- IMO’s Net-Zero Framework aims to achieve zero GHG emissions by 2050

- Potential rise in consumer costs, China benefit prompt dissent from US

- Immediate impact includes slowdown in R&D, regulatory uncertainty

Morning Brief: The global shipping industry’s path to net-zero is at risk, stalled by a lack of consensus over a landmark regulatory framework proposed by the International Maritime Organization (IMO).

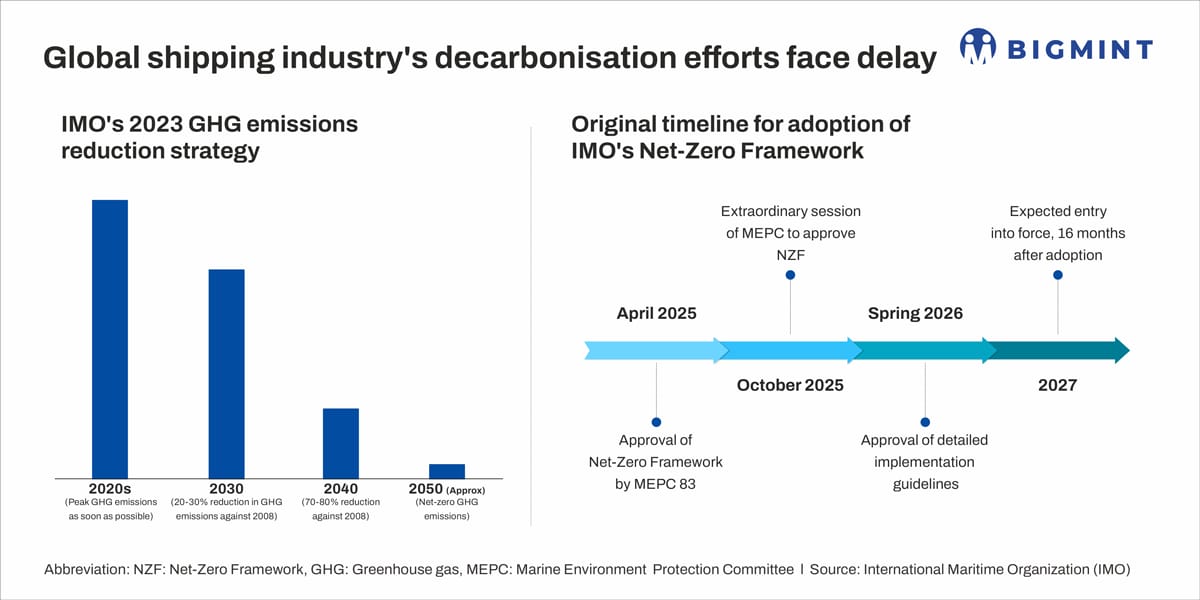

In October 2025, the adoption of the IMO’s Net-Zero Framework (NZF), which aimed to achieve carbon neutrality in maritime transport by 2050, was postponed, with a majority of member-states voting to adjourn discussions for one year.

This has pushed back the original implementation timeline by at least one year, with the NZF’s entry into force likely possible only in 2028 against the earlier expected 2027. It also marks a sharp turnaround in opinion, given that the NZF had been approved just a few months ago, in April 2025, with the majority of member states voting in support.

Key objectives of IMO’s NZF

In July 2023, the IMO, a specialised agency under the United Nations (UN) that enforces safety and environmental benchmarks for the global shipping industry, outlined key decarbonisation goals as part of its “Strategy on Reduction of GHG Emissions from Ships”:

(1) Improve the energy efficiency of new ships to reduce their carbon intensity.

(2) Reduce CO2 emissions per transport work by an average 40% across international shipping by 2030 compared to the baseline year of 2008.

(3) Increase uptake of zero or near-zero greenhouse gas (GHG) emission technologies, fuels, and/or energy sources, with these representing at least 5% and ideally 10% of the energy used by international shipping by 2030.

(4) Peak GHG emissions from international shipping as soon as possible and reach net-zero GHG emissions by or around, i.e. close to 2050.

For effective implementation, the NZF also proposes economic incentives for achieving reduction targets:

- Ships must gradually reduce their annual well-to-wake GHG fuel intensity (GFI) — the amount of GHG emitted for each unit of energy used.

- Ships exceeding GFI thresholds must purchase remedial units to balance their deficit emissions, while low-emission vessels will receive financial rewards by acquiring surplus units.

Additionally, a Net-Zero Fund will be set up to collect pricing contributions from emissions. These revenues will be used to reward green ships, fuel R&D, and support transition efforts in developing and vulnerable nations.

