- Refined zinc market in surplus of 151,000 t

- Lead metal supply exceeds demand by 22,000 t

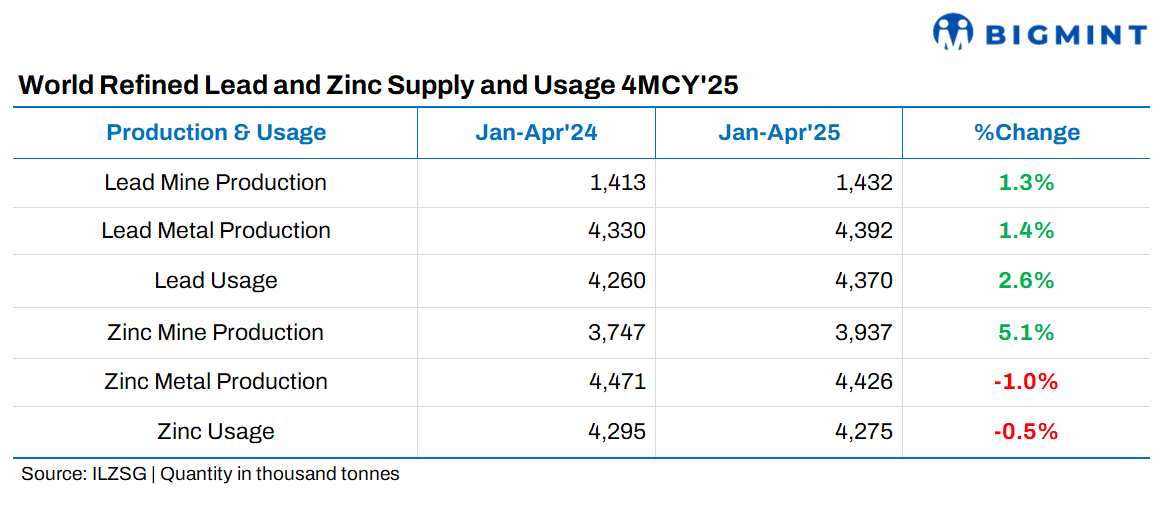

The International Lead and Zinc Study Group (ILZSG) has released preliminary data on global lead and zinc supply and demand for the first four months (January–April) of 2025.

Refined zinc supply, usage

The ILZSG reported a surplus of 151,000 tonnes (t) in the refined zinc market in 4MCY’25. Despite the surplus, global reported inventories declined by 53,000 t over the same period.

- World zinc mine production increased by 5.1%, led by output gains in Australia, China, Mexico, Peru, South Africa, and the Democratic Republic of Congo, where the Kipushi mine commenced operations in June 2024. Europe also posted higher mine output, aided by the Vares mine in Bosnia and Herzegovina, the launch of the Ozernoye mine in Russia (September 2024), and the restart of the Tara mine in Ireland (October 2024).

- Global refined zinc metal production fell by 1%. This was largely attributed to declines in Brazil, Kazakhstan, and Japan, where Toho Zinc’s Anakka operation closed. The Republic of Korea also saw reduced output due to a temporary suspension at the Seokpo smelter. However, these decreases were partly offset by higher output in Australia, Peru, and Europe, with Boliden completing an expansion at the Odda smelter.

- On the consumption side, refined zinc usage declined 0.5% globally. Demand fell in Brazil, Germany, the Republic of Korea, Türkiye, and the US, but these losses were partly counterbalanced by increased consumption in China, France, and India.

- China’s imports of zinc contained in concentrates surged 46% to 822,000 t. However, net imports of refined zinc metal stood at 120,000 t, down 19,000 t from the same period in 2024.

Refined lead supply, usage

The refined lead market registered a surplus of 22,000 t in 4MCY’25, with total reported global inventories rising by 13,000 t.

- Lead mine production grew by 1.4%, mainly driven by increased output in China, Peru, and Europe following the commissioning of new mining capacities.

- Refined lead production also rose 1.4%, supported by higher volumes in Canada, China, India, the Republic of Korea, and Sweden. These gains were somewhat offset by declines in Japan, Kazakhstan, and the UK.

- Refined lead usage increased by 2.6%, with notable demand growth in the Republic of Korea, Philippines, Taiwan (China), Vietnam, and the US. Europe also saw a usage boost, driven by the Czech Republic, France, and Germany. However, consumption was lower in India and Japan compared to the same period in 2024.

- Chinese imports of lead in concentrate form surged 43% to 255,000 t. Net refined lead imports totaled 4,000 t, compared to net exports of 12,000 t in the corresponding months of 2024.

Leave a Reply