- Consumption falls 5% but scrap-based steel production up 1%

- Imports edge up on firm Asian demand despite uneven steel output

- Policy controls increasingly distorting global scrap availability

Morning Brief: Global ferrous scrap consumption declined by 5% y-o-y in CY’25 to 575.2 million tonnes (mnt) from 605.0 mnt in CY’24, reflecting weaker steel output and cautious mill buying.

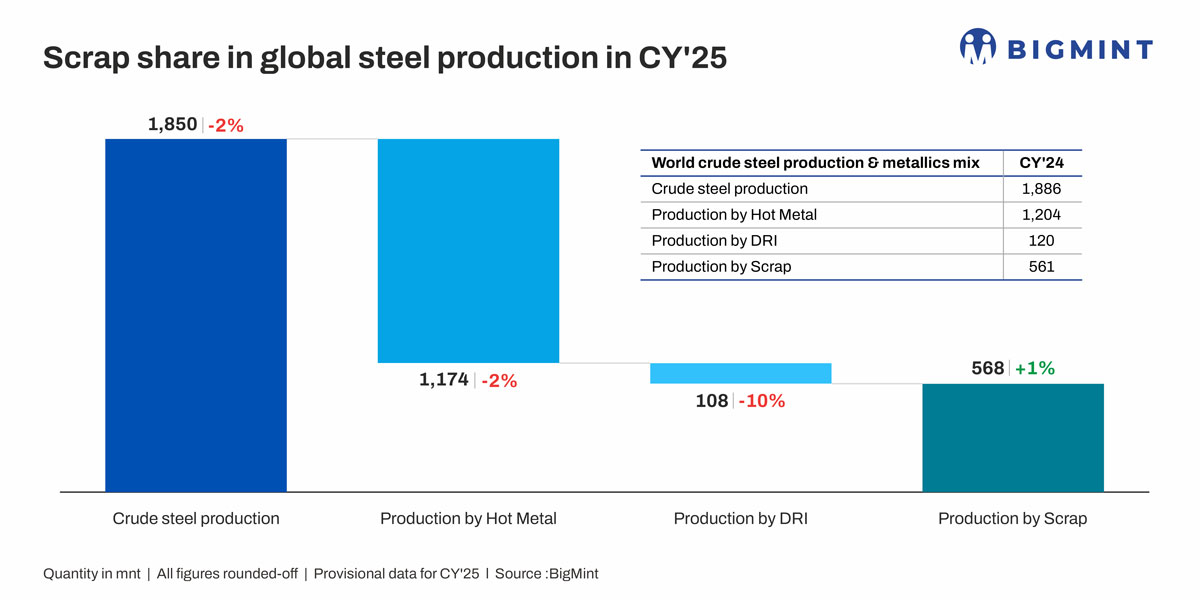

The modest fall comes amid a slight 2% dip in global crude steel production, which stood at 1,850 mnt in CY’25 from 1,886 mnt in CY’24. Production decreased across Europe, East Asia, and parts of the Americas, driven by weak downstream demand and excess finished steel supply.

Hot metal-based output declined by 2% to 1,174 mnt, while DRI-based production dropped more sharply by 10% to 108 mnt due to higher energy costs and lower utilisation.

However, scrap-based production rose 1% to 568 mnt, underscoring a structural shift towards higher scrap intensity as steelmakers prioritised cost control and decarbonisation despite a softer steel cycle.

How were consumption trends throughout CY’25?

At the beginning of the year, global ferrous scrap demand was uneven and largely driven by short-term restocking rather than sustained improvement. While January and February remained below year-ago levels, March witnessed a turnaround, with consumption reaching its CY’25 peak at 59.8 mnt on a seasonal demand recovery and inventory rebuilding.

Demand stabilised briefly in April-May but weakened from June onward, consistently trailing CY’24 levels. Volumes slipped into the low-40 mnt range during August-September and softened further in November-December, reflecting seasonal factors, weak steel margins, and inventory discipline. Demand softened across China, Europe, Japan, and South Korea, while India, Turkiye, and parts of Southeast Asia showed relative resilience.

Scrap imports rise marginally in CY’25

Global ferrous scrap imports rose modestly by 0.5% y-o-y to 59.2 mnt in CY’25, despite softer steel output in several regions, driven by continued import dependence in EAF-heavy markets, particularly in Asia.

Turkiye remained the largest importer at 18.54 mnt, though volumes fell 8% y-o-y, while India ranked second at 8.18 mnt, lower by 3% y-o-y amid higher domestic scrap and DRI use.

Thailand and Vietnam posted strong growth of 53% and 18%, respectively, while Bangladesh and Pakistan raised imports by 7% and 34% due to improved mill activity, restocking, and a low base in CY’24.

Global scrap generation, consumption by country

Country-level scrap generation and consumption data show regional divergence.

China’s scrap generation fell sharply by 13% to 193 mnt in CY’25, with consumption declining by the same magnitude due to steel output cuts and weak EAF profitability.

In contrast, India’s generation rose 22% y-o-y to 31.2 mnt, while consumption increased 16% to 39.2 mnt, leaving a wide supply gap for imports.

The US recorded a 5% drop in scrap generation to 62.4 mnt, while exports declined 19% to 11.7 mnt due to stable yet improved domestic usage.

Global scrap consumption generation

The EU remained broadly stable, reinforcing its role as a residual supplier. Turkiye saw generation rise 31% to 12.8 mnt but stayed import-dependent, while Japan and South Korea faced declining consumption amid weak steel output.