Points of contention

Political pressure, rather than concerns over technical feasibility, seems to have driven a divide among member-states.

According to various media reports, in the lead-up to the vote, the US had lobbied hard to get member-states states to oppose the NZF, such as by threatening retaliatory measures, including sanctions, additional taxes, and limitations on entry into US ports. The strong pushback likely stemmed from the understanding that the NZF would lead to increased costs to American consumers and would benefit China, the world’s largest ship-builder.

Saudi Arabia and other fossil fuel-producing states also echoed the US’s concerns about potential disruptions to global trade.

As per BigMint’s sources, disagreement also emerged on carbon pricing, cost-sharing, and transition equity. “Developing economies raised concerns that a global fuel levy could inflate trade costs without adequate financial or technological support. There were also practical worries around the readiness, safety, and availability of alternative fuels,” stated a leading shipper.

Notably, besides the obvious problems of limited supply and high costs, the usage of methanol and ammonia, the two front-runners in terms of alternative fuels, also raises significant safety concerns due to their toxic nature. Additionally, reports have suggested that the production of biofuels may also cause environmental strain. This is because biofuel crop cultivation will require natural ecosystems such as forests and grassland to be cleared and the use of machinery and fertilisers, which also undergo a carbon emissions-intensive production process.

Meanwhile, objections were also raised regarding the Net-Zero Fund, as there was a lack of clarity regarding which countries will receive disbursements and the terms and conditions of these statements.

Impact of delay

Presently, the immediate impacts are expected to be the postponement of the original IMO NZF timeline, as well as regulatory uncertainty, which would slow down investment and R&D in clean technologies and alternative fuels.

Smaller shipowners, developing markets, and unregulated trade lanes are set to be impacted to a more significant degree. These regions include the Arctic and coastal areas, small island nations, and sub-Saharan Africa. However, “regions with strong regional regulations — such as Europe under EU ETS and FuelEU Maritime — will be less affected,” a source informed BigMint. Countries without a need for external capital may continue investing in research to gain a first-mover advantage when the NZF ultimately kicks in.

Overall, the decarbonisation trajectory of the global shipping industry is likely to see increased regional divergences. Another source summed up the situation as creating “confusion in an industry that was preparing to move towards compliance.”

When is adoption likely?

The next round of IMO discussions is set to take place in October 2026. If the NZF is passed then, it will come into effect 16 months later. However, given the strong dissent towards the framework, shipping companies seem uncertain whether one year would be enough time to reach a consensus.

“Unless the concerns which stand today are duly addressed, the resistance to IMO’s NZF in October 2026 will be even greater as more parties will join the resistance,” highlighted a major shipping operator.

Another stated, “Ratification in 2026 is more likely than not, but the final framework will probably be diluted or phased. By then, regional regulations will be entrenched and early green-fuel vessels operational, providing clearer cost signals. However, compromises such as lower initial levies or longer transition timelines are likely.”

Outlook

The delayed adoption of IMO’s NZF may not stall shipping decarbonisation, but it risks making the transition more fragmented, abrupt, and costly later in this decade, especially given that IMO’s 2023 strategy mandates an interim target of a 20-30% reduction in GHG emissions against 2008 by 2030.

However, maritime trade emissions seem to be on an upward track, with OECD data suggesting that in 2019-2024, global maritime transport emissions rose 9.4% to 973 million tonnes (mnt) of CO2. “Slower progress in the mid-2020s could force sharper emissions cuts post-2030, raising compliance costs and increasing reliance on regional rather than global regulation,” stated a shipping company.

However, decarbonisation efforts are unlikely to be completely derailed. Investment in green shipping will continue, particularly by large fleet owners, liners, and cargo majors. These will be motivated by pressure from charterers, Scope 3 emission targets, and ESG-linked financing. That said, sources suggest that capital allocation to decarbonisation initiatives will be at a slower, more cautious pace. Among measures in focus are dual-fuel vessels, energy efficiency upgrades, and operational measures over single-fuel bets.

Carbon Capture Utilisation and Storage (CCUS) should be pursued more aggressively, opined a shipping company. “While it allows use of fossil fuels, the captured carbon dioxide can also find further usage. The net cost impact will not be very high.”

It is also important to note that, even before the October meeting, questions had been raised on the efficacy of the NZF’s goal of zero- or near-zero emission fuel types making up 5% to 10% of shipping fuel by 2030. As per a report from the Global Maritime Forum, there is a significant shortfall in SZEF-capable vessels despite supply being on track. Additionally, investment momentum had stalled, though this might have strengthened from the adoption of the NZF.

Leave a Reply