- MCX prices rise 4.54%, mirroring global uptrend

- Nexa Resources’ zinc output up 9% q-o-q in Q2CY’25

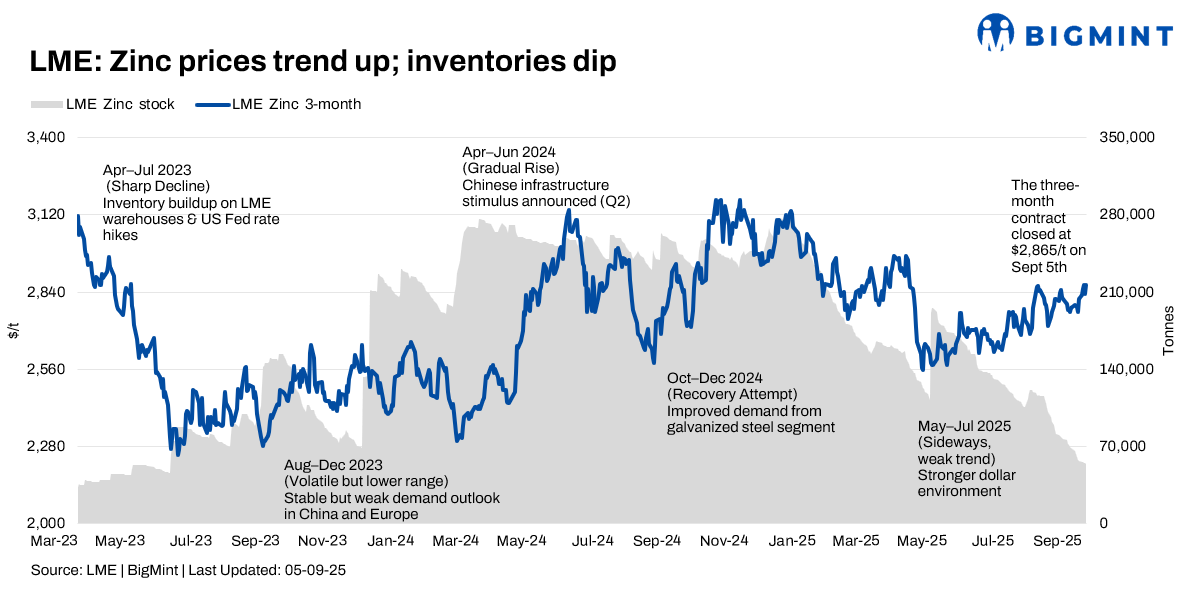

The London Metal Exchange (LME) zinc market experienced a strong uptrend during Week 35 (1-5 September 2025), largely driven by bullish sentiment following positive US economic signals and the continued decline in LME inventories. Prices surged, although there was some profit-taking later in the week.

Price trends

LME zinc cash-settlement prices trended significantly higher, reaching a high of $2,889.50/tonne (t) on 5 September against $2,840.00/t on 1 September. The three-month LME zinc contract mirrored this pattern, closing higher at $2,865.50/t on 5 September from $2,830.00/t on 1 September.

The overall upward momentum was fuelled by market optimism as US personal consumption expenditure (PCE) data met expectations, which heightened market anticipation for a September interest rate cut and subsequently softened the US dollar. However, prices saw some intraday fluctuations, reflecting profit-booking and market volatility.

LME zinc inventories continued their sharp decline during the week, falling to 54,750 t on 4 September from 55,875 t on 1 September. This continuous destocking indicates a tightening global supply of readily available zinc and provided a strong impetus for the week’s price rally.

MCX zinc trends (September 1-5)

MCX zinc prices experienced an uptrend, aligning with the recovery in global markets. The futures contract saw a 4.54% increase, to INR 277,700/t on 5 September from INR 265,650/t on 1 September. This upward momentum was driven by improving global sentiment and tightening supply. However, some profit-taking and volatility were observed during the week, reflecting mixed signals from both domestic demand and global market cues.

SHFE zinc trend

SHFE zinc prices saw an initial increase before facing some headwinds towards the end of the week. The most-traded SHFE zinc 2509 and 2510 contracts saw gains on 5 September, reaching RMB 22,115/t and RMB 22,155/t, respectively. The market was supported by expectations of US rate cuts and a weaker US dollar. However, oversupply concerns and slower domestic downstream purchasing due to rising prices likely capped significant gains.

Market updates

HZL eyes diversification into 4 new metals by 2030

Hindustan Zinc Ltd (HZL), India’s largest zinc, lead, and silver producer, plans to diversify into up to four new metals by 2030. CEO Arun Misra highlighted potential targets including neodymium, tungsten, and potash. Leveraging its underground mining expertise, the Vedanta subsidiary aims to tap hard-to-mine resources, ensuring portfolio expansion and long-term growth in critical minerals.

Nexa Resources posts 9% q-o-q rise in zinc output in Q2CY’25

Nexa Resources announced strong Q2CY’25 production and earnings, highlighted by a 9% q-o-q increase in zinc production to 74,000 t. This growth was driven by higher ore volumes and grades from Peruvian operations, alongside recovery at Aripuana and Vazante mines. Net revenues rose 13% q-o-q to $708 million, and adjusted EBITDA increased 28% to $161 million. The company expressed optimism for the second half of 2025.

Outlook

The near-term zinc outlook remains cautiously optimistic, especially for the LME market, given the continued decline in inventories and positive global macro signals. However, persistent oversupply concerns in China, coupled with varying regional demand trends, suggest continued volatility. Market participants will closely track demand dynamics, particularly in China, and monitor broader global economic signals for further direction. The divergent inventory trends between the LME and China remain a key factor to watch.

Leave a Reply