- POSCO, JFE’s crude steel output dips by 3-5% q-o-q

- Nippon Steel’s revenue drops by 4% q-o-q in Jan-Mar

Nippon Steel, JFE Holdings, ArcelorMittal, Hyundai Steel, and POSCO Holdings, major players in the global steel industry, have published their consolidated financial results for Q1CY’25 (January-March 2025). Notably, POSCO and JFE posted lower crude steel output q-o-q. Additionally, all these steelmakers recorded a decline in revenue.

Crude steel production

Nippon Steel’s non-consolidated crude steel production remained stable q-o-q at 8.56 million tonnes (mnt) in Q4FY’24 (January-March 2025). The company’s quarterly consolidated output increased slightly by 2% q-o-q in Q4FY’24 to 9.94 mnt against 9.78 mnt in Q3FY’24.

Additionally, Nippon Steel recorded 34.3 mnt in FY’24 (1 April 2024-31 March 2025) in non-consolidated production, which inched down by 2% as compared to 34.99 mnt in FY’23 (1 April 2023-31 March 2024). Moreover, the company’s consolidated volume edged down by 2% y-o-y to 39.64 mnt against 40.51 mnt.

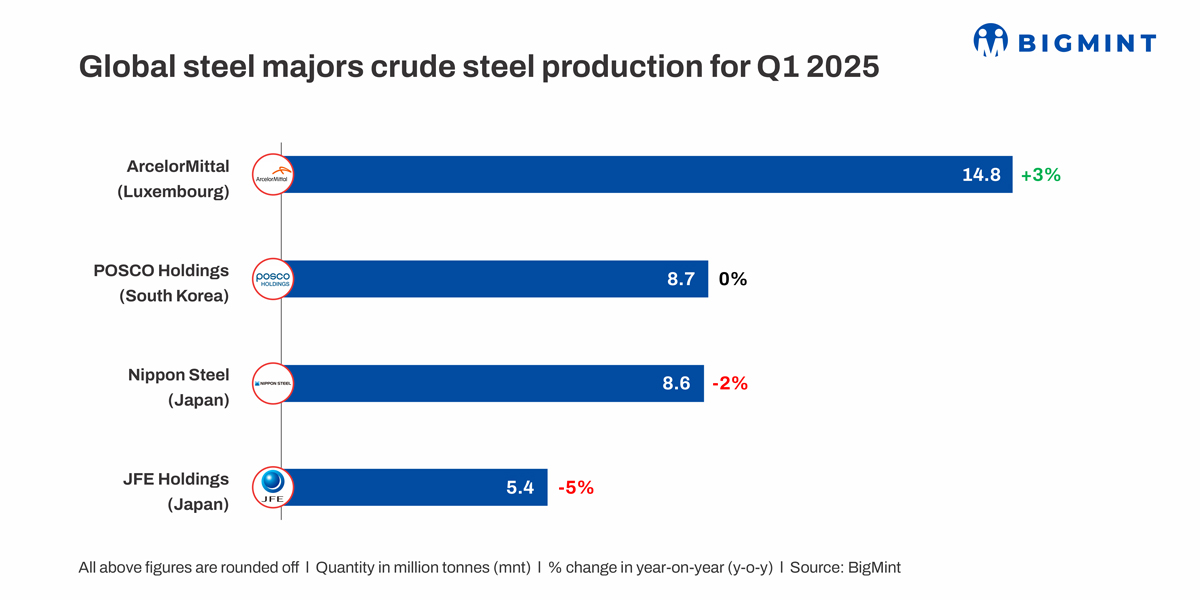

POSCO Holdings’ crude steel production in Q1CY’25 stood at 8.651 mnt, down by 5% q-o-q against 9.153 mnt in Q4CY’24. However, on a y-o-y basis, the same remained range-bound.

JFE Holdings’ quarterly non-consolidated crude steel output decreased by 3% to 5.39 mnt in Q4FY’24 (January-March 2025) from 5.53 mnt in Q3FY’24. Moreover, consolidated output dropped by 3% to 5.67 mnt in Q4FY’24 as compared to 5.83 mnt in Q3FY’24.