Scrap supply movement remains restricted

Global scrap supply remained constrained by policy intervention in CY’25. Russia retained quota-based export controls from January to December, limiting exports outside the Eurasian Economic Union (EAEU) to 1.5 mnt, while in 2026, the quota, which was restructured with certain licensing requirements, was increased to 2.2 mnt.

Similarly, Ukraine removed material from the export market by issuing zero-quota licenses for the full year to safeguard domestic steelmaking.

Supply tightening continued across Central Asia, with Kazakhstan extending its export ban until July 2025, Uzbekistan imposing a 100% export tariff from 1 July, Kyrgyzstan prolonging its ban until 18 September, and Armenia extending restrictions until 1 February 2026.

Meanwhile, tighter oversight in the EU from July 2025, alongside stricter checks on scrap export duty evasion in Malaysia and a ban on Syrian scrap imports into Lebanon, a transhipment hub for Turkiye, further reduced spot scrap availability.

Ferrous scrap price trends in CY’25

Q1CY’25: Weak start, cautious buying

Ferrous scrap prices entered 2025 on a soft footing across all regions. In South Asia, imported shredded and HMS prices slipped modestly from late-2024 levels as rebar demand failed to recover post-festive season and mills prioritised inventory liquidation over fresh bookings. In Turkiye also, prices also edged lower, tracking weak export rebar demand and limited mill appetite.

Q2CY’25: Sharper correction as margins erode

Prices declined more significantly in Q2 as steel margins deteriorated. Between April and June, South Asian scrap prices fell by roughly $15-25/t, driven by falling rebar spreads, tight liquidity, and lower furnace utilisation. Indian IF and EAF mills increasingly substituted scrap with sponge iron and hot metal where possible, putting a cap on scrap demand.

Turkish prices also weakened during the quarter, pressured by subdued rebar exports and growing availability of cheaper Chinese billets and slabs. EU and US faced ample scrap availability but limited buying interest, forcing exporters to discount to place cargoes.

Q3CY’25: Prices at multi-year lows, demand disconnected

The downtrend extended into Q3, pushing South Asian scrap prices to five-year lows. By September, Indian imported scrap prices had slipped below $370/t, a level not seen since 2020. Pakistan and Bangladesh followed a similar trajectory, with prices falling despite steady import volumes.

The key driver was demand weakness rather than supply. In Bangladesh, mill operating rates dropped to 35-40%, while in India and Pakistan, rebar sales remained sluggish and working capital constraints intensified. European sellers noted that even low prices failed to stimulate demand, with the market being “liquid but directionless” as buyers delayed commitments in anticipation of further downside.

Q4CY’25: Divergence emerges – Turkiye vs South Asia

The final quarter marked a clear regional divergence. South Asian prices remained depressed through October and November, reflecting weak rebar demand, tight financing, and greater reliance on low-cost domestic metallics. Even with higher y-o-y imports in Pakistan and Bangladesh, prices showed little upward movement.

By contrast, Turkish imported scrap prices rebounded sharply from early November, rising by $20-30/t within weeks and briefly moving above South Asian levels — a rare reversal last seen in late-2023/early-2024. The rebound was driven by short-term restocking, firm domestic rebar demand linked to government housing projects, winter scrap tightness in Europe, higher freights, a stronger euro, and increased EU buying from EAF mills ahead of the phase-in of the Carbon Border Adjustment Mechanism (CBAM).

On the origin side, European exporters reported tightening availability as domestic mills absorbed more scrap, while US suppliers cited weather-related collection disruptions.

Outlook

US steel tariffs and global decarbonisation policies are increasingly reshaping ferrous scrap trade flows, tightening availability without a parallel recovery in steel demand. President Donald Trump’s decision to raise steel import tariffs to 50% has lifted US mill utilisation above 80%, significantly increasing domestic scrap absorption.

With ferrous scrap exempt from tariffs, US exporters have steadily diverted volumes–particularly shredded–away from the seaborne market and into domestic mills. This trend is expected to persist through FY’26, as tariff protection continues to shield the US market from surplus Chinese steel and sustain higher operating rates.

Seasonal supply tightness has supported near-term scrap price gains, but structurally higher domestic absorption is likely to cap any sharp upside over the medium term.

At the same time, global scrap availability is being constrained by policy-led supply tightening rather than demand strength. The EU’s customs surveillance mechanism, introduced under the Steel and Metal Action Plan, alongside CBAM and stricter Waste Shipment Regulation rules, signals a clear intent to retain scrap for domestic EAF-based decarbonisation.

New EAF projects such as Tata Steel’s Port Talbot transformation will divert significant scrap volumes away from exports and into domestic use. As a result, EU scrap exports are likely to remain flat or trend lower, especially as stricter Waste Shipment Regulation rules take effect and domestic demand increases. Export restrictions across multiple regions, combined with rising scrap intensity in low-emission steelmaking, are steadily shrinking the freely tradable pool.

That said, price upside remains capped in the near term (Q1CY’26). Most market participants view the late-2025 Turkish premium as temporary, linked to seasonal and restocking factors rather than a sustained demand recovery. With South Asian steel demand still fragile and semi-finished imports continuing to pressure finished steel prices, a mild correction is likely in early 2026. Beyond that, however, scrap prices could rise, influenced by tighter global scrap availability. India, meanwhile, is expected to remain structurally import-dependent, with scrap consumption consistently exceeding domestic generation — a gap unlikely to close even with improvements in recycling infrastructure.

Leave a Reply