*China top importer despite drop in shipments

*India’s coal imports up 15% y-o-y

*Global inflation boosts cheaper Indonesian exports

*Surging Asian demand, sanctions on Russia to shape trade flows in CY23

Due to geopolitical upheavals, energy inflation and altered trade flows across the globe coal prices touched historic highs in 2022 and remained generally elevated throughout the year. Yet coal demand in 2022 dropped just 2% on the year. As per provisional data maintained with CoalMint, total imports of non-coking or thermal coal stood at 980 million tonnes (mnt). China, India, Japan and South Korea were the leading buyers of seaborne thermal coal.

Leading importers

China’s imports decreased by 18% to around 215 mnt, while India imported over 160 mnt in the year gone by – almost 15% higher y-o-y.

Tight pandemic restrictions weighed on industrial production and thereby power demand in China. However, imports increased towards the latter half of the year as power utilities sought overseas supplies to meet soaring demand in extreme hot weather. As severe drought and heatwaves hit western and southern China from late July, coal-fired power plants geared up production to meet the soaring demand for air conditioning and the supply gap from hydropower stations. They also increased purchases of higher quality thermal coal, such as Russian coal, to improve electricity generation efficiency.

Severe pandemic controls apart, China’s coal imports fell also due to higher domestic production, which increased by 9% y-o-y to 4.5 billion tonnes (bnt), as per data from the National Bureau of Statistics (NBS).

India’s coal imports increased y-o-y despite significant growth in domestic production partly due to the government’s mandate obligating operators of coal-based power plants to increase inventories by importing at least 10% of their coal demand and easing the restrictions on coal blending. Buyers also ramped up imports of sharply discounted coal from Russia.

Imports by Japan and South Korea stood at 135 mnt and 98 mnt – largely stable y-o-y. Economic momentum in these countries was subdued in 2022 as China’s strict zero-COVID measures stifled industrial activity across the world’s largest manufacturing base. Japan and South Korea have extensive supply chain ties with China which meant that each country suffered slowdowns in both productivity and demand growth in 2022 due to China’s COVID curbs. But imports shot up towards the end of the year on easing restrictions and stimulus measures in China. Elevated LNG prices, too, played a role in increasing the dependency on coal.

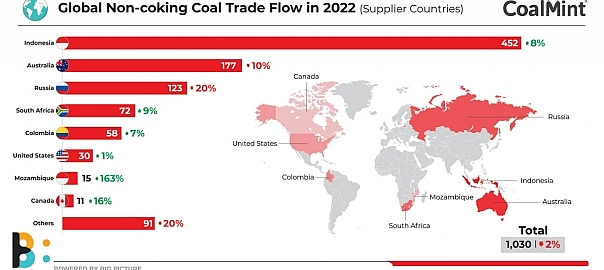

Major exporters

With over 450 mnt of shipments, Indonesia remained the leading thermal coal exporter in 2022 followed by Australia at 177 mnt, Russia at 123 mnt and South Africa with 72 mnt. While shipments by Indonesia increased by 8%, those by Australia and Russia fell by 10% and 20%, respectively. South Africa’s exports rose by 9% y-o-y.

While China continued to be the top importer of Indonesian coal, its percentage share in total imports came down from 28% at the start of 2022 to 25% towards the end, while that of India also came down from 25% to 21%. Indonesian shipments dropping by nearly 60% in January 2022 from December 2021, and stayed stunted in February, as the government’s partial ban on shipments jammed coal flows from the country and led to widespread confusion in international coal markets.

But Russia’s invasion of Ukraine changed all that. As Europe’s top natural gas supplier and the third largest global thermal coal exporter in 2021, Russia’s war in Ukraine upended power fuel markets across Europe, and ignited a fresh surge in coal prices to all-time highs by late February. In turn, those high prices quickly lured Indonesia coal flows back onto global markets.

The decline in Australia’s exports is mainly attributed to the pandemic reducing labour availability and adverse weather conditions from a strong La Nina phenomenon, which brought heavy rainfalls and severe storms. Australia’s thermal coal exports to China almost vanished due to an unofficial ban and were redirected to other Asian countries, such as Japan, Korea, and India.

Due to sanctions on Russian coal, Japanese buyers bought more of good quality Australian coal by entering into long-term contracts with suppliers. Exports to India and Vietnam also increased marginally. Indian sponge iron players are using more of 4600 NAR Australian coal for blending with South African material due to cost competitiveness.

Elevated Australian coal prices weighed on shipments to other Asian buyers such as South Korea and Thailand. However, Australian coal shipments increased to Europe throughout the year, falling towards the end of the year with European countries stocking up on both coal and LNG.

South African coal exports were hampered by disruptions in the country’s rail infrastructure caused by extensive cable theft, strikes and prolonged underinvestment. Trade dynamics changed with sanctions on Russia. As a result, more of South African coal was diverted to Europe, especially the Netherlands, while exports to the traditional markets of India and Pakistan dropped.

Indian sponge iron players (biggest users of South African coal) experimented with Russian, Australian, and Mozambican coal, impacting demand for South African coal. Buyers in Pakistan shifted to using more of Afghan coal during the year. While reopening of coal-based power plants in Europe aided consumers felled by elevated gas prices, the EU countries imported more of high-GCV South African coal.

Russia channelled cheaper cargoes to China and India amid sanctions. US sanctions on Russia gave sellers in that country more coal to sell to Europe. While India continued to be the top export destination for the US, its share fell from 26% to 21% towards the end of the year due to elevated prices. In India, the cement sector is the key buyer of high-GCV US coal and with pet coke prices being more competitive, cement manufacturers avoided booking costlier US coal.

Outlook

China and India are trying to reduce their dependency on coal imports and the European Union is seeking to turn away from coal-fired power generation. While China has mulled an import tax on coal from April, the Indian government has mandated that coal-based power utilities import 6% of their requirement to meet peak demand.

Also, the planned implementation of energy product sanctions on Russia by the EU this year is another factor likely to support global coal demand. Europe is set to ban imports of Russian oil products from 5 February in a move designed to apply further financial pressure on Moscow in response to the Ukraine invasion. That move is expected to further tighten supplies of all industrial fuels, and spur additional import demand of alternatives such as coal.

Moreover, in late 2022, China announced a slew of stimulus and easing measures designed to restore economic activity across the country. Increased industrial activity late last year already lifted coal imports in November and December to their highest since late 2021, and further fuel purchases look likely by the top purchaser of Indonesian coal as China’s economy gathers further momentum.

Therefore, it does not seem that global coal trade is losing steam in 2023 despite the long-term projection of contraction in conjunction with the growth in renewable power.

2nd Asia Coal Trade Summit

The IEA has predicted that coal imports in parts of Asia are expected to rise. Excluding China, India, Japan and South Korea, Asia’s thermal coal imports are forecast to grow by 29 mnt to 231 mnt by 2025. The increase will be led by countries such as Vietnam, the Philippines, and Malaysia. To gain a holistic perspective on emerging coal demand and trade dynamics in Asia sign in for CoalMint’s 2nd Asia Coal Trade Summit to be held in Bangkok, Thailand, from 24-25 April, 2023.

Leave a Reply