The company’s non-consolidated crude steel output for FY’24 (1 April 2024-31 March 2025) was 21.95 mnt, representing a decline of 6% from 23.45 mnt in FY’23. Furthermore, consolidated production dropped by 6% to 23.2 mnt as compared to 24.8 mnt in FY’23.

ArcelorMittal’s crude steel production in Q1CY’25 stood at 14.8 mnt, representing a rise of 6% from 14 mnt in Q4CY’24. Moreover, on a y-o-y basis, the same increased by 3%, against 14.4 mnt in Q1CY’24.

Financial results, market overview

Nippon Steel’s revenue for Q4FY’24 (January-March 2025) stood at JPY 2,143 billion, edging down by 4% y-o-y against JPY 2,226.2 billion in Q4FY’23. Furthermore, the company’s operating profit in FY’24 decreased by 30% y-o-y to JPY 547,960 million from JPY 778,662 million in FY’23.

JFE Holdings’ revenue decreased by JPY 350.9 billion or 9% to JPY 3,365.1 billion in FY’24 as compared to JPY 3,716 billion in FY’23.

While automobile production rebounded from quality concerns, plateauing demand and US tariffs impacted exports, creating uncertainty. Similarly, due to labour shortages, there were high shipbuilding backlogs, which hindered growth. Other manufacturing sectors, including construction machinery, were affected by reciprocal tariffs and an industrial machinery slowdown in China. Rising costs and labour shortages further depressed construction and civil engineering activity, delaying projects and dampening investment sentiment across sectors.

POSCO’s operating profit in Q1CY’25 was KRW 346 billion, up by KRW 51 billion or 17% y-o-y from KRW 295 billion in the corresponding period last year. However, the company’s revenue from steel sales decreased by KRW 552 billion or 6% y-o-y to KRW 8,968 billion in Q1CY’25 as compared to KRW 9,520 billion in Q1CY’24.

POSCO strategically focused its investments on pre-planned projects and explored new avenues for growth. Simultaneously, the company was committed to enhancing its facilities to achieve greater cost-competitiveness. In its steel operations, construction of an electric arc furnace (EAF) is underway to effectively meet the growing demand for low-carbon emission steel products. Furthermore, POSCO pursued overseas growth opportunities and improved the operational efficiency of its existing facilities through the strategic replacement or renovation of aged assets.

ArcelorMittal’s operating income for Q1CY’25 stood at $825 million, down by $247 million or 23% y-o-y from $1,072 million in the corresponding period last year (CPLY).

The company made progress on safety and growth initiatives while navigating global trade uncertainty. It prioritised domestic markets while leveraging its strong balance sheet to drive investment and returns.

Hyundai Steel’s consolidated revenue for Q1CY’25 declined by KRW 384 billion or 6% y-o-y to KRW 5,564 billion from KRW 5,948 billion in Q1CY’24. Moreover, the same dropped by KRW 49 billion or 1% q-o-q against KRW 5,613 billion in Q4CY’24.

Additionally, non-consolidated revenue for Q1CY’25 decreased by KRW 529 billion or 11% y-o-y to KRW 4,290 billion compared to KRW 4,819 billion in Q1CY’24. The same declined by KRW 193 billion or 4% q-o-q from KRW 4,483 billion in Q4CY’24.

Hyundai Steel witnessed stable steel prices due to reduced imports and production cuts, while raw material prices faced pressure from oversupply. This dynamic helped reinforce Hyundai Steel’s market position despite fluctuating raw material costs and demand shifts.

Outlook

Global steel majors navigated challenging market conditions in Q1CY’25, with declining output and financial pressures for most, though ArcelorMittal posted a 6% quarterly production rise and Nippon Steel managed to keep volumes stable. Looking ahead, ongoing demand uncertainty, trade disruptions, and rising input costs could weigh on performance. However, strategic shifts, such as POSCO’s investment in low-carbon technologies and Hyundai Steel’s market-driven adjustments, position the industry for potential recovery as global infrastructure and green initiatives drive long-term demand.

Leave a Reply