- Scrap-to-ingot spread remains largely steady

- GST cut expected to boost auto sector demand

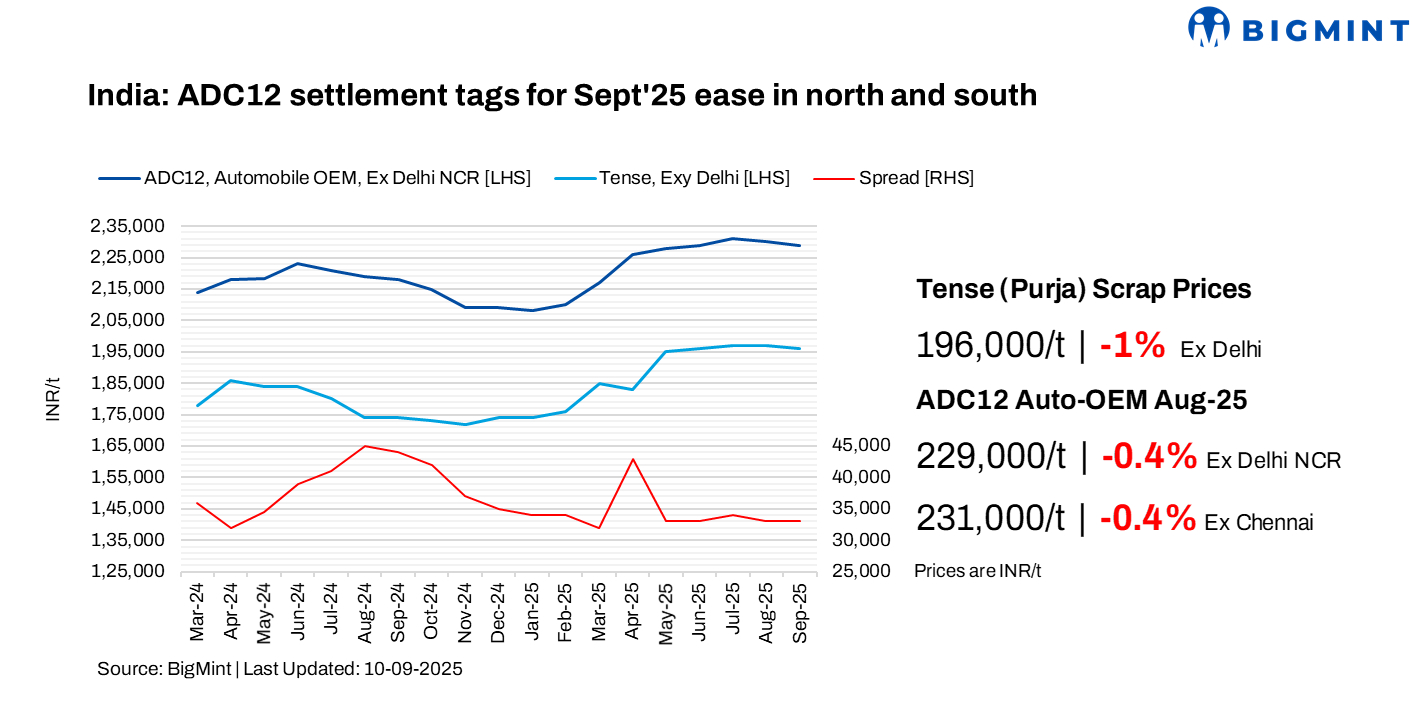

India’s aluminium ADC12 alloy ingot prices saw a slight m-o-m decline in September 2025, with marginal drops seen across both northern and southern regions, according to BigMint’s benchmark assessments.

BigMint’s monthly assessment for the OEM grade of ADC12 stood at INR 229,000/tonne (t) in Delhi and INR 231,000/t in Chennai, both down by INR 1,000/t m-o-m.

The spread between scrap and semi-finished products stood largely steady m-o-m at INR 33,000-34,000/t in both Delhi NCR and Chennai.

Meanwhile, three-month London Metal Exchange (LME) aluminium average prices hovered at around $2,612/t in early September, up by 0.7% from the previous month’s $2,594/t. At the time of reporting, LME aluminium prices had increased to $2,627/t. Inventories at LME warehouses in September had inched up by 1.4% to 482,154 t from 475,485 t in August.

Market insights

Offers for ADC12 remained on the higher side in both north and south India, hovering between INR 230,000-231,000/t in Delhi and INR 232,000-233,000/t in Chennai.

Bids in the north were heard at INR 227,000-228,000/t and in the south at INR 229,000-230,000/t.

Indicative ADC12 prices for 30-day payment terms in the west were heard between INR 227,000-228,000/t ex-Pune.

The recent GST cut on vehicles is expected to boost demand in the automotive sector, increasing consumption of ADC12 used in die-casting, especially as aluminium gradually replaces steel. Higher sales, particularly in entry-level cars, will support prices, while smoother GST implementation and improved affordability may further stabilise or even raise ADC12 prices amid steady demand.

Alloy imports plunge y-o-y

Imports: India’s ADC12 alloy market witnessed a dramatic contraction in imports during the first seven months of 2025 (7MCY’25), with inbound volumes plunging by 79% y-o-y. Total ADC12 imports stood at just 3,308 t, down sharply from 15,421 t in 7MCY’24.

Most of the imported material was from Malaysia, followed by Togo and Senegal.

Export: India’s ADC12 exports in 7MCY’25 stood at 845 t, almost three times lower than 2,342 t in the same period last year. Export volumes were strong in the initial two months but started declining from March 2025 onward, as robust domestic demand absorbed a larger share of supply.

Raw material price trends

In early September, prices of the basic raw material for aluminium alloys, that is scrap, saw a slight dip m-o-m. US-origin Tense (6-7%) scrap inched down by $20/t m-o-m to $1,960/t, while UK-origin Wheels fell by $5/t to $2,565/t. Meanwhile, Zorba 95/5 from the UK stood at $2,130/t CFR west coast, India, down by $5/t m-o-m.

In the domestic market, Tense scrap prices dropped by INR 1,000/t to INR 196,000/t in Delhi, while in Chennai, prices were assessed at INR 199,000/t ex-Chennai.

Silicon price trends

According to BigMint’s assessment, prices of China’s 553-grade silicon fell by $15/t m-o-m to $1,355/t CFR Mundra. The decline was primarily driven by an inventory build-up, which weighed on prices.

Outlook

ADC12 prices in north and south India are expected to remain range-bound through September and into October, supported by festive season demand despite weaker scrap prices. Market participants anticipate that major automakers will maintain stable pricing in October. Additionally, the recent GST cut on vehicles is likely to boost automotive demand, potentially increasing ADC12 consumption by 5-8%, limiting chances of any significant price correction.

Leave a Reply