- Strategic procurement shields cement producers from price spikes

- Plants pivot to cheaper thermal coal amid ample domestic supply

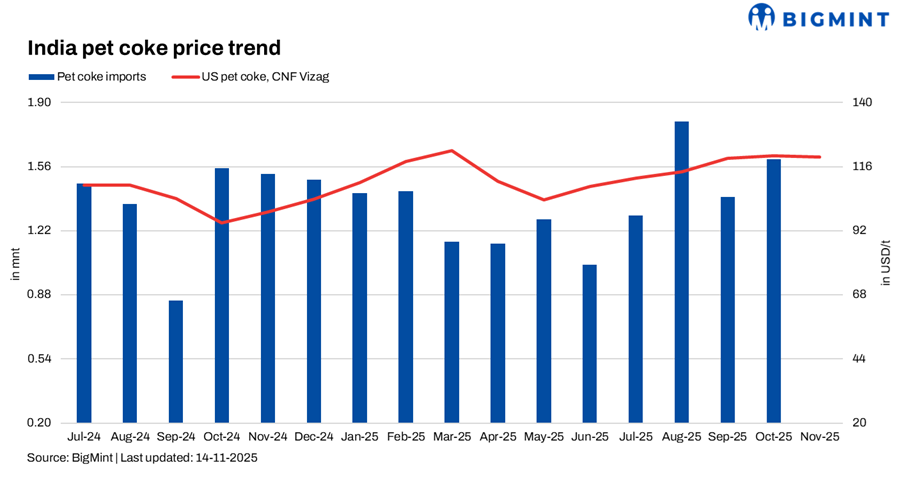

The Indian cement industry is executing a masterclass in strategic fuel procurement, effectively building a collective fortress against global price volatility. While a temporary surge in Chinese buying pushed US petroleum coke to $125-132/t CFR China, major players within the Indian market remain insulated, with many having their fuel coverage secured through the first quarter of 2026.

Multi-pronged strategy

Advance stockpiling: In the Indian cement industry, leading manufacturers demonstrated exceptional market timing, with one major producer reportedly booking 13 cargoes of pet coke in July 2025 when prices were at low levels. This forward-thinking procurement now serves as a critical buffer against current price spikes.

Seamless fuel substitution: With pet coke prices becoming untenable, plants are executing a swift and coordinated pivot to cheaper thermal coal. This is a core operational strategy, not a temporary fix. The stability of thermal coal alternatives, supported by ample domestic coal availability, provides a viable and cost-effective alternative, ensuring continuous production.

Internal arbitrage, market making: The sector’s flexibility extends to active portfolio management. Some plants have started selling their previously acquired US coal inventories on the domestic market, capitalising on price arbitrage and effectively acting as traders to optimise their overall fuel costs.

Bigger picture

This coordinated manoeuvre highlights a fundamental weakness in the recent pet coke rally. As sources indicated, the recent uptick in Chinese demand has originated from certain niche segments and is already showing signs of cooling. The stance of major Indian buyers, who have publicly stated they will only re-enter the pet coke market at $112-113/t — a full $5-10/t below recent peaks — has proven accurate. This has left the rally without a foundational buyer, confirming predictions of an imminent cool-down.

Global context confirms strategy

The cement sector’s strategic pivot to coal is well-supported by the global market structure. The stability in mid-CV Indonesian coal prices, coupled with a neutral/negative outlook for high-CV Atlantic coal, means their primary alternative fuel is both readily available and not facing imminent price inflation. This deep-seated operational flexibility ensures that even as global energy shocks occur, India’s cement production remains insulated, cost-competitive, and resilient.

Leave a Reply