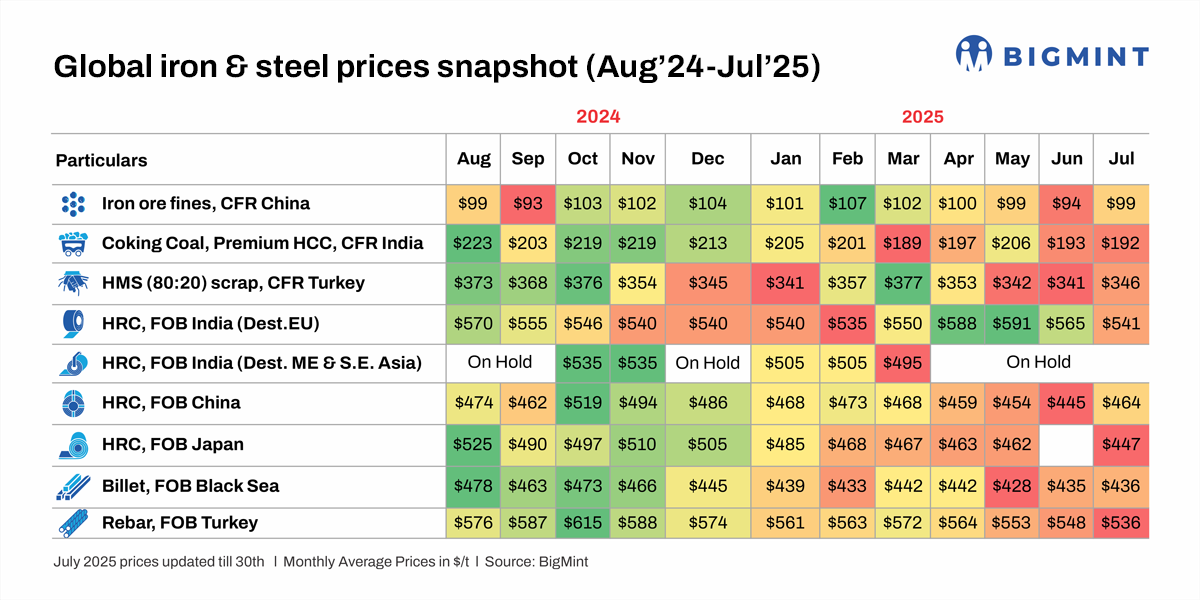

- Iron ore rises on positive macroeconomic signals

- Average Chinese HRC export offers up $19/t m-o-m

- Scrap prices post modest gains on Turkish demand

Morning Brief: Global steel and raw materials prices remained largely in the red in July 2025 as markets grappled with the impact of tariffs and restrictive measures on trade flows and supply-demand fundamentals, while US policy rates remained unchanged with the Fed assessing the impact of tariffs on the domestic economy and prices.

On the other hand, the People’s Bank of China, through successive rate hikes, tried to boost flailing demand in the world’s second-largest economy, with export prices of steel from China touching a 5-year trough in June. Policy booster doses did have a marginal impact in restoring confidence and provided some support to domestic and export prices of Chinese steel. But a broader recovery is still not in sight.

Commodity markets are anticipating slower world growth as a result of rising trade barriers and monetary conditions that are still on the restrictive side of neutral in the US. While the US tariff rates were slashed in mid-May for key countries, the redirection of supplies from Asia to major markets such as the EU will only increase competition and price pressure.

Snapshots of price movements in Jul’25

- China’s imported iron ore prices showed slight recovery in July, though average prices for the month remained below the $100-mark. Prices remained under pressure since mid-May, with the government announcing crude steel production cuts in CY’25. However, prices appreciated in the beginning of July, driven by positive macroeconomic signals, improved futures sentiment, and supportive policy news. Better margins of steel mills and regional sintering cuts led to enhanced lump demand, providing price support. Market sentiments improved following higher finished steel sales.

- Imported coking coal prices corrected marginally in July for Indian buyers. Sources informed that Indian mills were largely covered for August loading shipments. Additionally, a weaker finished steel market in India and sufficient offers for coking coal from Australia resulted in lower bids. Bid-offer disparity, too, dragged prices down.

- A flurry of deals boosted Turkish imported scrap prices in July, although prices still remained below April levels. Around 22–23 deep-sea vessels were booked from the US and Europe at $338–347/t CFR, with the majority of the deals being concluded in the second half of the month. Although rebar export prices from Turkiye edged lower, domestic construction sentiment was stable in the earthquake-hit regions and due to the upgrade of old buildings. This supported scrap demand.

- Average Indian HRC export prices to the EU dropped sharply in July to $541/t FOB. Prices have declined sharply since April. The decline is largely owing to soft demand in the EU during the summer break in the region, high energy costs affecting steel demand and production, and the possible surge in steel imports amid aggressive exports by China and redirection of cargoes due to the impact of tariffs. Indian export offers to the Middle East remain on hold.

- Chinese HRC export prices climbed up by nearly $20/t m-o-m in July as domestic HRC prices edged up towards the latter half of July, thanks to increasing SHFE HRC futures. SHFE HRC futures surged RMB 156/t ($22/t) w-o-w to RMB 3,477/t ($485/t) on 25 July against RMB 3,321/t ($463/t) on 18 July amid speculation that the government may cut coal supply and curb excess steel production. A major hydropower project boosted market optimism for future demand. The surge in domestic steel and raw materials prices boosted HRC export offers. Japanese HRC export prices, on the other hand, declined amid major global competitors such as Formosa reducing offers for July and China’s Baosteel rolling over export offers. Moreover, domestic construction sentiment, too, remained muted even as the tariff impact on exports continued to weigh heavy.

- Russian billet prices remained rangebound in July, with offers recording an uptick in early-August. Although the Russian currency depreciated somewhat in comparison with June, the uptrend in the Asian billet market amid positive Chinese policy signals, increased Chinese steel export prices, and rising raw material prices offered support to Russian billet prices. However, Egypt favouring Chinese billets over Russian cargoes limited the price increase.

- Turkish rebar export prices dropped m-o-m as seasonal monsoon rains and the summer lull continued to curb rebar demand across markets. Average prices softened in July due to the fact that mills continued to grapple with soft rebar demand and high scrap costs. A source informed that due to the decline in prices mills might consider production cuts in the days ahead. The Turkish rebar-to-scrap spread stood at $190-195/t.

Outlook

According to some estimates, the steel price cycle seems to have hit a trough in mid-2025, with prices likely bottoming out in most key regions. However, the impact of tariffs and retaliatory trade measures, energy inflation, neutral monetary policy in major countries and global supply glut are expected to weigh on construction and manufacturing demand, as well as steel prices.

Although August has started on a positive note, with Chinese steel prices and margins edging up and global majors hiking offers, it remains to be seen what the impact of government stimulus will be, especially on the debt-ridden property sector. Importantly, if the Chinese government’s mandate of crude steel production cuts in the latter half of the year materialises, global steel prices may receive a much-needed boost.

On the other hand, US steel majors such as Nucor and US Steel (Nippon Steel) may witness a period of production growth and stable prices following the imposition of 50% tariffs on steel imports. However, the mid-term impact on the economy and on steel end-users remains to be ascertained.

The EU, for its part, may see a spurt in prices in Q4CY’25 in the lead up to CBAM implementation in January 2026, with import prices likely to rise by roughly EURO 50/t. However, steel demand and production are unlikely to register any significant recovery this year.

Leave a Reply