- Chinese HRC offers hit 8-month high on rising coke costs

- Coking coal gains on sustained met coke price recovery

- Turkish rebar offers inch up but sales remain depressed

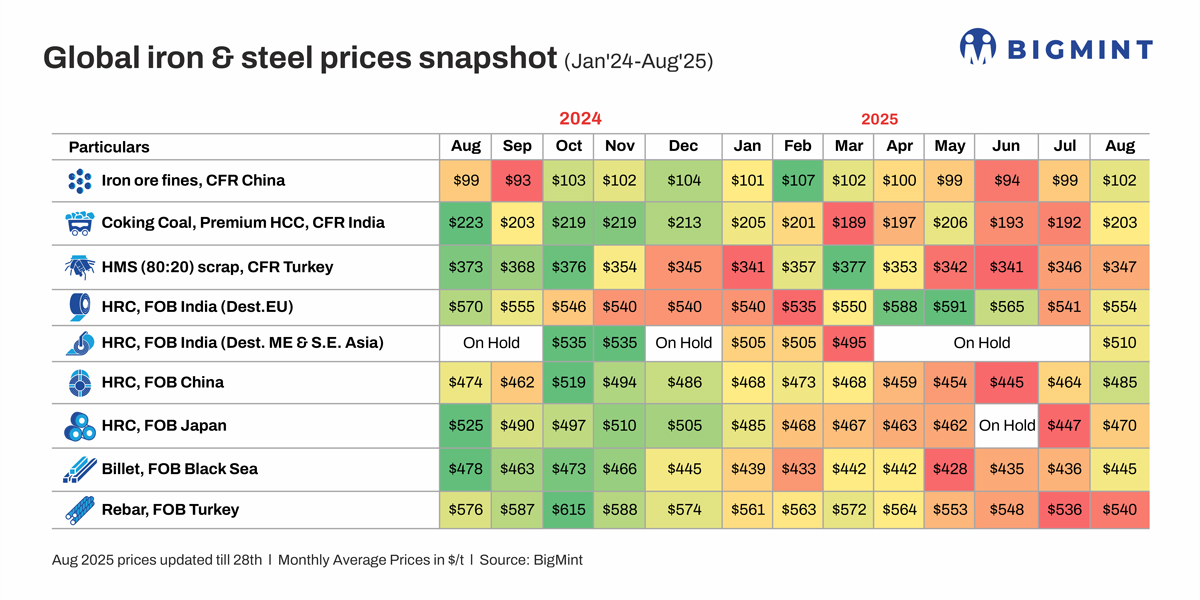

Morning Brief: Global steel and raw material prices witnessed a m-o-m recovery in August 2025, with China, the primary market-mover, witnessing bullish sentiment amid production restrictions. Chinese met coke supply tightened, which pushed up raw material costs and provided robust price support to finished products. This propelled prices in other regions and commodities.

Snapshots of price movements in Aug’25

Steel supply cuts boost Chinese iron ore fines

Benchmark Australian iron ore fines prices gained $3/tonne (t) m-o-m to a monthly average of $102/t CFR China in August. This marked a five-month high.

Notably, production restrictions were imposed in mid-August on certain steel mills based in Tangshan to combat air pollution ahead of a key military parade on 3 September. Reports also highlighted China’s plans to upgrade its steel sector in 2025-26 by eliminating inefficient and outdated capacities.

While lower crude steel output generally translates into reduced iron ore demand, industry stakeholders believe that the restrictions will help the steel sector sort out its supply glut and, consequently, lift product prices and mills’ profit margins. This strengthening is expected to percolate upstream to iron ore prices as well.

Additionally, demand was moderate this month, and bullishness in the coke market seeped into iron ore. The easing of trade tensions with the US also improved market confidence.

Coking coal stages smart rally

Coking coal prices, CFR India, recovered by a strong $11/t m-o-m to $203/t in August, fuelled by a surge in the Chinese market.

