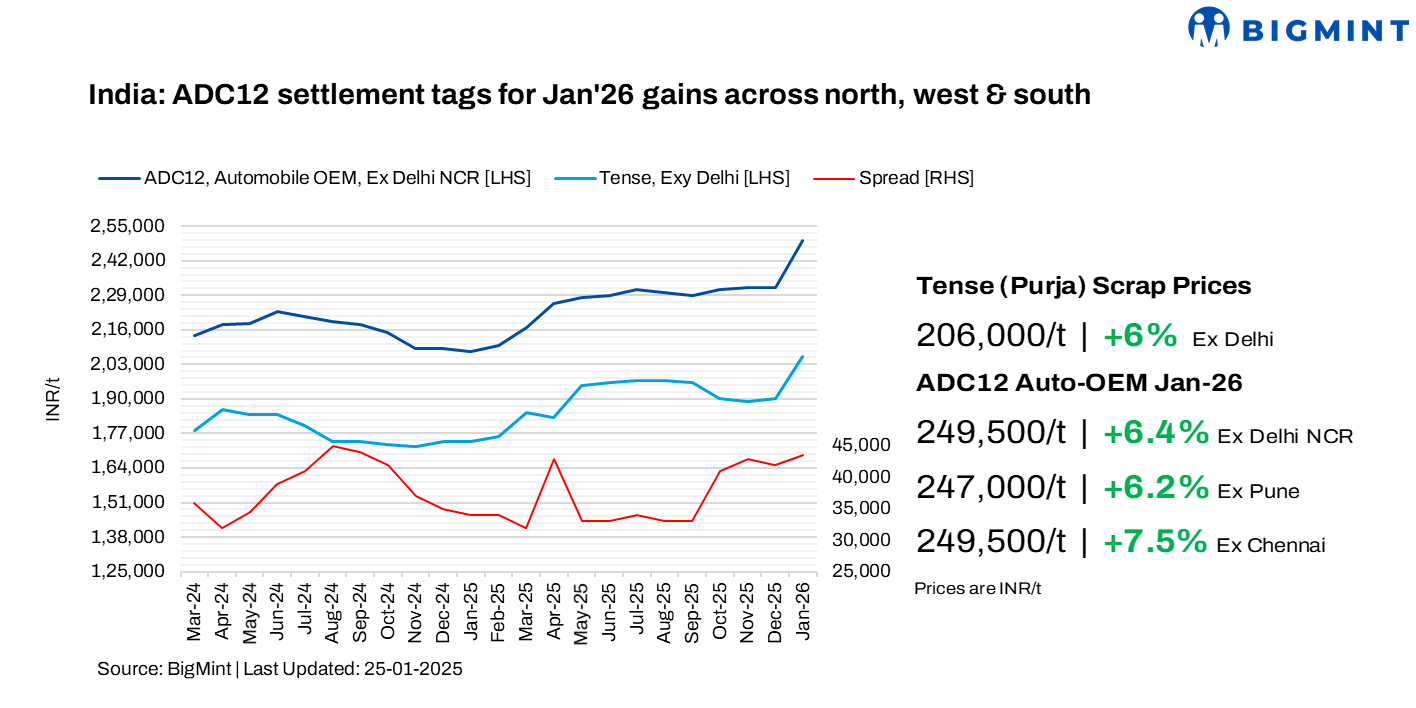

India’s aluminium ADC12 prices moved upward in January 2026, supported by rising raw material prices both domestically and globally. Automotive sector demand continued to provide positive support, despite an m-o-m slowdown in sales in December. Meanwhile, the price spread between ADC12 and scrap narrowed slightly, driven by a sharper increase in scrap prices compared with ingot prices. Import conditions remained favourable following the easing of ADC12 restrictions, even though import volumes declined on a y-o-y basis.

