- Rising imports push nations to impose protectionist measures

- Excess supply drives distortions in global steel trade dynamics

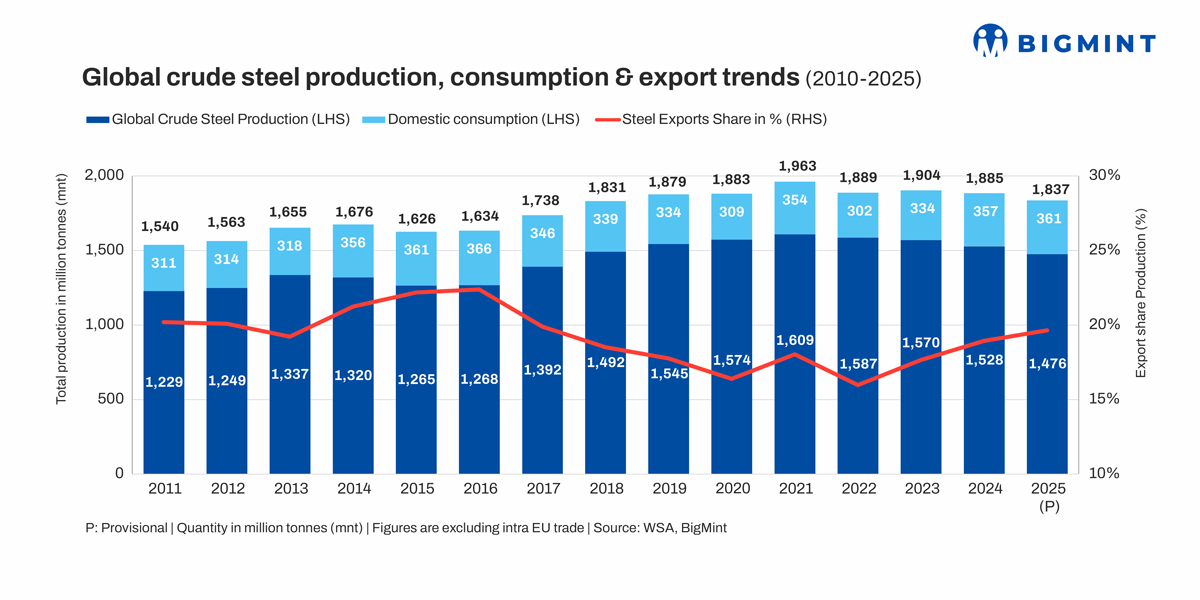

Global steel trade expanded sharply during 2022-24, growing at a Compounded Annual Growth Rate (CAGR) of 8.7%, driven largely by weak domestic demand in surplus-producing nations, particularly China. According to the World Steel Association (WSA), global steel consumption declined at a CAGR of 1.9% over the same period, while production remained broadly stable, falling only marginally by 0.1%.

This imbalance forced producers to divert excess supply to overseas markets, significantly boosting export volumes. In 2024, China alone accounted for nearly one-third of global steel exports, intensifying concerns among importing countries over market distortion, pricing pressures, and adverse impacts on domestic steel industries.

Rising trade-protective measures

This surge in exports prompted a wave of trade-protection measures in the importing countries, aimed at re-balancing trade flows. According to an Organisation for Economic Co-operation and Development (OECD) report, 19 governments initiated 81 anti-dumping investigations covering steel products in 2024, highlighting mounting global concerns over steel trade distortions. Major importing countries, including the European Union (EU), the US, Vietnam, South Korea, India, Turkey and Malaysia responded with trade defence measures to protect domestic producers amid rising imports and global price pressures.

Key measures include

Similar cycle seen in 2011-16

Between 2011 and 2016, global steel trade recorded a moderate growth of 3.3% CAGR, as total production expanded faster at 1.2% CAGR compared with 0.6% CAGR in domestic consumption. As a result, exports surged to 366 million tonnes (mnt) in 2016, equivalent to 22.4% of total global steel production, marking an all-time high which prompted various trade measures. India imposed a safeguard duty in 2016 and an anti-dumping duty on Chinese steel imports in FY’17 following the conclusion of the investigation, while the US imposed a 25% tariff on steel imports in 2018. The European Union retaliated with a similar duty the same year and subsequently imposed definitive safeguard duties on certain steel products in 2019.

Following these countermeasures, global steel exports contracted at a CAGR of 3.2% during 2016-22 (excluding fluctuations during the COVID years), while domestic consumption recovered at a CAGR of 3.8%, easing pressure on international trade flows.

Outlook

The trade protection measures have had the intended effect with growth in global steel trade falling sharply to 1.1% in 2025 and may keep global steel trade significantly disrupted in the near term. Exporting countries, particularly China, are likely to continue diverting excess supply to other markets. While the domestic steel markets in countries implementing these trade protectionist measures may receive some relief, global market volatility is likely to persist until trade flows stabilise and supply-demand imbalance improves.

Leave a Reply