- Indian imported coking coal prices rise to 11-month high

- Tight winter supply, high freights lift Turkish scrap prices

- China’s HRC export offers hold firm; Indian offers fall further

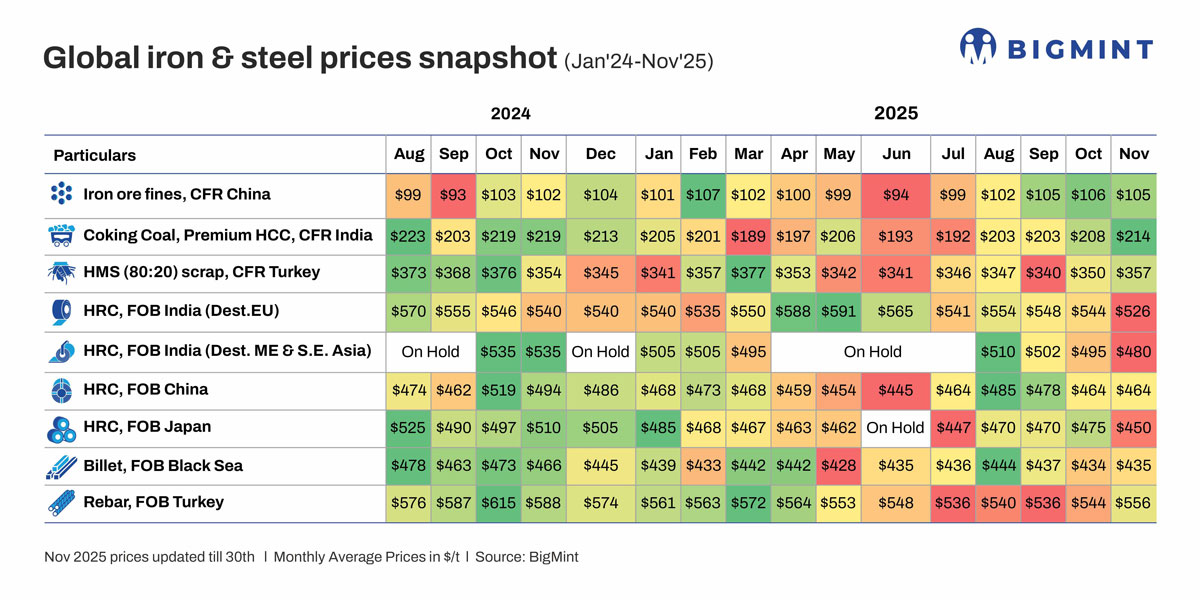

Morning Brief: Global steel and raw material prices recorded mixed trends m-o-m in November. While prices (monthly averages) increased across the scrap, billet, and rebar segments, flats fared comparatively poorly, with Indian and Japanese hot-rolled coil (HRC) export offers sliding m-o-m. However, Chinese HRC offers remained stable m-o-m due to firm iron ore and coking coal costs.

Notably, the global manufacturing purchasing managers’ index (PMI) slipped to a four-month low of 50.5 points in November, suggesting that steel demand remained tepid last month. However, material shortages emerged in certain segments, which propped up prices.

Highlights of price movements in Nov’25

Iron ore prices dip: Iron ore prices fines (Fe 62%) inched down by $1/t (1%) m-o-m to a monthly average of $105/t CFR China in November. Demand weakened primarily due to poor margins on steel sales, which led mills to undertake maintenance downtime and production cuts. Air pollution control measures, such as sintering restrictions in Tangshan, also affected demand for fines.

Mysteel’s surveys indicate that only around 35% of the 247 blast furnace (BF) mills tracked could secure profits on 27 November compared to 45% on 30 October.

Rising coke prices also pressured mills margins and capped gains in iron ore prices. Quasi Grade I was up 7% m-o-m to RMB 1,556/t exw-Tangshan in November.

Meanwhile, iron ore inventories increased slightly to 89.4 million tonnes (mnt) on 27 November compared to 88.5 mnt on 30 October, signalling inventory build-up amid lower consumption by steel mills.

However, optimism emerged, with positive sentiment regarding December’s Politburo meeting, the Central Economic Work Conference (CEWC), and the US Federal Reserve’s expected interest rate cuts supporting prices.