ADC12 prices in Jan’26

BigMint data shows that average OEM ADC12 prices for January increased by up to INR 17,500/tonne (t) m-o-m across the northern, western, and southern regions. Notably, the Chennai market registered the sharpest rise of INR 17,500/t to INR 249,500/t. This was followed by Delhi and Pune, where prices increased by INR 15,000/t to INR 249,500/t and INR 247,000/t, respectively, according to BigMint’s bi-monthly assessments.

Meanwhile, the price gap between scrap and semi-finished products narrowed to INR 43,000-47,000/t due to a more pronounced rise in domestic scrap prices.

Additionally, a leading Indian automaker has raised its ADC12 settlement price by INR 7,200/t m-o-m to INR 243,100/t for February 2026, marking the second increase of the year. The price hike was driven by rising raw material costs and firm demand from the automobile segment.

Market dynamics in early Feb’25

Market feedback across regions indicated that supplier offers for ADC12 during late January were on the higher side, ranging between INR 250,000-258,000/t across regions. However, OEMs were actively negotiating lower settlement levels for February 2026 deliveries, typically in the range of INR 247,000-250,000/t on standard 30-day payment terms.

In the Delhi market, supplier offers were heard at INR 251,000-254,000/t, while bids were at INR 249,000-248,000/t. Meanwhile, in Pune, offers stood at INR 250,000-252,000/t, with OEMs negotiating transactions in the range of INR 247,000-249,000/t.

In the southern region, suppliers were reportedly offering ADC12 at INR 255,000-258,000/t, whereas buyers bid around INR 253,000-254,000/t.

Raw material trends

In January, imported aluminium scrap prices moved higher, supported by an 8.4% increase in average LME aluminium prices to $3,138/t amid supply-side concerns. In line with imported scrap trends, domestic aluminium scrap prices — particularly casting-grade scrap used in ADC12 production — also strengthened as availability tightened, especially in the southern region.

Notably, tight scrap supply in the Delhi market led to a price increase of INR 11,000/t, with levels reaching INR 206,000/t, while in Chennai, prices rose by INR 14,000/t to INR 202,000/t during January. The rise in domestic scrap prices closely mirrored reduced procurement of imported aluminium scrap in December 2025, driven by higher landed costs due to elevated LME aluminium prices and exchange rate pressures. As a result, secondary alloy producers increasingly turned to the domestic market for raw material sourcing, exacerbating local supply constraints.

Among key imported grades, US-origin Tense stood firm m-o-m at $2,100/t, while UK-origin Wheels increased by $185/t to $2,845/t.

Meanwhile, Chinese silicon 553 prices remained largely stable at $1,340/t CFR Mundra amid steady demand.

India’s scrap, ingot imports in CY’25

India’s aluminium scrap imports rose 15% y-o-y during 2025 to nearly 2 mnt compared to 1.75 mnt in the last year. The United States remained the largest supplier, shipping 0.42 mnt to India, although there was a marginal drop from CY’24 due to strong domestic scrap demand in the US, uncertainty around tariffs, and lower price viability for Indian buyers.

ADC12 imports

In contrast, India’s ADC12 imports fell by 44% y-o-y in 2025, totalling only 12,539 t compared with 22,431 t in 2024.

Auto sector performance

India’s passenger vehicle (PV) industry recorded an m-o-m drop in retail volumes in December 2025 despite a y-o-y gain. Retail sales fell 39% m-o-m to 2.02 million units, primarily driven by elevated post-festive inventory levels, aggressive dealer discounting, subdued market sentiment, and a growing preference for 2026 model-year vehicles.

The market expects FY-end purchases and sustained GST 2.0 sentiment will support demand momentum, while improving financing turnaround times and better vehicle availability are expected to further strengthen near-term sales performance.

Outlook

ADC12 prices are expected to remain elevated in February, supported by tight domestic scrap availability and elevated import costs and exchange-rate pressures. February settlement discussions in the range of INR 248,000-255,000/t reflect sustained cost-side pressure. Despite buyer resistance of INR 4,000-5,000/t, firm seller confidence, elevated scrap prices, and steady OEM demand are likely to keep prices supported through the month.

Leave a Reply