An above fundamentals development from the policy side of things is that “The National Development and Reform Commission, the Ministry of Industry and Information Technology, and other departments are conducting research and planning on the regulation of crude steel production for the year 2024.”

From the fundamental perspective, there are still no drivers for a reverse in ferrous commodities prices. Both rebar and HRC production increased as expected. While the rebar balance sheet is healthy HRC is still digesting its inventory. On the other hand, iron ore may be gradually regaining its position as the most resistant to fall (below its previous low) within the ferrous complex as prices are starting to affect supplies – though not enough to cause a supply contradiction.

Meanwhile, an above fundamentals development from the policy side of things is that “The National Development and Reform Commission, the Ministry of Industry and Information Technology, and other departments are conducting research and planning on the regulation of crude steel production for the year 2024.”

In general, the impact would depend on the investigation and study results. In 2023, there were also production curb speculations but not implemented eventually. Secondly, what would be the benchmark of the curb? In the previous year, NBS crude steel data was made flat YoY. Additionally, from Mysteel data, 2024’s year-to-date production is lower YoY; this suggest room for production to increase. Nonetheless, the escalation of the policy could definitely stir market sentiments.

Below NDRC release reads: “To consolidate and enhance the achievements of supply-side structural reform, in 2024, the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Ecology and Environment, the Ministry of Emergency Management, and the National Bureau of Statistics, together with relevant departments, will continue to carry out national crude steel production regulation. We will focus on energy conservation and carbon reduction, differentiate based on the situation, maintain balanced supply and demand, provide targeted guidance, support the superior and eliminate the inferior, promote the optimization and adjustment of the steel industry structure, and facilitate the high-quality development of the steel industry. To coordinate with capacity and production regulation work, relevant departments will jointly conduct a comprehensive survey of the basic equipment information of steel smelting enterprises nationwide.”

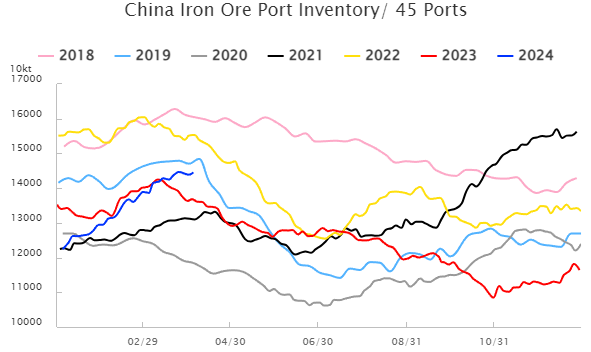

Back to the fundamentals of iron ore. While there is limited room for hot metal output to increase (this week +22.7Kt WoW to 2.2358Mt), there are signs of improvements from the supply side. At $100/t, it is unrealistic to expect major miners to reduce shipments. Instead, it would mainly affect the total shipments of marginal high-cost miners, as well as, the ratio of major low-cost miners’ shipments – which is already happening. While it is still not to the extent that it will cause a fundamental contradiction from the supply side, it reduces the margin of safety for prices to plummet deep below iron ore production costs and for the assumption that China’s iron ore inventory will build up to sky high. Of course, as with our previous reports, for bullish positions to take charge; steel inventory must be drawn down to a reasonable level (such that it is in a seasonal neutral or low level) or an above-expected increase in downstream demand.

Overall, from a valuation perspective, iron ore may be gradually regaining its position as the most resistant to fall (below it previous low) within the ferrous complex. Hence, there may be less value to chase the price decline. That said, there are still no drivers for an active long position entry.

Note: This article has been written in accordance with an article exchange agreement between Horizon insights and BigMint.