- Imported coal costlier than domestic, yet China continue strong coal imports

- Buyers rely on contracts, quality needs, and supply security despite inversion

A curious situation has developed in China’s coal market. Despite strong international coal prices driven by supply constraints in Indonesia and steady demand from India, imported coal arriving at Chinese ports remains consistently more expensive than equivalent domestic coal. This situation, known as price inversion, would normally discourage imports. Yet Chinese imports continue. Understanding this paradox reveals the complex forces at play.

The inversion explained

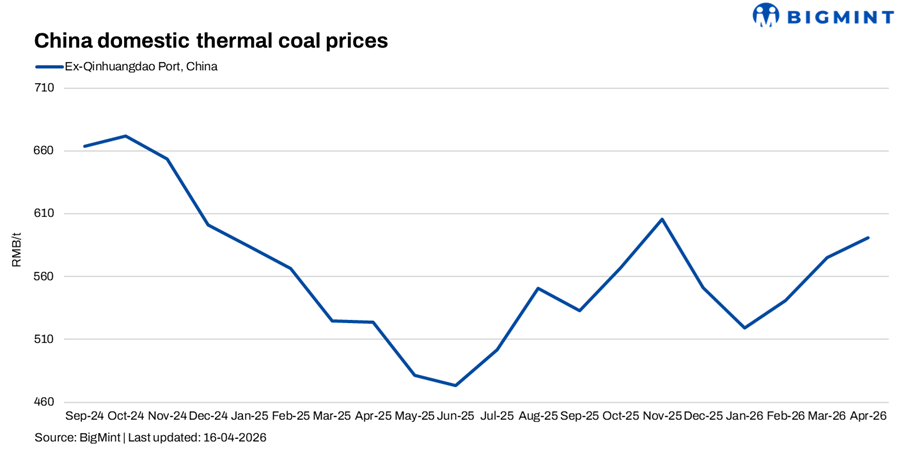

The term “inversion” simply means that imported coal costs more than domestic coal after all shipping, taxes, and fees are accounted for. The data clearly shows this is happening. For example, imported Indonesian coal of around 3,800 kilocalories per kilogram was landing at Chinese ports at a cost equivalent to roughly RMB 608/t, while domestic coal of a similar grade was available at around RMB 596/t, making the imported product more expensive. This is not a small difference, and for higher grades, the gap is even larger, with 5,500 kcal/kg imported coal priced near 824 yuan per ton (CFR) compared with domestic coal at around 766 yuan per tonne, reflecting a premium of about 58 yuan per ton.

Yet the import volumes tell a different story. In March, China imported 39.06 million metric tons of coal, a slight increase from the same month last year. For the first quarter as a whole, imports reached 116.2 million metric tons, up 1.3% year-on-year.

Why buy at a loss?

Several factors explain why Chinese buyers continue to purchase more expensive imported coal. First, some imports are tied to long-term contracts signed months or even years ago. Cancelling these contracts is not a simple option. Second, certain industrial users require specific coal qualities that are not easily available from domestic mines. For these buyers, the alternative is not cheaper domestic coal but no coal at all.

Third, there is a strategic element. Power plants and large industrial users maintain relationships with multiple suppliers to ensure security of supply. Even if imported coal is more expensive today, maintaining those supply lines is valuable insurance against future domestic shortages or price spikes. Finally, some traders are betting that domestic prices will eventually rise to meet international levels, closing the inversion gap and generating profits.

Shift to ultra-low grades

Interestingly, the pattern of imports is changing in response to the inversion. Chinese buyers are shifting their attention toward ultra-low calorific value Indonesian coals, in the range of 3,000 to 3,800 kilocalories per kilogram. The inversion gap on these lower grades is smaller, making them less painful to purchase.

Offers for Indonesian 3,400 GAR coal were heard at around $40-41 per metric ton on a Free-on-Board basis. Chinese power plants have shown active interest in these grades, even as they step back from purchasing medium-calorific value coals. This suggests a tactical adjustment: buyers are not abandoning imports but are changing which grades they target to minimize the financial impact of the inversion.

Outlook

The inversion is unlikely to disappear quickly. International coal prices remain supported by Indonesian supply limits, strong Indian demand, and geopolitical uncertainties. Domestic Chinese prices, meanwhile, are capped by stable local production and moderate demand. For the near term, Chinese importers will likely continue to operate in this challenging environment, picking their spots carefully and favouring lower-grade coals where the economics are least painful.

Leave a Reply