First, following a mining accident in July, authorities in China’s Shanxi province intensified safety and environmental checks on coking coal mines, which ultimately curtailed market supplies.

Downstream, met coke tags strengthened, with three rounds of price hikes agreed to by steelmakers. Met coke supply was tight, amid low inventories and a sharp reduction in production in Shandong in the second half of the month due to the Victory Day parade on 3 September. Meanwhile, demand was firm, buoyed by steady hot metal output.

Higher met coke prices directly resulted in a spike in coking coal tags.

However, Indian demand was somewhat moderated by steelmakers’ resistance to higher prices. Bids softened by the month-end amid expectations of improved availability. Indian met coke prices remained largely firm due to limited import arrivals. This also supported Indian coking coal prices.

Turkish imported scrap prices remain stable

Turkiye’s imported ferrous scrap prices were largely stable m-o-m at $347/t, inching up by $1/t. Sluggish, stagnant rebar demand in both domestic and export markets limited mills’ scrap intake, with some steelmakers reducing capacity utilisation rates. Ample scrap availability also meant that there was little urgency to procure cargo. Moreover, market activity was affected by the summer holiday lull.

However, scrap suppliers were unwilling to reduce offers, with US-based traders witnessing steady domestic demand and strong freight costs. This ultimately kept scrap prices flat m-o-m.

Black Sea billets climb on robust sales, currency weakness

Russian billet export prices climbed up by $9/t m-o-m to $445/t FOB Black Sea, influenced by robust demand in the Middle East and North Africa. According to reports, Syrian buyers showed sturdy enthusiasm following the termination of US sanctions on the country and amid reconstruction efforts due to a long-drawn civil war.

Syrian buyers were also disinclined to source cargo from afar, due to the July attack by the Houthis on a Chinese commercial vessel in the Red Sea. Compared to Chinese supplies, Russian billets offered lower freights and shorter transit times.

Additionally, currency depreciation, with the rouble falling to 80 per US dollar from around a two-year peak of 77 in July, pushed suppliers to hold their ground.

However, demand weakened gradually, with elevated freights putting off buyers amid a lack of steel demand. A slowdown in Turkish construction activity also pressured consumption.

China drives surge in global HRC export offers

Hot-rolled coil (HRC) export offers increased across regions, with China witnessing the highest uptick of $20/t m-o-m to an average of $485/t FOB, an eight-month high.

Higher raw material costs, resulting from the series of met coke price hikes, lifted Chinese prices. Some Tangshan-based rolling mills also received orders to suspend production during 25 August-3 September, which gave rise to expectations of tight supply.

Meanwhile, elevated prices dampened demand and led to cautious sentiment.

The uptrend in China also drove up Indian and Japanese HRC offers. In fact, rising Chinese values moved Indian mills to again start offering HRCs to the Middle East for the first time since March, though demand turned out to be lacklustre due to summer-time slowdown.

Indian offers to the Middle East were at $510/t FOB, while those to the EU rose $13/t m-o-m to $554/t FOB — a wide disparity, perhaps indicating buyers’ pricing expectations for the material. The spike in offers to EU was influenced by the Chinese price rise; the market was mostly inactive due to the summer holidays.

Turkish rebar offers edge up but sales remain depressed

Turkish rebar offers increased by $4/t m-o-m to $540/t FOB. Demand was restricted to immediate requirements, which supported prices, but bulk bookings were mostly absent.

Despite the persistent lack of demand, Turkish mills were unwilling to reduce prices due to narrow margins. Mills increasingly cut their utilisation rates, struggling with extended losses and ample material availability.

Outlook

All eyes remain on China for further market cues. Preliminary analysis suggests a range-bound trend, with prices hovering at these levels but under pressure from weak demand. It is to be noted that supply constraints, especially in met coke, rather than demand trends, set in motion the recent price hike. The steel supply glut continues to provoke production cuts, and such rationalisation efforts may support prices in the long run.

Leave a Reply