India’s imported coking coal prices rise to 11-month high: India’s imported coking coal prices increased by $6/t (3%) m-o-m to an 11-month high of $214/t CFR India.

Chinese steelmakers showed strong demand for imported coking coal, driven by strict safety inspections at domestic mines and low inventories. This drove price gains in Australian premium hard coking coal (PHCC) (up 3% m-o-m to $197/t), with three consecutive met coke price hikes in China supporting the uptrend.

In tandem, both Indian coking coal and met coke prices increased, with the latter up 5% m-o-m to INR 31,500/t exy-Jajpur.

However, Indian demand was limited, as steelmakers were reluctant to trade at these higher levels, given weak steel prices. To illustrate, domestic BF-rebar prices hit a five-year low in November.

As a result, bid-offer disparities emerged, with suppliers quoting $217-220/t CFR India, as assessed on 28 November, but bids were largely clustered around $210/t CFR.

Turkish melting scrap prices hit 8-month high: HMS 80:20 prices stood at an 18-month high of $357/t CFR Turkiye, rising $7/t (2%) m-o-m. The slight uptick stemmed from (1) high freights (ranging around $45/t from the US in early November), (2) tight supply and firm collection costs due to slower scrap generation, and (3) stronger demand, driven by Turkish mills winter restocking and an improvement in rebar sales.

Indian HRC export offers slide further as demand weakens: Indian HRC offers to both Europe and the Middle East and Southeast Asia slipped by 3% m-o-m. While EU-bound cargo was quoted at $526/t FOB in November, down $18/t m-o-m, offers to the Middle East stood at $480/t FOB, falling by $15/t. This marks the third consecutive month with an m-o-m decline.

Offers to Europe faced pressure, as end-user demand was weak, and market participants remained uncertain about additional tax burdens under the Carbon Border Adjustment Mechanism (CBAM). However, trade continued, though sluggishly, with India exhausting its HRC quota for Q4CY’25 by 1 December.

Offers to the Middle East softened on competitive pressure from lower Chinese prices and a slowdown ahead of the National Day holiday (2 December). Similarly, weak downstream demand and heavy rains impacted Vietnamese trade.

Cost support keeps Chinese HRC export offers flat: Chinese HRC export offers held firm m-o-m at $464/t FOB. Higher raw material costs kept prices stable, while limited demand weighed on prices. Demand from Middle East buyers, however, improved slightly.

Japanese HRC export offers plunge: Japan’s HRC export offers recorded the sharpest fall of $25/t (5%) m-o-m to $475/t. Subdued construction demand and a cautious manufacturing sector dampened domestic trading activity, while exports remained sluggish. Nippon Steel kept its HRC export prices steady m-o-m for end-November and early-December 2025 sales, while Tokyo Steel also maintained stable prices for HRC deliveries in December.

Black Sea billet prices firm up: Billet offers, FOB Black Sea, inched up by $1/t (0.2%) m-o-m to $435/t in November. Firmer Turkish rebar prices, stronger scrap values, and a rising rouble contributed to a slight uptick in offers during the month-end. Weak demand and apprehensions regarding inventory build-up during the winter had prompted some sellers to reduce offers in the middle of the month, which limited the m-o-m price rise.

Turkish rebar prices rally on stronger scrap: Turkish rebar prices recovered slightly by $12/t (2%) m-o-m to a seven-month peak of $556/t FOB, on the back of stronger-than-expected year-end sales in the domestic market. Higher scrap prices due to the winter shortage also pushed mills to lift their rebar offers.

Outlook

Chinese steel prices are expected to recover in December because of a decline in steel inventories and production. Mysteel indicates that stocks of key carbon steel products fell by 7% m-o-m during end-November, while the daily average hot metal output among BF mills was 2% lower m-o-m in November.

Higher Chinese steel prices could push up iron ore prices, and Indian and Japanese HRC export offers are also likely to rise in parallel. However, CBAM-driven uncertainties may continue to limit price gains for Indian HRCs bound for Europe.

Rising scrap prices and a winter supply shortage are likely to support Black Sea billet and Turkish rebar offers.

The outlook for coking coal also appears positive, with tight supply and winter restocking expected to lift prices.

Leave a Reply